Pav

2.2K posts

Pav

@Back2futur3

Navigating complexity of life through technology.

Sydney, New South Wales Katılım Mart 2020

334 Takip Edilen124 Takipçiler

In a few years, no one will work and everyone will be rich. Here is how much money you will have:

Everyone will get UEI payments of about $50,000 per year, but that money will be worth many times more than it is today since prices will drop dramatically.

The price of information work will drop by 10,000X or more. For example, work that would take a lawyer a day and cost $5,000 would take AI minutes and cost just 50 cents.

Put differently, $1 could purchase $10,000 worth of services.

Your $50,000 income would buy the equivalent of $500,000,000 worth of services at today's prices.

In a few more years, AI will become even more cost-efficient and you will be able to buy well over one billion dollars worth of services with your UEI income.

Manufactured goods will also drop dramatically in price. Within a few years, prices will drop by 10X, and within a few more years by up to 100X. This is because all the labor will be done by inexpensive robots.

A car that costs $80,000 today will cost $8,000, and eventually $800.

A $500 room in a high-quality hotel will cost $50 and eventually $5.

A $300 meal in a five-star restaurant will cost $30 and eventually $3.

Humanoid robots will initially cost about $3,000 in mass production. As human labor is eliminated across the supply chain, their price will fall to $300 and eventually $30.

Although your $50,000 yearly UEI will remain unchanged, it will buy $500,000 worth of physical goods, and eventually $5,000,000 worth at today’s prices.

English

There is no easy money in this world.

I personally would avoid it. Just look at Birmingham City council putting all there savings with a Bank of Island in 2007 and losing it all after GFC . They also where paying somewhere around 11% . It's a trap and Michael Saylor is sharlatan. Sooner or later it will implode

English

So, @grok — give me investment advice… should I buy bitcoin directly or buy $mstr and these loans they’re offering around it?

Do some deep research please

EndGame Macro@onechancefreedm

The Real Risk Behind a 10% Yield in a 4% World A 10.25% yield looks like a no brainer especially when Treasuries are offering somewhere around 3.5% to 4.6% across the curve. But when something promises more than double the risk free rate, that spread is the market pricing in risk that investors might not fully understand. STRC isn’t a Treasury, a CD, or even a corporate bond. It’s a preferred security issued by Strategy Inc., which means you’re not lending to the U.S. government or even to a diversified company, you’re lending to one firm, on subordinate terms, with no federal insurance, no collateral protection, and no guaranteed liquidity. The fine print makes this clear. STRC isn’t backed by the company’s bitcoin or hard assets; it’s just a preferred claim on whatever remains after other creditors are paid. That’s a massive distinction. If Strategy runs into financial trouble, preferred shareholders are behind the banks and bondholders in line. And unlike a bond, there’s no contractual obligation for the company to keep paying. The 10.25% dividend can be reduced, deferred, or canceled altogether, and it resets monthly so it’s not a locked in yield, just a moving target based on market conditions and company decisions. The dividend is also based on a stated value of $100 per share, not necessarily what you pay in the market, meaning if the share price drops to $90, your yield on paper rises, but your capital is already eroding. This is especially important in the current economic climate. The Fed is signaling rate cuts because parts of the system are weakening. In that kind of environment, liquidity risks rise, credit spreads widen, and refinancing costs increase. Companies offering double digit yields are often doing so because traditional credit markets demand even higher rates or won’t lend to them at all. If a mild recession hits or funding dries up, dividends can be paused to preserve cash, and preferreds like STRC can sink fast. You might collect a few months of high payouts and then find the market price down 30–40% with no buyers in sight. There’s also reinvestment and call risk. If rates fall sharply, Strategy could redeem the preferreds at $100, capping your upside just as safer yields are dropping. And because these aren’t government backed or widely traded, exiting your position may not be easy, liquidity can vanish overnight. The glossy marketing pitch leans on monthly dividends and brand association, but the real equation is yield versus structural risk. That 10% is the market’s way of telling you you’re being paid to shoulder concentrated credit, liquidity, and market risk in a tightening financial system. A 10% yield in a 4% world should make you ask why it exists, not how fast you can get in. The fine print already answers the question, it’s a high risk security dressed up like a high income opportunity.

English

@Lost1million What do you expect to accomplish with this post assuming it's true?

English

I’m going to fucking throw up. Lost that remaining $1k I had. My bank account has $0. I wish I never fucking found trading. I’m posting this so everyone that sees this can convince themselves that this is the fucking devil at work and STOP TRADING. FUCK. ME. FUCK.

English

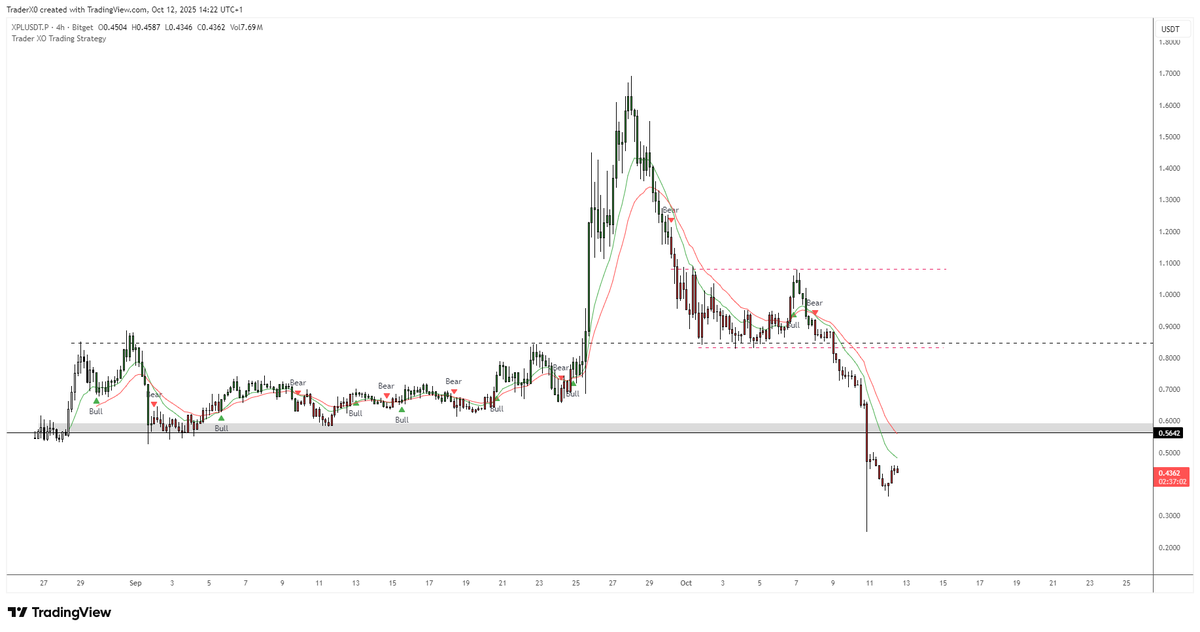

@Trader_XO XPL is the only one that got me . I didn't put that much in it anyway not millions like 99% on CT judging by there account sizes . It was not leveraged and I thought it would go to 1.50 . Now it's a waiting game if it goes to zero so be it .

English

I wanted to follow up on this tweet.

Sometimes the simplest systems or rules are enough to keep you on the right side of the market.

While it’s easy to say this in hindsight and few could have foreseen a cascading liquidation event, my point isn’t about the warning signs, or would have, could have, should have.

Even before the drop, XPL was a clear example of an alt where dip-buying should’ve been avoided and kept me away from the trade - which was stated on my tweet.

A basic trend-following approach would’ve kept traders out of a bad trade that only got worse.

We’ve all made those mistakes before, I certainly have but failing to learn from them will only hold back progress.

I’m sharing this only to help others avoid making the same mistakes, especially when the crowd is advocating for "buy a dip" that turned out to be more than that.

Stay blessed.

XO@Trader_XO

It’s honestly not that difficult. The waiting game is what many screw up. Personal preference: not a fan of dollar cost averaging into a losing trade - I’d rather dca into a winning position.

English

@QuantumSuicider @saylor @Strategy Yes retard I have been called a lot worse as the saying goes it takes one to see one 😉

English

Look you get margin called because you are leverage trading then it's the exchange that stopped you out and profited from your loss . However generally not always exchanges tend to open counter positions to yours to minimise risk .

If you are buying spot then there is no liquidation price until you hit sell at that point you take the loss and some one has to buy your position of you which means that you have lost that money

English

The most important question is

If we all lost money and $19 Billion got liquidated from crypto market

Who the fuck made that money ?

English

@LoveYouAllNFT How do you know he actually made 100 million unless it's been independently verified.

English

@JasonBassler1 Out of all people I have more faith in Elon. He is not perfect, but compared to others I would rather have him owning the wealth. Also it's no coincidence that Elon is richest person in the world. No other human in this world could achieve what he has done

English

Let me get this straight…

The world’s richest man owns Twitter (X).

The second richest wants to buy TikTok.

His heir now owns CBS and Paramount.

The third owns FB, Instagram & WhatsApp.

The forth richest owns Amazon & WaPo.

And no one sees a problem here?

English

It seems every second one on CT has lost millions worth of wealth. I am a little perplexed by this there is no way on earth I personally would have that much money in Crypto even stocks seems risky . Add leverage and you are asking for trouble honestly who ever got liquidated have dug there own grave

English

Will you thrive or die with AGI? Take this test.

AI is advancing fast. Faster than any technology shift in history. Electricity took 46 years to reach mass adoption. The smartphone, 16. ChatGPT reached 100 million in two months.

Studies show that humans handle incremental change well but struggle with exponential change because our brains have evolved for linear prediction.

We’re probing at this situation when we ask: will AI take my job?

No one knows the answer to this question. What we do know: change is happening and it could be more radical than we can imagine. The question is: will you be able to adapt?

Here is a thought experiment that will score you on adaptability. Score low and you will struggle, score high and you may thrive.

Here we go.

Imagine your future existence rests on three principles:

+ Nowhere to go

+ Nothing to do

+ No one to become

That’s it. That’s your life.

Most people feel psychological vertigo when hearing this because it violates the evolutionary code of our species.

Humans are a striving species. We go places. We build things. We become someone.

Our entire civilization and self identity is built on the premise that meaning comes from becoming. Our self-worth is our usefulness.

If your response to this possible future is “No thanks, I’d rather die.” You score low on adaptability and will struggle with change.

If you feel discomfort but are also curious and are open to experimenting, you score high on adaptability and are more likely to thrive.

History shows that adaptability, not intelligence, determines survival.

English

Week ahead

From past experience with large liquidation events, a recurring pattern tends to emerge where price often backfills a portion of the larger moves / wicks, though in this instance, given the scale of the event, probably less so across various alts.

Volume typically tapers off and could remain subdued next week, until demand is established before leading into an up rotation again.

The one caveat to keep in mind is any announcement from “Taco Man,” which could act as a fresh catalyst => reigniting volatility and increasing tape speed again.

Lets see what Monday brings...

English

Well well well my gut feeling saved me ,currently we are at 112 area. I still think it goes lower . Generally speaking market tends to visit or fill this wicks which currently sits around 100k area and I think we will go there soon .

Pav@Back2futur3

This latest PA on BTC has me confused we either bounce 117.500 and continue higher or we go back 112k and I am thinking of ultimatly 96k. It just seems really strange to go where it did and not break the low and sweep the highs. It doesn't make sense for BTC to go lower then 112k tbh with all the etf inflows , but if it does it will fuck so many people

English