RationalExuberance retweetledi

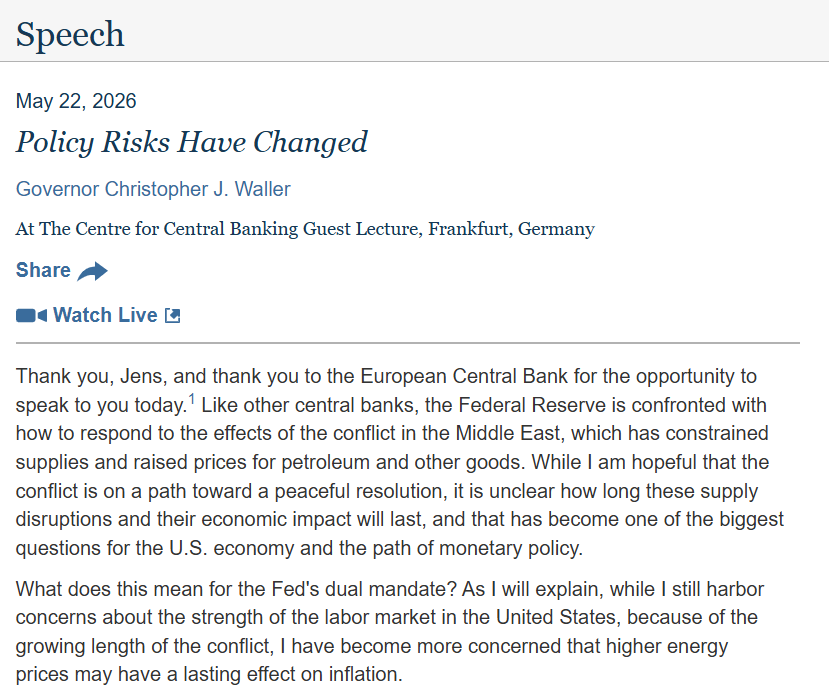

This is a hawkish speech from Waller. While he doesn’t think hikes are needed in the near-term, he comes across as quite troubled by recent inflation developments. I’ll thread a few highlights:

English

RationalExuberance

11.3K posts

Watch @JoeSquawk's full interview with Treasury Secretary Scott Bessent: cnb.cx/4tvp4j5

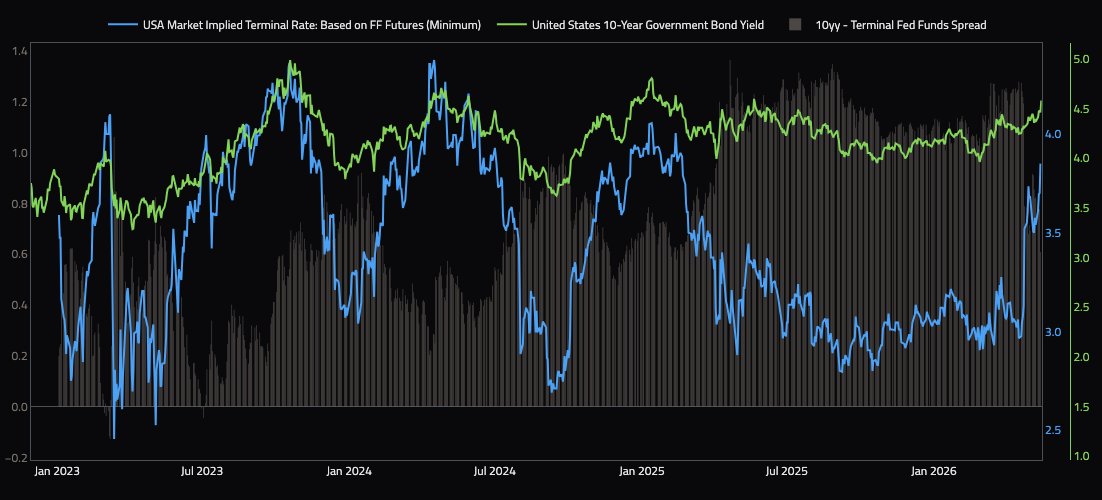

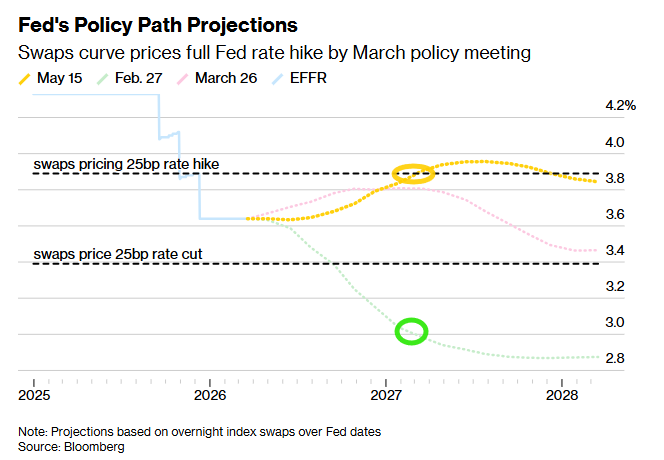

From the Markets Update (neilsethi.substack.com/p/markets-upda…): FOMC rate expectations from the CME Fedwatch tool pushed a little higher with rate hike bets now peaking next July at 77% (the highest to date). The chance of a 2026 rate hike up to 49% (while chance of a cut is 0.4%). The chances of two hikes by the end of next year now 39% (July). The chance of one cut by the end of next year is 11.5%.

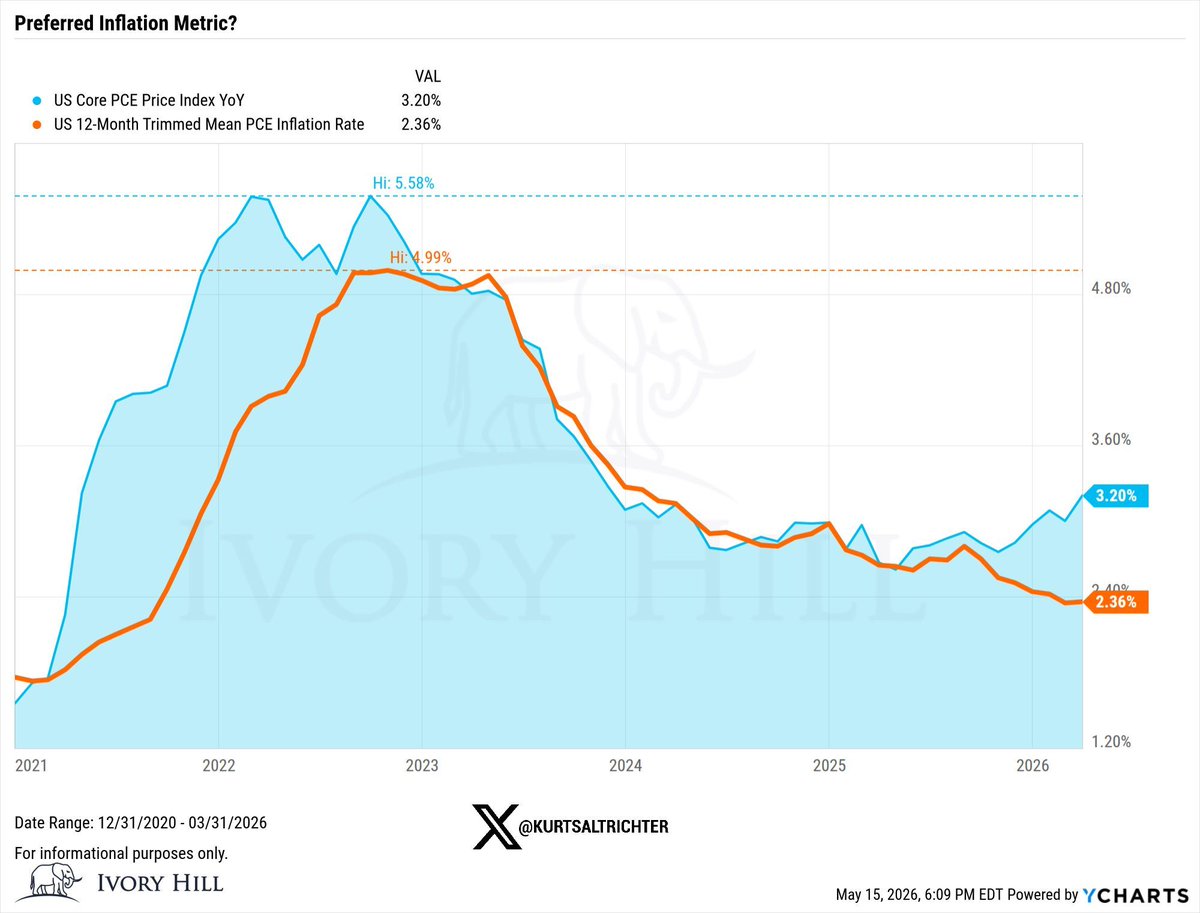

Two gauges of US inflation, CPI & PCE, have diverged meaningfully. The reason: Price spikes in products tied to the AI infrastructure buildout. "AI infrastructure demand plus energy-related supply constraints tied to the Iran conflict could make inflation more persistent:" Pimco