ENRI Indonesia retweetet

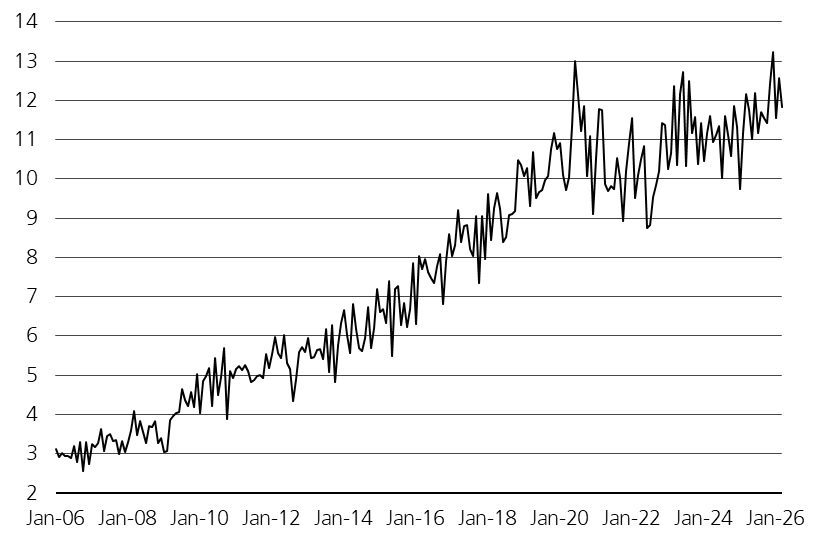

Germany's wholesale prices have risen by 4.1% year-on-year in March, the fastest growth in over three years amid surging petroleum prices.

English

ENRI Indonesia

90.3K posts

@DodiJusra

Energy and Natural Resources Institute of Indonesia