@BitcoinAIGuy i rotated into iren last time you told us and i regret it so much

English

Anthony 🦛

75 posts

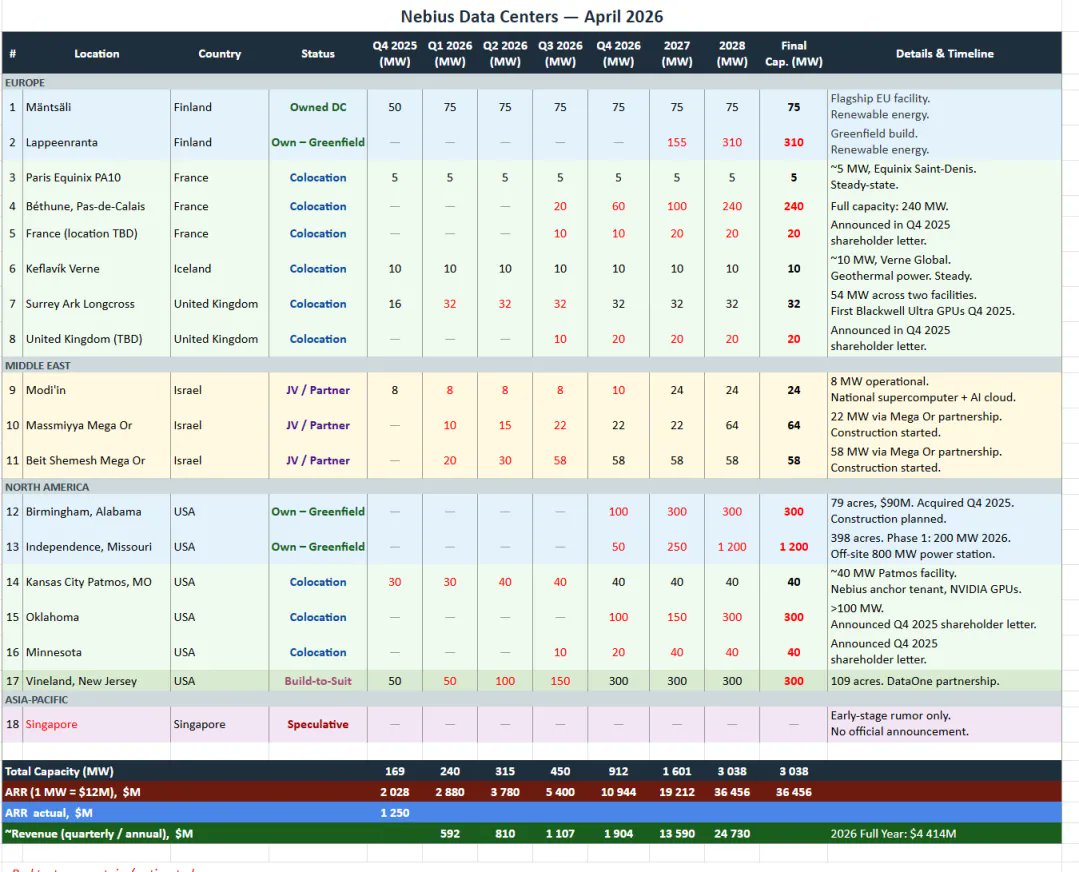

JUST IN: $NBIS RAISES 2026 CAPEX GUIDANCE TO $20 BILLION TO $25 BILLION UP FROM $16B to $20B

$IREN Where is a CUSTOMER deal? What are they going to do with energised sweet water 1? I was seriously expecting a deal with a hyperscalar after they already announced they have energised SW1. What am I missing?

$SIVE $POET Marvell just cancelled its POET orders (the ones tied to Celestial AI). It created some noise today — Sivers went from +20% to flat, POET is down -45%. But let’s be clear on what this actually means for $SIVE: The POET path to Marvell (and therefore Google) was always one of the more speculative legs. It was still in early prototype/qualification stage. Meaningful revenue from this path was never expected until 2027+ anyway. SIVE’s core drivers remain completely untouched: → Jabil 1.6T LRO (confirmed and progressing) → Ayar Labs (active orders & qualification) → O-Net + Enablence (external light source modules) This is why we talked about how SIVE’s multi-path strategy is such a big de-risking factor. One leg gets delayed → the rest of the map keeps moving. Overreaction in the short term, in my opinion.

$IREN CEO keeps talking about how much capacity they have and how much demand there is. Still, they haven’t signed a single deal in the last 6 months. Just for comparison: do you remember the first $NBIS x $META deal? Nebius’s CEO Arkady Volozh stated that the initial $3 billion AI infrastructure deal with Meta was limited to that amount specifically because the company had sold out of all its currently available capacity. Last month, $NBIS announced the deal with $META will be now worth up to $27 billion! $IREN talks about capacity and demand while $NBIS signs deals and partnerships.