@aleabitoreddit how did you perform before this historic run? have you just been doing this forever or is this AI niche your rocket fuel?

appreciate you, changing lives!!

English

Garrett Heator

442 posts

We need to normalize not being on any medications as the default of human existence

Shai hit his signature move Push-off, flop, free throws.

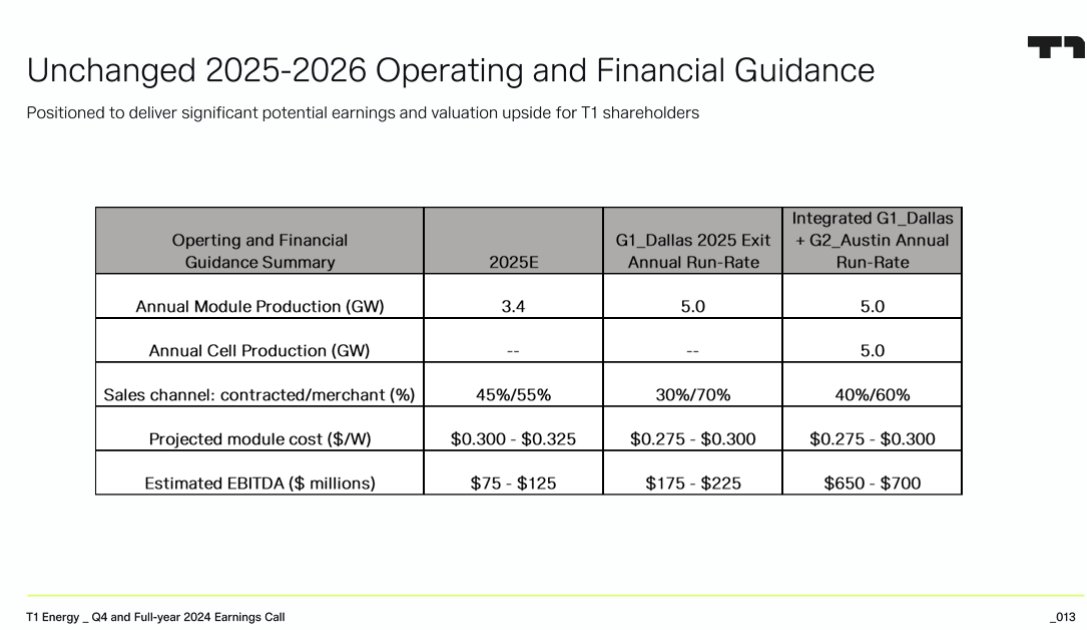

$FREY: Took a quick look at Freyr's pivot from battery developer to solar module and cell manufacturer. $FREY purchased a brand new 5GW US solar module plant (Wilmer) from Chinese producer Trina for $621M or 3.1x runrate EBITDA, which will make them the #3 producer in the USA. Trina will own ~20% of FREY pro forma and will provide various support services as they ramp up the plant. $FREY expects to generate $100M EBITDA in 2025 increasing to $200M once it's fully ramped. They've got 1.5GW already contracted out in offtake agreements. $FREY plans to build a new solar cell plant for $800M of capex, which they expect will generate an additional $475M of EBITDA or a total of $675M EBITDA for both the module and cell plants. $FREY pro forma for the transaction will have 200M shares outstanding, $132M of cash and $545M of debt for a total Enterprise Value of $1B at a stock price of $2.95. If you buy the stock today, you're purchasing the Wilmer solar module plant for about 5x EBITDA with an option on the new solar cell plant and some recovery value from the co selling/leasing the battery production facilities in Europe. $FREY believes that cashflow from the module plant along with new equity and project financing will fund the $800M capex needed for the new cell plant. They're going to detail these plans in the near future. Below is the pro forma cap structure and implied valuation multiples. IF you believe they can ramp up the Wilmer to $200M of EBITDA, at 5x-8x that implies $3 to $6 per share value. IF you believe they can build and ramp up the solar cell plant (with $800M of debt funding) resulting in $475M of add'l EBITDA, at 5x-8x multiples that gets you to $11 - $21 per share. This does not include any potential value from disposing the legacy European battery development/mfg facilities. There's a lot of execution risk here and I have no idea if this team can do it, but an interesting pivot and transaction. The CFO recently bought 130k and 550k shares on the open market. Company presentation here: ir.freyrbattery.com/events-and-pre…

Not exactly! I'm just a tad more familiar with photonic supply chains than I am with energy so I like picking potential winners. Just wanted to introduce $IQE into the equation like i did with $AXTI, so I could do a "Did you Listen Anon?" post 3 months later if it turns out well.

LPKF Laser are kinda interesting. Initial notes are: -> Owns LIDE - only 2-step laser + etch process hitting 5µm vias at 50:1 AR on glass panels. -> Every serious glass substrate player (SEMCO, SKC Absolics, LG Innotek, DNP, Intel) is a customer, partner, or in qualification. -> Their LIDE process is the only one hitting the spec envelope $AVGO/ $AAPL/ $NVDA ASICs actually require? -> €337M MC - seems to be priced as a solar-drag industrial laser co. Not as a chokepoint of the packaging transition. -> Pretty ugly P&L. I started a small position yesterday which I'll build out next week depending on how I feel when the time comes.

if $INVZ closes even half of that valuation gap with $OUST, looking at 10-20 baggers on some strikes. just sayin

It is time for the United States Postal Service to ban junk mail. Unsolicited spam calls are already prohibited by the FCC. Emails are heavily regulated by the CAN-SPAM Act of 2003. Junk mail is the majority of mail, 100 million trees per year. Enough!