Millionaur retweetet

Anthropic is doubling their fundraising plans to $20B.

Handful of public companies are directly exposed + invested.

But this is where is gets interesting.

$ZM up roughly 20% in 3 days.

$AMZN up 6% in 3 days.

$SKM up 15%+ too.

Common denominator? Anthropic.

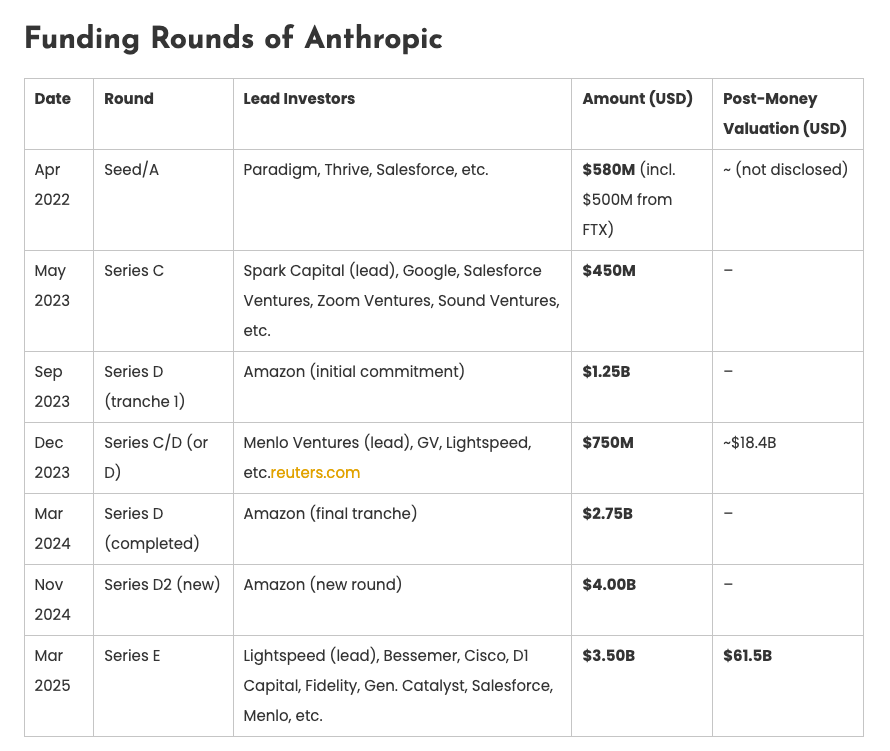

Here's what I found for the investments.

Seed + Series A

> $CRM

Series C

> $GOOG

> $CRM (again)

> $ZM

Strategic Investment

> $SKM

Series D

> $AMZN (multi-year investment)

Series E

> $CSCO

> $CRM (again x2)

After that?

$NVDA + $MSFT got involved.

$AMZN has the most financial exposure to Anthropic by far.

But $CRM invested early and repeatedly, and it's the ONLY one of this group that is red on the day.

Everything else has ripped the last three days.

Yes, $CRM's anthropic stake is likely only a few hundred million dollars (not super meaningful to a $200B company)...

But strategically? Salesforce is probably the enterprise software company most aligned with Anthropic.

Enterprise software has been dead lately but add in AI leverage w Anthropic? $CRM could re-rate quickly.

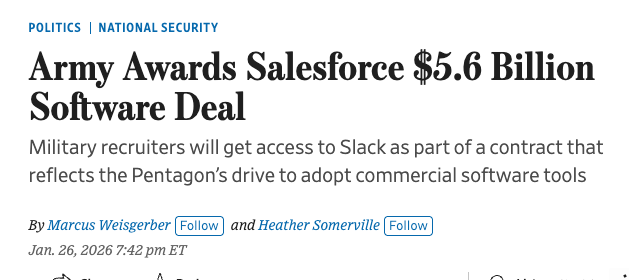

..and I'm not even going to mention the $5.6B software deal with the Army yesterday (that's a story for another day).

Low risk spot on the chart too, sitting on a huge weekly support.

I'll risk a daily close under $220 for $CRM to see $260+ again soon, currently $226.

$CRM is my top Anthropic play right now.

amit@amitisinvesting

BREAKING: Anthrophic is doubling their fundraising plans from $10B to $20B, as per the Financial Times. This will value the company at $350B as investor interest is now 5x the original size of the round. Anthropic went from $1B to $9B in ARR last year. $NVDA $AMD $AVGO $MSFT

English