Finneko@finneko_prgrm

🚨 Le Venezuela, le Groenland, l’Iran… ça commence à faire beaucoup de géopolitique d’un coup mais contrairement au premier pays nommé, les choses risquent d'être beaucoup plus délicates.

🇮🇷 Les protestations internes en Iran fragilisent le régime et Trump laisse planer la possibilité d’une intervention qui pourrait être décidée mardi prochain. Les questions qu’on m’a récemment posées sont les suivantes : est-ce qu’il veut en finir avec les mollahs et quel impact sur le pétrole ?

🤷♂️ Ma réponse est assez claire. Il ne cherche pas à renverser le régime iranien par une guerre classique car une intervention directe contre l’Iran serait coûteuse, imprévisible et détournerait l’attention du vrai sujet stratégique. Par contre, accentuer les fractures internes, maintenir une pression économique maximale et laisser le régime s’user de l’intérieur, c’est peu coûteux et très cohérent avec sa doctrine. L’objectif n’est pas d’exporter la démocratie, ici, on veut affaiblir durablement la capacité de nuisance régionale de l’Iran.

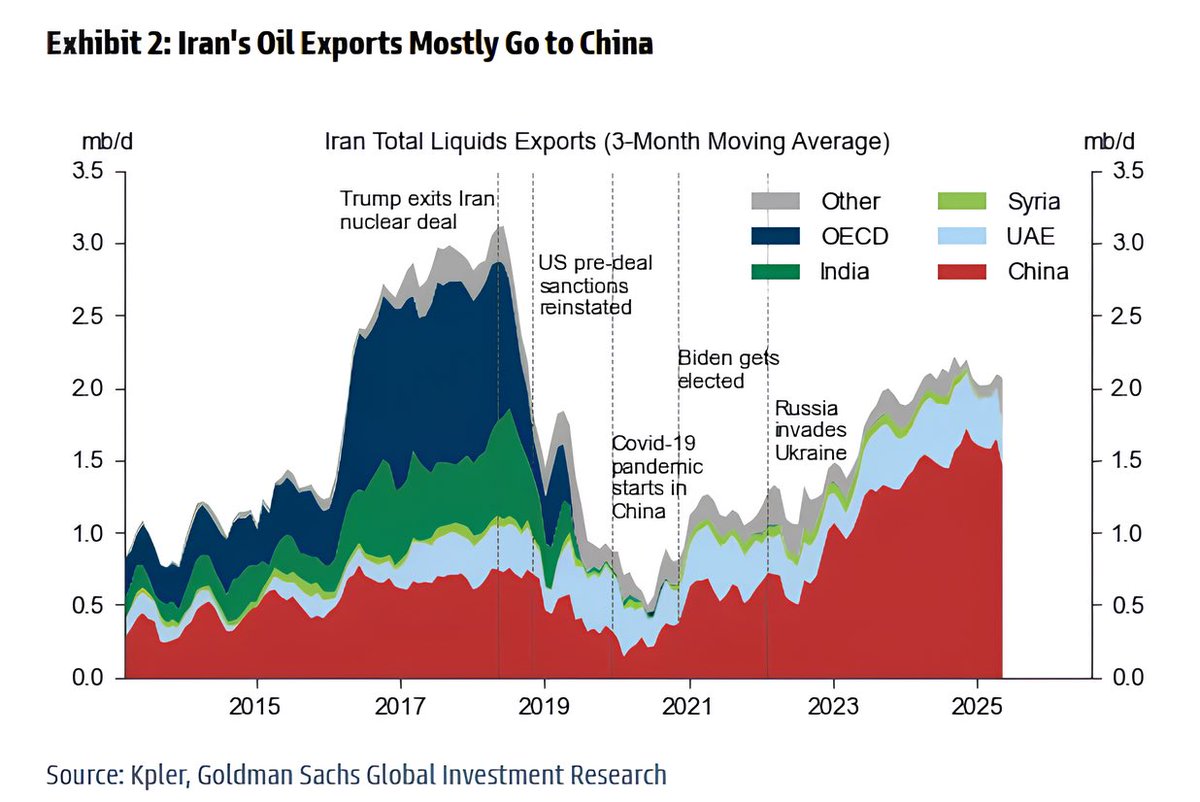

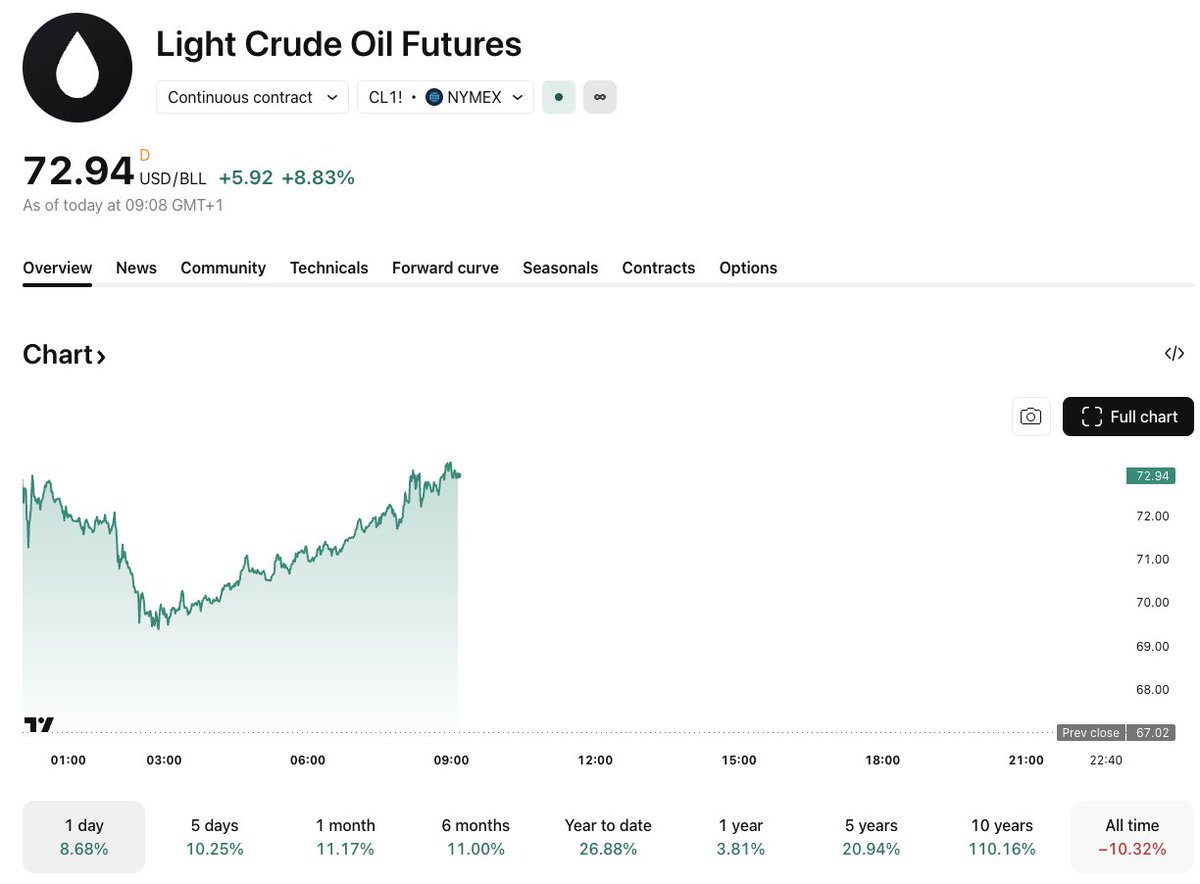

🛢️ Pour le pétrole, je vous invite vivement à lire mon tweet attaché car ce sera toujours la même histoire avec cet actif. Le vrai risque n’est pas tant la production iranienne que la prime de risque liée aux détroits, aux réactions en chaîne, aux sabotages indirects. La peur peut faire prendre plusieurs dollars au baril mais, à moyen terme, Trump n’a aucun intérêt à avoir un pétrole durablement cher puisque son objectif est de retrouver une essence pour les américains a 2 dollars le gallon avant les midterms. et on est encore loin du compte ($2,92 à ce jour). Surtout, un baril élevé, c’est de l’inflation importée, une politique monétaire plus contrainte et des conditions financières plus dures. Tout l’inverse de ce qu’il veut avant une rivalité prolongée avec la Chine.

🧐 Donc ce qu’on observe, et ce que je pense qu’on va continuer d’observer, c’est du stress géopolitique contrôlé. Beaucoup de menaces, beaucoup d’ambiguïté stratégique, un durcissement discret sur les circuits énergétiques iraniens mais sans franchir les lignes rouges. Le Détroit d’Ormuz est l’exemple parfait : tout le monde peut menacer, patrouiller, communiquer mais personne n’a intérêt à une fermeture ou à une escalade majeure. Ce serait un choc pétrolier mondial et un cadeau stratégique à la Chine.

🤔 Je peux me tromper car Trump n’est pas toujours prévisible mais le prochain move, à mon humble avis, ne sera pas un missile. Ce sera de continuer à faire croire qu’il pourrait y en avoir un tout en resserrant l’étau économique et en désescaladant ailleurs pour compenser. Iran sous pression, Ukraine plus calme, énergie contenue et inflation sous contrôle, une gestion fine de la bande passante stratégique.

On gagner du temps, on complique la vie de l’adversaire principal qu’est la Chine et on évite les erreurs irréversibles. Trump avance tranquillement, en toute impunité.