Sabitlenmiş Tweet

Armaan

9.9K posts

Armaan

@Armaanchan

UNC Kenan Flagler Alumni | Investment Analyst at Trusted Advisors | Former Crypto Journalist @Cointelegraph and @Bitcoinist

Panama Katılım Kasım 2010

603 Takip Edilen925 Takipçiler

@RiceRiddler How are they gonna keep going with one piece after the Manga is done is the real question

English

Genuine question:

I look at Pokémon cards and see an iconic IP with a huge ecosystem of players, vendors, collectors, and fans built and nurtured over the last 3 decades. Collectors of all ages collect specific artists, sets, and even extremely niche things like “cards with sleeping Pokémon”.

I look at One Piece TCG and see an equally iconic IP with a 3-4 year old TCG, with a quickly growing competitive scene and tournament-won prize card sales being sold to collectors every day for 5-6 figures.

Do we ever see OPTCG ever catching up to or even surpassing Pokémon TCG’s chokehold on a legion of diehard collectors? Why or why not?

English

@MeenaMaysa_Phat Have whatsapp? Interested in ticket purchase service

English

@Armaanchan You must have the email address registered with your ticket purchase to make a purchase. If you don't have one, the shop offers a ticket purchasing service for you.

English

รับกดบัตร Tomorrowland Thailand 🇹🇭

ค่ากด 500-1500฿

✅ว่าง 2 คิวสุดท้าย

*มีมัดจำค่ากดเพื่อล็อคคิว

#TomorrowlandThailand #Tomorrowland

รับกดบัตรคอน 🐶 Meena 🐧 Maysa@MeenaMaysa_Phat

รับกดบัตร Tomorrowland Thailand 🇹🇭 ค่ากดเริ่มต้น 500-1500฿ Full Madness Pass ฿ 12500 Full Madness Comfort (VIP) ฿ 20200 Day Pass Prices ฿ 5100 Day Comfort (VIP) Pass ฿ 8200 #TomorrowlandThailand #Tomorrowland

ไทย

@GlobalCollapse @BTC_Bella69420 @power_analys1s @McnallieM @FransBakker9812 @TheKamaHsutra @cazenove_uk @seancbuckley @BitcoinAIGuy @Agrippa_Inv @Freedom_By_40 It's already at $15M, shares outstanding are not updated

English

@BTC_Bella69420 @power_analys1s @McnallieM @FransBakker9812 @TheKamaHsutra @cazenove_uk @seancbuckley @BitcoinAIGuy @Agrippa_Inv @Freedom_By_40 Just gotta hope $MIGI reaches $10M market cap and you're good to go :)

English

🏆 Miner Madness 5.0 Update

Top 3 Leaderboard:

🥇 Andrew Burge +36.14%

🥈 Rogue Koala +35.57%

🥉 Paul +35.42%

Top Analysts:

🔥 @McnallieM +29.30%

🔥 @FransBakker9812 +28.72%

🔥 @TheKamaHsutra +28.58%

#MinerMadness #BitcoinMiners #BTCUSD

powermininganalysis.com/miner-madness5

English

@aleabitoreddit @Bash29398256308 Also curious at to why $SLNH is an exception here

English

Almost every Neocloud segment stock is a extremely solid buy (maybe aside from $SLNH)

$WYFI is kinda T2 with NScale's $865m agreement. But it's valuation got completely reset from $40 to $15. So it's an extremely attractive buy up there along with $NBIS, $IREN, $CIFR, $WULF and the others.

English

Welcome to 2026. Jan 1st ratings:

Strong Buy:

$TTD

$SMCI

$AIRO

$INTC

$HIMS

$AXTI

$TSM

$NBIS

$CIFR

Samsung Electronics (KRX: 005930)

$HUT

$IREN

$WULF

$GLXY

$TSSI

$META

$ETOR

$CRCL

Buy:

$KRKNF

$ONDS

$GEMI

$NVDA

$MU

$AMKR

SK Hynix

$SNAP

$RDDT

$AAOI

$COHR

$FISV

$FLY

$DJT

$LITE

$AMZN

$MRVL

$AVGO

$OSS

$BULL

$ORCL

$CRDO

$ALAB

Avoid:

$RGTI

$QBTS

$RGTI

$BMNR

$ETH

$PLTR

$WMT

_

TLDR thoughts:

TTD - Complete valuation reset dropping 67% YTD, compounded by EOY tax sell-off. Great recovery play going into 2026.

SMCI - Trades like distressed company just because they delayed revenue by 1 quarter for new blackwell specs. Forward revenue is increasing 50% Y/Y, P/S close to .5 now. Great recovery play from tax harvesting.

AIRO - Roughly ~1/6th balance sheet was cash. Everyone seems to be into drones, especially with accelerated gov inevstments. Another IPO name that got sold off. Great recovery play going into 2026 with esp. hot segment. Roughly ~3.8x P/S compared to ONDS trading at 25-30 P/S, but obviously there's quite a lot of other businesses like their education sector which messed up margin calculations quite a bit.

INTC - It's literally become the semi arm of the US government. Hyperscalers will likely be incentived (strongly pressured) to use Intel whatever chance it gets over TSM, Samsung, etc. I would not bet against the US government.

HIMS - Huge selloff going into 2026. Down from $70's. Sales/Traffic is down, but Zava acquisition/growth should add a huge tailwind going into 2026. Esp. with few hundred mill buybacks, strong recovery play first two monts in.

AXTI - Posted thesis on this earlier. CEO - "40% of Inp supply chain", InP will be a huge, huge bottleneck for hyperscaler AI buildout 2026-2027 until there's enough time to engineer around it in 2028.

TSM - I've covered this quote a lot. Increasing margins. Maxed out demand. Just extremely good compounder next few years.

Samsung Electronics - benefits from foundry/memory. just golden egg regarding all the tailwinds helping the buisness.

NBIS - Extremely strong buy, $7-9B ARR, it's literally 5 different companies growing triple digits Y/Y. management quoted 20-30% EBIT margins, it's just a waiting agme.

CIFR, HUT, IREN, WULF, GLXY - Whole datacenter space is extremely sold off after Oracle/OpenAI fears. OpenAI recently raised $40B, another $10B from $AMZN, and more. So a lot of fears regarding capex spend has been de-risked. It's multifaceted too, eg. Bitcoin drop, affects $CIFR balance sheet, $GLXY in crypto space. But generally huge recovery play/ramp for neoclouds sector.

TSSI - Similar to SMCI. deferred revenue = nuke. Should recover after tax harvesting + lot of revenue gets recognized

META - Huge algorithmic selloff post earnings due to one-time tax. They also cut capex/opex spend of their reality labs and other departments and this should be a huge tailwind for EPS going into 2026.

ETOR - Literally sitting on $1.2B with a $2.8B marketcap and growing double digits Y/Y still. $150M buyback should be a nice tailwind, and tax harvesting from YTD performance should subside.

CRCL - Same as stablecoin thesis should be really solid going into 2026

Buy

KRKNF - Anduril partner+ scale. Probable uplisting in 2026, lot of tailwinds from defense spending.

ONDS -pretty explosive revenue growth, new $10m contracts left and right. large cash balance to fund r&d. Pretty high p/s but there's valuation premiums for speculative leaders in the space like rklb.

GEMI - So i typically dont like exchanges, but gemini got nuked from $30+ IPO sub $10. pretty solid recovery play.

NVDA - Huge backlog lol. Everyone knows bull case for nvidia

MU - Memory is hot

SK Hynix - Memory is hot

AMKR - benefits from "made in america" chip expansion in prod.

SNAP - Opex Cut from memory, increase revenue from memory monetization, $400m from perplixity. $1.5B revenue/quarter. They could literally stop growing revenue complelty if they convert all of that to $1B+ FCF/year, it would re-rate snap completly.

RDDT - This is not going anywhere for the next 10+ years tbh, it's like robinhood of social media, growing extremely fast from new ways to monetize revenue, and just extrmeely profitable.

AAOI - interconnect play for amzn, msft asic scale up.

COHR - benefits from photonics rollout for next gen asics.

FISV - Nuked a bit too much post ER, strong recovery play esp. post tax-harves.t

FLY - Space is hot from SpaceX IPO. Should do well given tax harvesting is over, and they have medium lift coming up with northrop.

DJT - I never thought i'd put this here lol, but this is just because of their TAE merger.

LITE - Large BOM from Google TPU rollout, attractive valuation. Slight selloff after Google TPU revised est. but it's basically in every single hyperscaler asic deployment.

AMZN - one of the mag7 that's not overvalued

MRVL - Selloff from analyst misinformation, strong buy going into 2026. Especially with msft maia revenue doubling Marvell's current revenue when it ramps up

AVGO - Like NVDA just strong long, as AI infrastructure deployment ramps up

OSS - I made a post speculating that they're one of andruils' suppliers. but regardless, edge computing will be hot 2026 and its 180m mc presents attracctive upside.

BULL - similar to robinhood where they have a huge userbase, but they just need to figure out monetization

Oracle - Sold off a bit too much imo. I put this on avoid months ago but after the from from $330 to $190, it's more attractive again esp. after openai raised another $40B

CRDO -extremely high margin, necessary connectivity for dc rollout

ALAB - extremely high margin, necessary connectivity for dc rollout

Avoid:

There's a lot of stuff on the "overvalued list" like $RKLB that i like but I wouldn't quite say avoid it either aside from these.

RGTI , QBTS, RGTI - Quantum names are still overvalued and likely won't deliver fcf in the next few ytears.

BMNR, ETH - if you saw my eth post, not exactly bullish since the amount of ETH burn is just single-low double digits every day, which is a joke.

PLTR - one of the most overvalued ai names

WMT - How is this 40 p/e? This is Walmart?

__

(these are based on today's prices)

TLDR:

IPO names like Circle, Etoro, AIRO, Klarna, Figma, present attractive upsides post drop + tax harvesting going into 2026.

Tons of names like SMCI, HIMS that dropped 40% or so past 3 months, are amazing swing/recovery trades post-tax harvest + Jan effect.

Lot of the names that doom dropped like FiserV or The Trade Desk present good recovery trades too post-tax harvest.

Many datacenter stocks like nebius, iren, cifr, wulf, galaxy, are amazing recovery trades too.

Lot of other segments like memory, bottlenecks, photonics, and others are just great longs in 2026, despite each hitting ATHs.

There's still quite a lot of overvalued names from Quantum, to certain Space stocks (eg. planet or rocketlab), specific AI names like Palantir to retail stocks like Walmart that I would probably avoid for the time being until there's a slight correction.

This was a TLDR just if I'm short term trading-only (not long term) but feel free to ask questions.

Serenity@aleabitoreddit

2026 Newsletter. Thematic Investments: Evolution, Disruption, and Bottlenecks 1. Soft Robotics - Evolution to $TSLA, $ONDS, Boston Dynamics. 2. SiPh - InP Bottleneck | $AXTI, $LITE, $GOOGL 3. Glass Substrates - Bottleneck | $NVDA, $INTC, $TSM 4. Money Movement - Disruption to $V, Stripe, $BOA 5. AI Cloud Layers - Bottleneck | $NBIS, $IREN, $HUT. 6. LLM Cybersecuirty - Evolution to $CRWD, $CSCO, $MSFT 7. LEO Space Infrastructure | Evolution to $RKLB, SpaceX, $ASTS 8. Consumer Agentic Workflows (50 Step) - Disruption to the Consumer Workforce, from Manus, $PATH Cognition 9. Distributed Computing Latency - Bottleneck | $TSLA, $AMZN, $GOOGL, 10. Copper Interconnect Life Extension - Bottleneck | $NVDA (LPU/Groq), $AMD, $INTC _ This is an light overview of thematic investments I find the most interesting from a public-information synthesis perspective + second/third-order effects from bottlenecks! _ 1. Soft Robotics: The Evolution to Robotics Traditional robotics (Optimus, Boston Dynamics) relies on Inverse Kinematics to rigid joints. Soft robotics changes the math. We've met the point where hardware (Optimus, Boston Dynamics, Figure) met LLMs (Gemini, Grok, Opus), and we're at the beginning of possible widespread commercialization. By using materials inspired by octopus tentacles and human skin, robots are moving away from gears and toward fluidity to handle extremely delicate tasks like handling produce like the human hand, to picking up extremely heavy surfaces adding Octopus-like extensions to $ONDS/Andruil Drones. The evolution is thinking outside the box in terms of what robotics can do. I remember working with some Stanford PHds in this field like 7 years ago, and it just so happens AI is starting to be commercialized after many years of research. So expected, this field to be as well. Possibilities are limitless adding organism-like fluidity to rigid robotics, this is just the natural evolution. Most of these are prob private companies. _ 2. Silicon Photonics - Bottleneck of the AI Infrastructure "InP Chokepoint" Blackwell Ultra Clusters to Google TPUs have hit the upper wall and requires photonics for interconnects | OCS to scale up. The Substrates: $AXTI (via Tongmei) and Sumitomo (Japan) control roughly 60-70% of the world's InP substrate market. The Materials: Companies like Vital Materials (China) and AXT control the refining of the raw Indium itself (78%+ of supply chain). If you are a US tech giant, your entire "AI Growth Story" for 2026 depends on materials controlled by geopolitical rivals. The only scalable solution is engineering around it, either by delivering light-on-chip, while using 90% less InP or companies that use tiny slivers of Indium Phosphide instead of large, expensive wafers. There's opportunities with the bottleneck itself like AXT, Sumitomo. Or companies that help address it like $POET. _ 3. Glass Substrates - Fixing the Bottleneck for CPOs from $NVDA to others. The shift toward glass substrates is essentially the semiconductor industry’s answer to a physical wall they are hitting with current materials. Current chips sit on a substrate made of organic materials (essentially specialized plastic). As chips get larger, like Nvidia's massive GPU packages, plastic substrates warps. So, glass substrates is becoming the industry standard for Co-Packaged Optics (CPO) because they solve the single biggest problem in photonics with alignment. US Government already sees this as a necessity and we've seen huge subsidies funneling down to some of these companies. Companies like $INTC, Samsung Electronics, Absolics (SKC Subsidiary), DNP, and others are the main beneficiaries, especially as MRVL and $AVGO (driving glass for optical switches) move forward with CPO revolution. _ 4. Money Movement - The Disruption to Card Networks, Banking, Exchange, and Payments For decades, moving money has been a "toll road" business. Every time you swiped a card, 2% to 3% of that money vanished into the pockets of the Card Networks (Visa/Mastercard) and Issuing Banks. Or buying/selling crypto from an exchange would be .2-1%. It was the most profitable, "un-killable" business model in history. Until now. The "Genius Act" of 2025 just handed companies like $XRP with Money Transmitter Licenses or Banking Charters the keys to the kingdom. Not really theoretical for me. I happen to be working on this myself at my own startup with some folks who created V / $PYPL's real-time payment networks. But basically companies with existing MTLs or pursuing banking charters leveraging the Genius Act and some other tech can now bypass legacy % fees by doing settlement on top of the Federal Reserve and blockchains, effectively converting percentage-based fees into a few cents. Would 99% companies do it? Probably not since every single margin from across the payment industry would just go to 0. I'd be happy though. But basically Bridge's $1.1B acquisition by Stripe should have been a red-alarm to existing companies that days of 1-Day ACH, interchange models, $25 international transfers, are soon to be over. This extends to many other adjacents from low fee disruptions like $HOOD, Mercury all the way to Stablecoin Neobanks, or companies making their own stablecoins like $SOFI. _ 5. AI Cloud Layers - The Solution to HyperScaler compute Bottleneck While Hyperscalers are stuck in 3-5 year grid interconnection queues, miners like WULF and IREN are sitting on plug-ready GWs today This is the opportunity of a lifetime as hyperscaler funnel their cash cow Cloud revenues down to tiny companies. There's many different layers to this from Fluidstack, Poolside, Fireworks on the GPU orchestration layer, to the bare metal layer that companies like IREN are building. Then there's becoming the hyperscaler themselves like NBIS owning the physical locations, the GPU, software orchestration, and then providing simple interfaces for inference. This is the opportunity for a few small companies to become Amazon Web Service or Microsoft Azure over the next year or two, or get acquired (eg. GOOGL buying Intersect for $4.7B) Neoclouds like NBIS, IREN, CRWV, down to colo plays like CIFR, WULF, HUT (and private sectors -> Energy) stand to benefit. _ 6. LLM Cybersecurity - The Evolution to Modern Security and Vulnerability Defense Recent reports (e.g., from Anthropic's Red Team) showed that advanced models like Opus (and future iterations) could autonomously scan open-source smart contracts and identify "Zero-Day" exploits worth millions of dollars in minutes. The Implication: If an AI can find a logic flaw in a immutable Blockchain contract, it can find a flaw in a bank's SWIFT API or a power grid's control software. Same with KYC/AML. Models like Gemini Nano Banana are able to create realistic images/videos of people and people are able to get past a lot of programs. There's tons of things as an unsexy alpha in this field like LLMs automating away SOC2/PCI dss compliance to agents sitting on a server, continuously monitor logs, and auto-generate the evidence needed for auditors. 7. LEO Space Infrastructure | The Evolution to Expanding into the final frontier. Space is the next big thing. This is not anything new. (hope you got the joke). But anywhere from companies like $RKLB, SpaceX. Companies that fix orbital congestion or launch cadence bottlenecks. To companies that commercialize the infrastructure like ASTS or Starlink present many opportunities over the next year. So companies like Impulse, Blue Origin, $ASOZF to RKLB, $ASTS stand to benefit across the entire chain. 8. Consumer Agentic Workflows (50 Step) - Disruption to the Consumer Workforce, from Manus, PATH Cognition This one is simple and needs no explanation. But largely obvious in potential impact on employment + cost saving. How do you automate away business development? How do you automate away marketing? How do you automate away software engineers? This is going past few step ChatGPT answers and directly in to the real world where an AI agent can roam X, find the right people, DM someone, continue conversations, and lead to a sales call in just one workflow. This is the end of the "Chatbot" era and the beginning of the "Action" era replacing everyone previously required in a company. I haven't quite seen this done at scale yet with any company. Public companies like META that own these, don't really present the best exposure. Maybe $PATH for public space. 9. Distributed Computing Latency - Fixing the Bottleneck for AI Compute Capacity Strains Hyperscalers like GOOGL Cloud, MSFT Azure at max capacity. Elon Musk already floated distributed computing as the future of solving this issue (eg. having networks of $TSLA's providing compute for LLMs for inference). The "Tesla Compute Cloud" thesis is fascinating, but the single biggest physical barrier I've identified is: Inference Latency. Too generate "Token B," the model must first finish generating "Token A." It cannot do both at the same time. If you split a massive model (like Grok-3) across 5 different cars to fit it in memory, you have to send data between those cars for every single token generated. So, if your network latency between cars is even 20ms (optimistic for 5G), and you are generating 50 tokens, you just added 1 full second of pure "waiting time" (latency) on top of the compute time. In a data center using NVLink, that wait time is measured in nanoseconds. Same applies to any spare computer, GPU, and others owned by retail users. And there's billions of consumer GPUs (Teslas, iPhones, Gaming PCs) that sit idle 90% of the time. Solving the "distributed latency" problem for inference presents one of the single greatest arbitrage opportunity in the history of computing. Haven't really seen any companies that accomplished this at scale yet. Maybe NVIDIA Dynamo, $AKAM, TSLA, getting a little closer. 10. Copper Interconnect Life Extension - Addressing the Bottlenecks of Nvidia and Others Since we can't have infinite InP, we have to engineer around it with what we have (eg. Copper), so copper cables can do things that physics said it shouldnt like carrying 224G signals across a rack without signal loss. The industry is hitting a hard stop on InP where, US cannot physically cannot mine and refine enough InP to turn every link in a data center into fiber optics. If anything helps, then it's good. EG. NVDA's $20B "Acqui-hire" of Groq's team and IP. LPU is more about inference latency/architecture but it addresses copper life extension as a byproduct. Groq’s entire architecture beat Nvidia on latency because it rejected optics. Groq uses a "deterministic" mesh that relies on direct electrical (copper) connections between chips, avoiding the "jitter" and conversion time of optical switches. Companies like $ALAB, $CRDO, Groq, or anyone who can find ways to engineer around the optical bottleneck with copper will be a winner. _ There are tons of trades from both private sector investments to public! Just wrote up my thoughts on the fly today, but happy to elaborate later. Regardless I believe a lot of these thematic investments from: Investing in InQ Bottleneck Workarounds ( $POET ) or the bottleneck itself ( $AXTI ) to Disruptors ( $CRCL ) in the public sector. To Investing in copper extension bottleneck fixes (Groq), bank charter disruptors (Mercury) to evolutionary companies (Lightmatter, Festo) in the private sector. Present asymmetrical upside in 2026. Happy New Year!

English

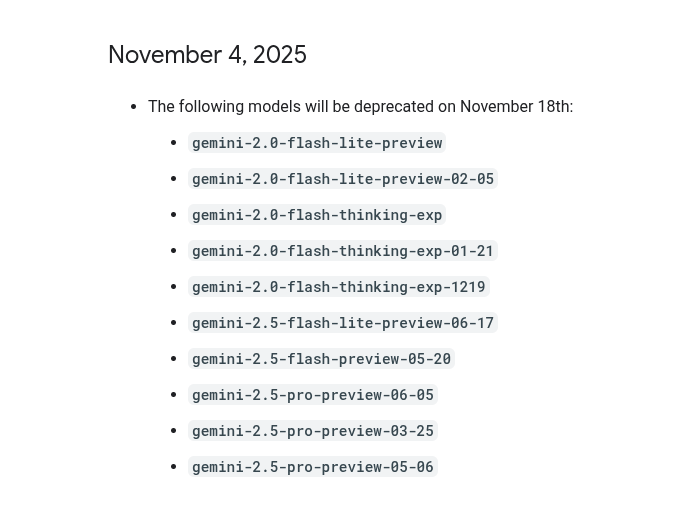

@Sargallot @Polymarket That photo is not updated by the way. They changed it in their Changelog. See below and scroll to the Nov 4th update.

ai.google.dev/gemini-api/doc…

English

Okay so.. about Gemini 3.0 Release date bet on @Polymarket . Here is some data you might be interested to know.

1. Deprecated models on November 18th are only EXPERIMENTAL models. Flagships keep running. People are getting hyped thinking that will be the day. No its not.

English

@Kenboyasahi @Learnernoearner Yeah explain . He’s just a larp I’m guessing??

English

@iMxrco @RealSkarm @Catscollecttcg I've had a seller do this for another order: escalate to ebay and get your money back. He's not shipping

English

@RealSkarm @Catscollecttcg Yeah I’m thinking he’s going to do the same. It’s a shame because he provided tracking number on Aug 29th but absolutely no movement.

English

My cost for McDonald’s pikachu is now $63… 😵

Won’t be ordering any more of those lol

English

@BestPokemonDeal @coopandchar Are 151 surprise slim boxes listed at $105 on eBay legit?

I've checked the Chinese apps and locally they're at $90: makes no sense for them to be only $100 flat on ebay?

English

You’re right, everyone got screwed by Surprise 151 release, and part of the reason of pricing Gem 3 higher is because Chinese stores want to make sure that doesn’t happen again.

In terms of the fakes, that’s why I’m extra careful to only post shops I vet heavily or ones I personally talk to frequently. Also why I try and make sure to share pictures of people’s Gengachu pulls.

English

For everyone asking me about Gem Pack 3,

Just wait till closer to release.

I’m not saying you’ll see better than $70, but I know that at $70 China-based sellers are confident there’s a margin to be made and that they won’t oversell like with Surprise 151.

Hopefully we get better pricing but it all depends on how release plays out, and what the secondary market starts pricing things out as unfortunately.

English

@CormickRips The back of graded guards help make it feel like it has more protection vs just bumpers imo

English

Since GradedGuard wants to be all mysterious or whatever with these limited ass drops & have them resell for 10x retail price I decided to try out DragonScaleSupplies with very similar + more designs. Just got my first 2 in and they didn’t disappoint, will be ordering more! 🔥👏

English

@MrGenXGuy Have you seen any tutorials on cracking these?

Just got a couple and the fit is so tight against the card on the edges

English

Who wants to learn about the CCIC grading? Read on….

Established for card grading in June 2024 this is a state owned (Chinese Gov) grading company and if you send them fake cards - well that is a felony. A CCIC is assurance your card is legit!

BUT you should do a cert check. Open WeChat and type in the search field CCIC and click on that. Follow my two pictures and scan the QR code on the card. Voila!!

Will post scan results in the comments.

When buying I’d say price a Blue 10 at 25% above a raw card value. A blue 10 can be a PSA 9/10 from what I’ve read. They also have gold 10s. I will buy a bunch of blue 10s and crack em all for fun and send to PSA.

The slabs are similar to TAG and are amazing. Highly recommended - so watch EBay for deals. Don’t sleep on these as I think they are awesome; just make sure your card is legit. It only costs like $5 to grade these in China btw so I expect to see a lot more of these in the future as a standard dor selling Chinese singles.

@StevenxTCG tagging you in as I feel like you’d like to know this too!

English

@ScalpersDaWild @foxpulls @RattlePokemon @Kennyboulder They do but right away I can tell the color on the pack is faded. Definitely open the pack to make sure?

English

English

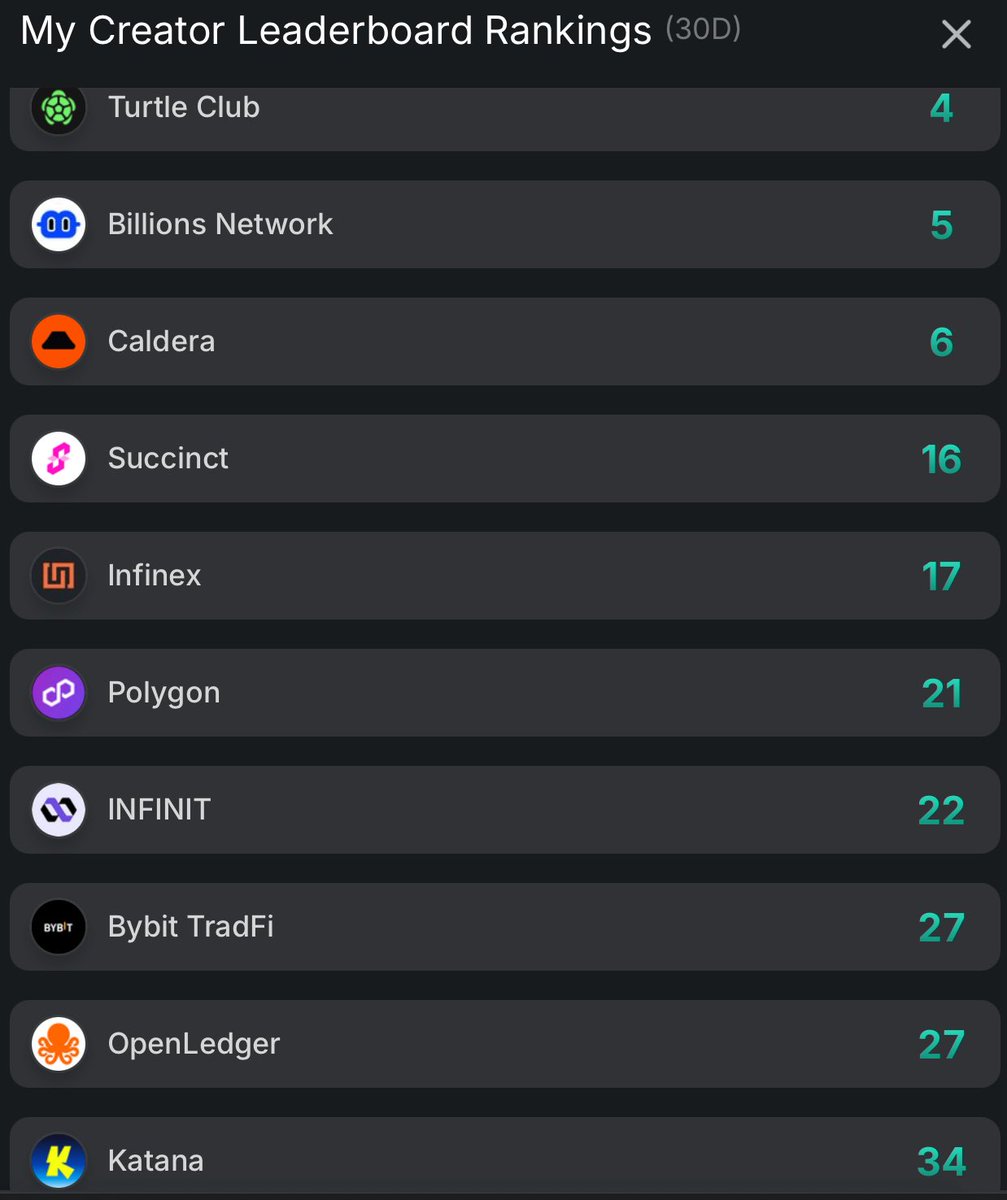

@wals_eth @turtledotxyz Have you tried $HOME? Direct competitor to Infinex that is already live and has an ongoing campaign in Kaito

English

The disrespect from Infinex is WILD, I will not negotiate with terrorists.

My stables on Infinex will find a forever home in Katana vaults on @turtledotxyz

Infinex has a LOT to learn about community building from Turtle Club & Katana.

Some founders need to get humbled asap.

English

@faysal444888 @sunil_trades Just wait. If you're approved for payment details as well, then you'll be in the end of September distribution

English

@sunil_trades I have $4700 stuck in my FTX account, which can be sold to ftx creditor for $3982, with all my completed kyc, is it okay to sell or should I wait?

English

As ETH breaks $4200, we remember

FTX creditors being paid $1250 for our ETH

English

English

@GatewayCollects @Armaanchan @eelchico @PokiPair Yeah complete bs but was expected honestly. I’m still going to blast this shop with negative feedback and on socials after they send my money back…last time I ever buy from china

English

@eelchico @GatewayCollects @PokiPair @ZeusTheDegen

Got my first cancellation for two Pikachu's today. 5000 feedback shop refunded and deactivated ebay account.

Yea, this won't be pretty

English

English

Dropping 1 case of SC 151 vol 3 Surprise. Price is slightly higher than before. This will probably be the last booster boxes we will sell of Surprise.

evolvedxgaming.com/products/sc-15…

English

@Armaanchan @eelchico @GatewayCollects @PokiPair How many of yours got cancelled? Hopefully we both at least get some orders

English

English

@Armaanchan @eelchico @GatewayCollects @PokiPair My order hasn’t been cancelled, been communicating with the seller and they said it should ship within 8 days but we will see…so far so good

English