Jonathan Baire יונתן

1.6K posts

Jonathan Baire יונתן

@JonathanBaire

Entrepreneur, juggling three seven-figure companies with grit and vision! 💪🔥 #EntrepreneurLife #Purposedriven

US/Africa Katılım Eylül 2017

2.9K Takip Edilen308 Takipçiler

@88magalhaes @aleabitoreddit 😂 😂 😂 thanks for putting that out there! This tells me everything I need to know.

English

@aleabitoreddit Also $IREN has Mike Alfred on the board. Can't really have a largest red flag than that.

English

Do you guys think there’s only $5,650,000,000 dilution to go with $IREN?

Very surprising that people haven’t switched to $NBIS or other names if you’re long Neoclouds.

One already has confirmed funding with $NVDA + convertibles from institutions.

The other is likely actively selling new shares on the open market to get funding off retail shareholders.

The sad reality is:

$IREN simply cannot monetize the rest of their capacity without using that. It’s not “optionality”.

Financial structure nuance matters when you’re choosing winners for equity appreciation.

Nebius is clearly has the better financing structure and this is already showing up in YTD returns.

Serenity@aleabitoreddit

$IREN filed to dilute $6,000,000,000 at a $11.7B MC. That is not noise. This is Iren's way to monetize their 4.5GW capacity by selling all those new shares onto the open market. If you want some history on how this turns out: Look at $BKKT that crashed 99% with Mike and $IREN board of directors history with excessive ATMs. Or his recent company $ASST. It’s accretive to the company and executives: Because it wipes out all retail shareholders and they can always issue SBC. So they don’t actually care what stock price it needs to be at to sell. After they’re finished, they have $6B in new cash to use for scaling without paying interest. But the reason why convertible notes with interest, and $NVDA funding balance sheets is much better for retail capital: Is because it doesn’t wipe out retail equity to achieve this. Because at this point $IREN looks like the $AMC of datacenters with a dwindling moat, and looming $6B in shares sold into the open market. Reason I post about $IREN is because - people dismiss a $6B ATM as “Noise” - it’s one of the most popular retail “buy the dip” companies that they’re buying into a $6B dilution machine - people still don’t understand the risk at all. - the amount they have now is not enough to finance GPUs/GW capacity monetization. - they likely will have to use the ATM, it’s not “optionality” Again: I have zero positions in the company. I’m just warning retail investors that this ATM structurally wipes out your equity appreciation by how structural mechanics of $6B+ ATMs work. Because $IREN likely needs to sell new shares at any price to monetize their GW, otherwise there would be zero need to file it. Executives actually don't need to care because they can make up for stock price dropping by issuing SBC like $SNAP. If you have to wonder if your equity gets wiped out from an excessive ATM: There are better longs out there than $IREN.

English

@JonathanBaire 540 on meta looks good 375 on TSLA looks good - any strike you like really cause we r moving up here as

English

@Maximus_Holla Brad Jackobs must be onto something.

Are taking some chief?

English

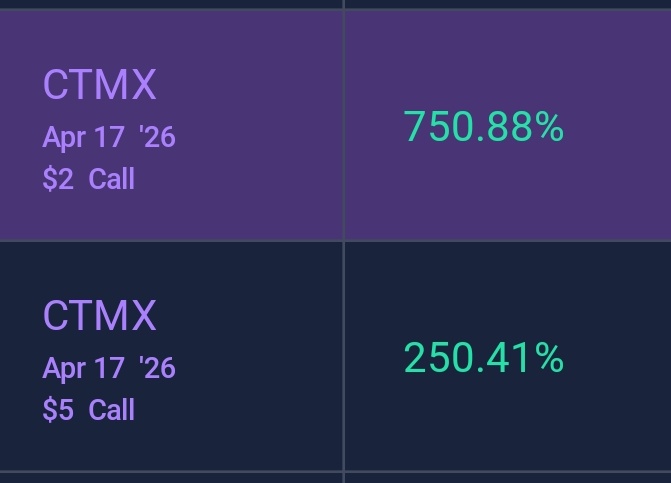

$NEXT 7c hitting $1 deep ITM, i see this was traded as low as 1 cent 😅

zohm@zohmbastic

$NEXT trimming a couple more 7.9s

English

@aleabitoreddit @rioferdy838 Any update on this chief?

English

@rioferdy838 I said they were good proxies to know how well a general segment was doing but I personally wouldn’t chase $BE or $CLS after a 25% increase. But if you were to enter positions would be smart to DCA

English

Macro Analysis:

Focus Areas: Flows · Proxies · Seasonality · Positioning

Setup :

_

Neocloud: $NBIS · $IREN · $CIFR · $DGXX

Connectivity: $ALAB · $CRDO · $CLS

Robotics: $KRKNF · $ONDS · $RR

National Security: $RKLB · $MP · $KTOS · $CCCX

Energy: $FLNC · $EOSE · $TE · $SEI

Semi: $TSM · $AMD · $NVDA · $MU

_

Part 1 - Institutional Flows

Into October–November, hedge funds sell underperformers to lock in tax losses and rebalance positions.

This creates mechanical downside pressure from tax-loss harvesting by rotating losers YTD and rotating into winners. Once this selling ends and wash sale windows expire, institutions and quants often buy back these oversold names in uually mid tolate Dec or early January.

The setup above shows every stock that up YTD, usually you want to position aggressively into these EOY by tax-harvesting losers and scaling into positions that win.

Stocks like $SNAP, $ETOR, $DRFT, and others that might be undervalued fundamentally is largely affected by institutional positioning. It's better to go with the flow rather than fight against it unless you want to wait out 2-3 months and accumulate during this time (which is a valid strategy as well).

Part 2 - Proxies

Neocloud - We've seen $META x $CRWV deal, $WULF x $GOOGL x Fluidstack JV, $MSFT having more compute demand from OpenAI, and others, which is extremely bullish for the whole Neocloud sector. So sector will likely continue to outperform.

National Security - We've seen Trump take stakes into critical material companies like $MP and start looking into backing more national security risks such as quantum names like $RGTI, $IONQ, and others. This is generally positive for other names like $RKLB or other national security buildout across the board.

Semi - $TSM is the best proxy for semiconductor buildout and demand and their forward revenue projections are absolutely insane. People make the mistake of looking at Fab cycles from $ASML but it's not the right proxy.

We can go on with $CLS as a proxy for connectivity or $BE earnings for energy, etc.

But generally, you can get a good idea on what sector is outperforming or is likely to do well based on other companies in the area.

Part 3- Seasonality

November and December are the strongest months for equities.

This one is more psychological because of sentiment. But also partly mechanical because funds “chase performance” to lock in annual gains after they redeploy cash from tax loss harvesting in October.

Part 4 - Positioning

This is purely based on your own risk level. For example, with a smaller $100k portfolio you can be fine positioning aggressively like:

25% $NBIS, 10% $IREN, 10% $ALAB, 10% $CRDO 5% KRKNF, 5% FLNC, 5% TSM calls, 20% misc or low beta (eg. $HOOD), 10% cash.

If you want to be a degen, now is probably the best time to do so though. I gave an example ETF earlier on how you can position but I typically don't recommend concentrating your whole portfolio into single stocks.

There are other segments I didn't mention like Fintech/Commerce ( $HOOD, $SOFI, $DLO, $SEA) and so on but you can plug and play.

Part 5 - Macro

People worry about AI bubbles, but bubbles pop when Federal Reserve tightens, and we recently got a correction in a lot of bubbly names. But now we're going into 2 more rate cuts and government re-opening (which is such a weird catalyst but it is one).

We have a 86% chance of 2 more rate cuts which is insane (as per Polymarket). And, with a triple rate cut, growth and small caps tend to surge as cheaper money and debt easing spark risk appetite. Floods of liquidity will eventually flow into growth stocks and small caps.

_

This is just the general trend, you can pick your own basket of stocks, or whatever you feel is great. I'm personally the most bullish on Neoclouds, AI buildout and positioned more heavily toward asymmetrical picks but to each their own (eg. people have large positioning in energy/robotics, or fintech)

Also something to note is that even if something goes up 500% like $RGTI, make sure the rise backed by fundamentals (eg. Neoclouds, forward revenue)

But generally if you had to take one piece away, being aggressive into two more rate cuts, end of year seasonality, and consolidating into winners is the best time ever for it.

Serenity@aleabitoreddit

The NeoCloud Thesis: Hyperscaler Capex Funnel Why I'm putting $1.5M+ into Neoclouds, and why this might be a 200-300%+ return. 🔹 Buckets Mag7 contracts: $CRWV, $NBIS ✅, $WULF, $CIFR ✅ With compute: $IREN ✅, $BITF Speculative: $WYFI, $GRRR ✅, $SLNH Miners pivoting to HPC: $RIOT, $MARA, $CLSK, $HUT Thesis: Mag7 is AI compute strained, by design from $NVDA. Trillions of capex that normally flowed through AWS, MSFT Azure, Google Cloud for traditional compute, will now funnel into NeoClouds when they cant handle new AI loads from Anthropic, OpenAI, Gemini, etc. This is a once-a-decade opportunity, similar to the GPU arms race that made $NVDA a $4T company, on who powers the infra for AWS/Azure/etc for the next 5-10 years. NBIS (17B from MSFT), CIFR / WULF (3B from GOOGL), CRWV (backstopped by NVDA) are all scaling hundreds of percent (NBIS went from 150M quarterly revenue to likely 1.5B+) with 60-80% gross profit margins. This revenue growth is almost unheard in history. It's mainly because it's the wealthiest hyperscalers funneling capex into tiny companies. NVDA / TSM (2022->): GPU for hyperscalers CRDO / ALAB (2024 ->): hyperscaler wins -> parabolic growth. NBIS/CIFR/IREN/etc (2025 - ) AWS/Azure/etc. -> parabolic growth from AI compute This is how you get hundreds of % in return, not value investing in Paypal. Momentum riding the next generational companies. So bear thesis usually involves around - Execution Risk (before it was more speculative, now companies like NBIS have 4B+ to execute) People can always worry about execution but Microsoft or Google would not be signing such large 5-10 year contracts without their own DD. - Large interest rates (mainly looking at you CRWV), that's why NBIS, CIFR, and others have potential amazing returns. You have 4B+ in funding for $NBIS at $138+ a share (when it's $107 now). And funding for $CIFR at $16+ a share when it's $11 now. ABOVE current price funding is a bullish tell. - GPU depreciation (valid concern but it's almost like oil, even older models kept their value and still deliver equity). - Valuation (I still think we're just getting started. If NBIS scales to 6B rev next year 75% gross margin), 26B marketcap is extremely tiny. - NVDA potentially launching their own GPU-as-a-service and directly competing. Right now these Neoclouds are NVDA's answer to preventing concentration risk to Azure/AWS/etc. - Custom hyperscaler chips like TPU, Trainium. But likely years away, since they're still begging for NVDA compute and signed 5Y-10Y contracts. Regardless these neoclouds like Nebius are really undervalued relative to forward revenue/gross margins. We're still very early. Make sure to ride the Neocloud wave like Crypto/TSLA with Trump election or NVDA with OpenAI release. Of course this is highly speculative and I wouldn't YOLO full port calls, but Risk vs. Reward on these little 5-20B neoclouds powering AI workloads for Google/MSFT/etc, the cash cows of Mag7, is worth it. (Trade time Horizon: 8m - 1 year.) This is the single best asymmetric AI infrastructure trade for 2025-2026.

English

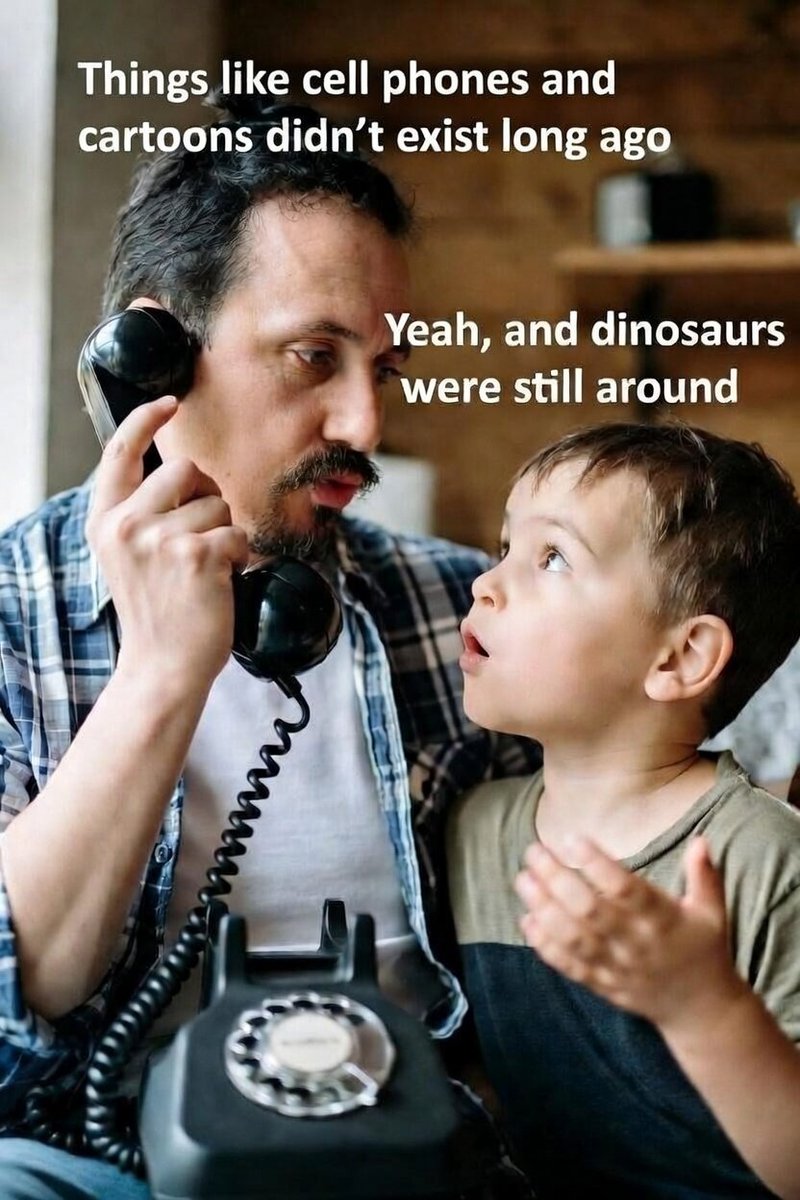

Explaining to my son that many things we have today didn't exist before... For example, that a long time ago, there were no cell phones or TV.

I tell him that when I was a kid, we had TV, but not all the cartoons he can watch today...

Then he asks if dinosaurs were still around 😬..

End of story 😂

English

@Sir_Kory Thank you for this insightful piece. It has strengthened my conviction.

English

$POET

Let’s 🧐 at the latest developments of this company 3 months later.

POET Technologies and 2026 Catalysts

The transition from technical validation to commercial scalability.

At the heart of its value proposition is the Optical Interposer, the only platform capable of integrating electronic and photonic components directly on-chip, drastically slashing the costs and power consumption that currently bottleneck modern AI infrastructure.

Key Catalysts for 2026:

OFC Conference (March 16-19):

This is the main event.

Live demos of Blazar™ and Starlight™ for hyperscalers like Microsoft, Google, and AWS serve as the ultimate market confidence test.

POET recently received a 4.5 "Elite Score" from Lightwave for its Teralight 1.6T engines, which will be officially awarded during the event.

Earnings and Revenue (March 30): Focus is shifting from R&D to top-line growth.

Revenue is expected to rise (estimates around $0.62M) alongside a significant reduction in burn rate compared to the previous year.

Capital Management:

With $150M raised in January, the company has effectively eliminated short-term liquidity risk.

Institutional interest is surging, with firms like Morgan Stanley and Goldman Sachs notably expanding their positions.

Partnerships and Design Wins: Official integration announcements into major hardware players or hints of collaboration with networking giants would signal the shift from a "speculative bet" to an industry standard.

Summary:

2026 is the year of commercialization.

As energy efficiency remains the top priority for AI data centers, POET holds a unique strategic advantage.

Do as always your DD 😉

NFA

#stock #StockMarket

#investing #finance #trading

Sir Kory@Sir_Kory

$POET easy 5$ incoming and well over in the near future. Not financial advice. #stock #StockMarket #StocksToWatch #Investing #market

English