Sabitlenmiş Tweet

Neutral

3.4K posts

Neutral

@JanKlan2

“Hard times create strong men, strong men create good times, good times create weak men, and weak men create hard times.”

Katılım Mart 2021

61 Takip Edilen79 Takipçiler

Mark Wahlberg tiene 54 años.

Se levanta a las 3:30 de la madrugada y se acuesta a las 7:30 de la tarde. Entrena cinco días a la semana.

Pero su rutina es completamente diferente a la de cuando tenía veinte años.

Aquí tienes siete cosas que hace a los 54 para mantenerse joven (y cómo puedes ponerlas en práctica):

Español

Now that $HYLN is over 5$ and a billion dollar market cap, Its officially not a penny stock anymore. This means It will attract attention from funds who are not allowed to trade in penny stocks (most of them). Also note that the rennaissance quant fund bought HYLN shares, they are widely regarded as the best quant and usually very early. (they bought $TSLA before the massive runnup) Also, we havent been included in the Russell index but this will probably happen next month, even forcing more buyers. This might become a perfect storm, especially when comparing with $BE valuation which would compare with a $HYLN valuation of 450 which would mean $HYLN has an upside of at least 75x. (but in reality more because HYLN has a better product)

English

@dorbc @NoahKingJr If you live in a simulation, jump off a building and see what happens.

English

Hybrid humans with AGI Neuralink implants with ASI-level downloads per request depending on fields of activity.

On an evolutionary scale, the perfect human body would be designed and also have Neuralink or similar. I think hybrids would be the future. But the current civilization can’t handle that.

Maybe that’s why Musk insists on Mars.

The question here is: If hybrid humans were designed and developed, what are the chances for them to be put first in a simulation?

And if that is logical, how do we know we’re not in a simulation now?

It often feels like a simulation, to be honest. A lot of unexplained facts by scientists are impossible according to current knowledge and laws of physics.

English

@KatanaBets Investing is not as easy as it may seem to others… What do you think about this year 2026 will it be time to go away?

English

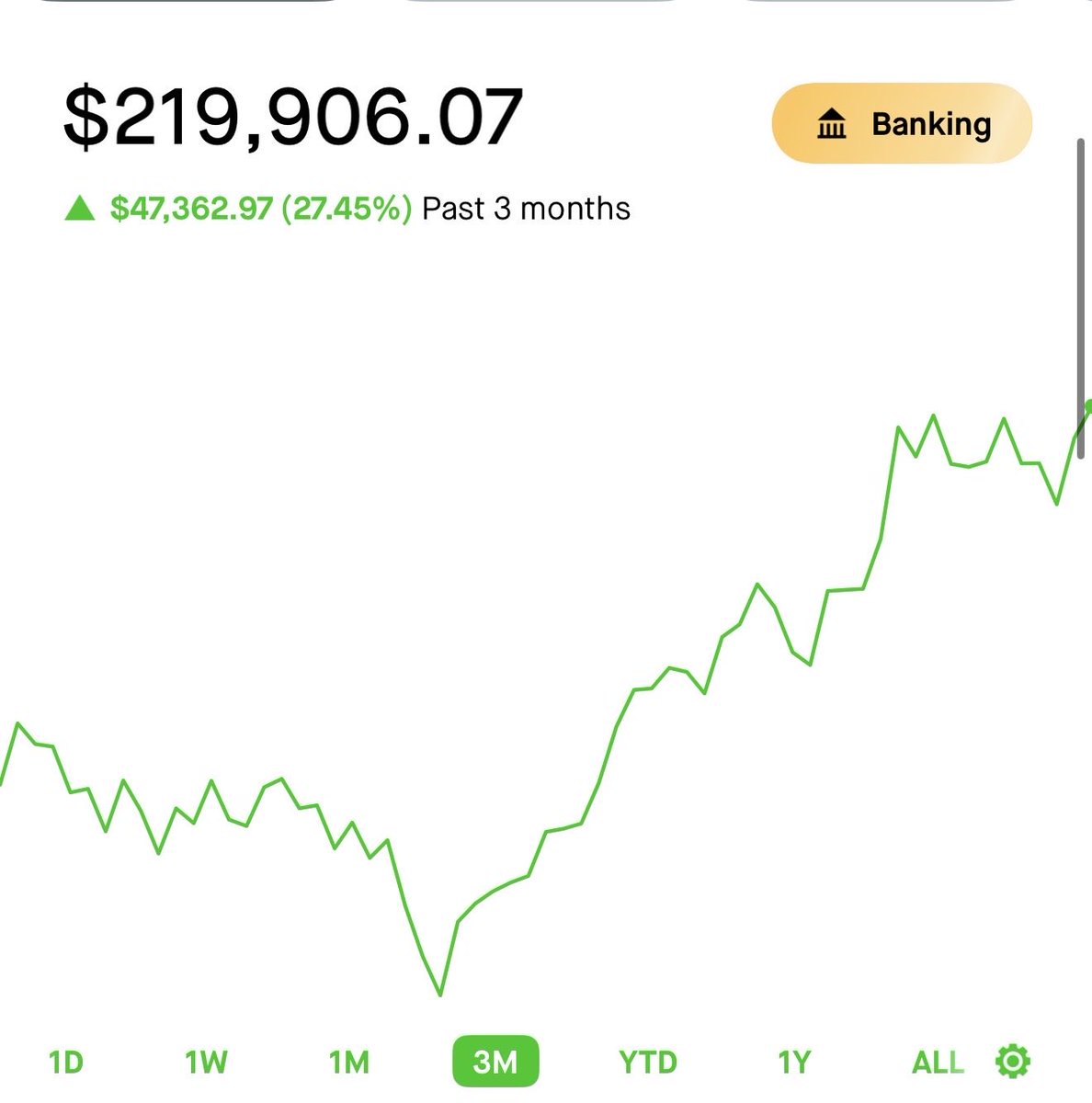

Entered the market in 2018 but wasted a few years trading like a goober, didn’t have the education or experience. Learned some hard lessons early and let the 15k I had just sit in a few boring stocks for some years after that. Came back in January of 2025 after spending way more time educating myself on the market. I was also able to inject more capital I had which brought me up to 80k. I then started selecting companies I wanted to own a part of, and have been working on it since then! This time with a much different and safer mindset and risk tolerance.

English

@LaLaAhOh @AyusoValue But this company will be reborn, they went down low, they loaded their bags and they will go up

English

@AyusoValue $NFE is another case of poor governance, though not of self-dealing. $NFE was a case of BOD not exercising independent oversight of a management who owned a controlling interest in company.

English

Might have found another fantastic long term add that is not a theme I currently have in my portfolio (at least a very small allocation to)

-Expanding margins while priced rather cheap by its own standards (15x P/E, 11.2x fwd)

-Products have absolutely exploded in popularity past few years with lots of further opportunities for growth (gaming sector)

-Durable business model and monster balance sheet, long history of elite ROIC and shareholder value creation

-Rising dividends and large buybacks

-Hasn’t moved as much as it should have this year yet

Can anyone guess the name?

English

@KatanaBets Do you have anything related to uranium in your long-term portfolio?

English

We are, and have been, at that point in the cycle where everyone online is always talking about multi baggers, 10x, 100x opportunities in short order.

I just want to remind you guys that’s not how this works, at least, not short term where most people on X will make and hold their moves.

On average, only ~7 out of 100 traders who are short term focused (year or less) are actually profitable. Don’t get me wrong, that could totally be you, but, I know there’s a lot more than 7 of you reading this who think they are part of that 7.

This is where my value proposition comes in. No matter your amount of starting capital, could be $100, could be 100k. Just focus on buying and holding long term.

Identifying strong businesses with disciplined balance sheets, solid earnings growth, wide moats, and great management, and then buying & holding for the long term, is how you statistically win.

Now am I totally discouraging the fun of doing something like swing trading? No, you can do that, but just use a small percentage of your port to do so. Currently only 2% of my portfolio is in anything that will be held for shorter than 1 year. Less than 1% if you count my other portfolio which is also long term only.

You can take 2% of your port and scratch that little trading itch, while not knocking yourself off course for the longterm. Long term buy and hold strategy ALWAYS wins out, especially with indices.

Do not be led astray by accounts posting how they are up %2000 Ytd during one of the most wild and volatile bull runs ever lol, they cannot repeat that performance YoY no matter what they claim.

FinX and WSB personalities have led so many people off of responsible and profitable courses, it’s a real tragedy.

Anyways if you took the time to read my little rant, appreciate you, stay the course and you’ll be better off than most people. Like literally will be, the fact you’re even here as an active market participant means you’re already statistically more proactive than 85% of the population. With that said, why ruin your special inclination with short term trading? Find your winners and hold them, it’s still just as fun I promise.

English

USA has ChatGPT

USA has Grok

USA has Claude

USA has Gemini

China has DeepSeek

China has Qwen

China has Kimi

China has MiniMax

Europe has?

Indonesia

@justfactsnotbs @Treeshool @CommodMkt What else besides oil companies? gas, uranium, hydrogen companies also ? miner's stocks?

English

@Treeshool @CommodMkt You didn’t read it..buy the oil companies equity that are trading lower today then before the war and the oil spike…have fun with your semiconductor stocks

English

Welcome to the most asymmetric trade in modern financial history.

The thread below lays out why. The opportunity exists because capital has chased the AI trade while ignoring the physical assets AI requires to run — assets that have quietly become the best-performing asset class of the decade. Since October 2020 when we first called for the commodity super cycle: QCI Total Return +217%, GSCI Total Return +205%, Gold +140%. NASDAQ trails at +130%. S&P 500 at +85%. The top three are all commodities. Yet oil cannot get out of its own way while copper and the broader atom complex prints fresh highs . That is the dislocation. That is the trade.

Get long. Buckle in. Hang on for the ride.

Forgive the longer posts in this thread — attempting to mimic my old 10-bullet commodity takes. On to it.

English

$BE is an awesome stock and has had a great run, but im betting $HYLN will be the better investment from this point just because people havent discovered It yet... They just got UL certified and are truly fuel agnostic without downtime and 800VC DC native to power the next gen datacenter without conversion steps!

English

$HYLN

Up 51% since this post!

Up 115% since I first started talking about it on my page.

In my opinion, the party could just be getting started here. I could do a longer write up here later if y’all wanted. NFA.

Katana@KatanaBets

My secret gem $HYLN is making new YTD highs today Most of you may remember this from the SPAC bubble and how they were making CNG trucks. Not anymore, the stories different now. They ditched the trucks and focused entirely on building the engines that will help power this buildout (generators) among other applications. Years of R&D later, and they are about to reach commercialization in one of the biggest power/grid buildouts ever recorded in history. They have multiple advanced contracts with the Navy and Army for their KARNO linear compressor. They have been awarded mission critical readiness status multiple times so you know this product is REAL. It delivers fantastic efficiency for all applications involving power generation. Do not sleep on this company because of their history. The thesis has very much changed since then. (Full transparency I own 1250 shares at a 1.28 cost basis. NFA!)

English

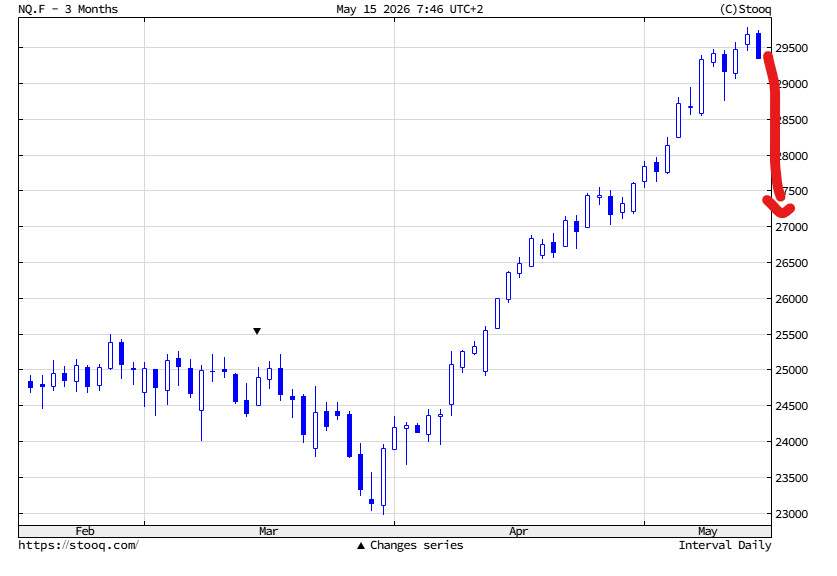

UWAGA na Nasdaqa to może być bardzo szybka i bolesna nauka spekulacji :) dla fanów wiecznej hossy

Taka sama jak niedawno na złocie .. małpy się po prostu nigdy nie nauczą

Polski