Marzevine retweetledi

Marzevine

3.7K posts

Marzevine

@MuammarZaky14

just a young man who like crypto, stock and macroeconomics 💰💵

Katılım Şubat 2022

215 Takip Edilen87 Takipçiler

Marzevine retweetledi

Marzevine retweetledi

Marzevine retweetledi

Yen is telling you the crude selloff may only be temporary relief.

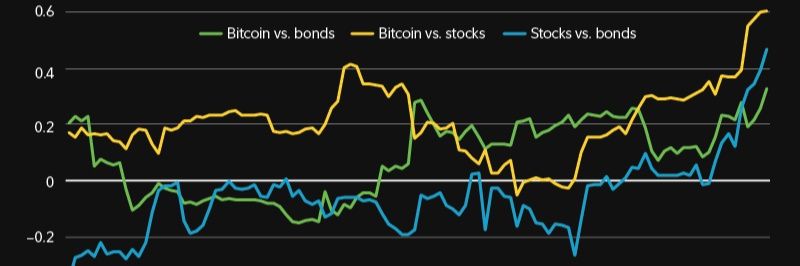

Oil dropped nearly 5%, but USDJPY is still not showing real easing.

For an energy-import dependent country like Japan, a sharp fall in crude should have given the yen some breathing space.

But it didn’t.

That means the market is not fully buying the oil dip.

The pressure is deeper, dollar demand, reserve stress, higher yields, and fragile global liquidity.

If yen refuses to strengthen even when oil falls, the message is clear:

Macro pressure is still alive, and the easing in crude may be temporary.

English

Marzevine retweetledi

Asbun..

Long run pass through Indo paling buruk di ASEAN, 1% depresiasi Rupiah translate 0.69% ke CPI di periode yg sama..

Susi Pudjiastuti@susipudjiastuti

Betul 👍👍👍👍👍Pak Presiden @prabowo

Indonesia

Marzevine retweetledi

Defisit APBN sd 30 April 2026 sebesar Rp164,4 T. Dinarasikan membaik dari Maret. Padahal yang terlebar kinerja April selama 10 tahun terakhir. Secara rasio atas PDB yang 0,64% pun tidak terbilang baik untuk kondisi 4 bulan realisasi. Narasi APBN telah membaik jelas berlebihan.

Indonesia

Marzevine retweetledi

Tokenized assets have never been more popular.

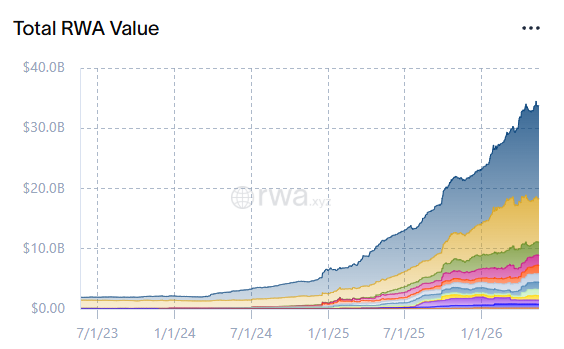

The distributed asset value of real-world tokenized assets is now up to a record $33.8 billion.

This represents a +1,600% increase over the last 2 years and adoption is only accelerating.

Growth in these assets gained momentum after onchain platforms like Jupiter began listing tokenized assets through partnerships with Securitize, xStocks, and Ondo finance, prompting +34% week-over-week volume growth.

Meanwhile, Bloomberg reported this week that the SEC is leaning toward allowing the trading of tokenized assets in a "surprise move."

This would mark one of the US' biggest shifts into crypto infrastructure yet.

Tokenization is taking over.

English

Marzevine retweetledi

Exploding Rates and the Stress Test for the Paper System and the reason you should own Gold.

When interest rates explode, the story is bigger than higher EMIs, higher mortgage rates, or more expensive loans.

The real story sits much deeper.

The foundation of the modern paper system is being stress-tested.

For decades, modern finance rested on one simple belief:

Long-duration debt was safe.

Government bonds were safe.

Mortgage-backed securities were safe.

Bank bond portfolios were safe.

Pension fund assets were safe.

The collateral behind the global financial system was safe.

Then rates started rising fast, and the belief began to crack.

A bond paying 1–2% looks weak when the market demands 5–6%.

A 30-year mortgage written at 3% turns into a burden when new money costs 7%.

A bank holding long-duration paper watches its “safe assets” fall sharply in market value.

The borrower might still be paying.

But the lender, the bank, the pension fund, the MBS holder, and the institution holding the asset are left sitting on the loss.

This is the hidden damage of exploding rates.

And here is the part most people miss.

Under a hard-money system, many banks would have already failed.

Hard money does not allow endless liquidity injections.

It does not let losses get buried forever.

It does not rescue broken balance sheets with newly created currency.

It forces losses into the open.

Fiat works differently.

Losses are delayed.

Losses are hidden in accounting.

Losses are moved into held-to-maturity books.

Losses are managed through central bank facilities.

Losses are diluted through inflation.

And over time, losses are pushed onto the public through currency debasement.

So the system survives.

Not because the losses are gone.

Because fiat gives the system a way to avoid admitting the full loss today.

This is why gold matters.

Gold has no duration risk.

Gold has no counterparty risk.

Gold has no refinancing risk.

Gold is not someone else’s liability.

Gold is not printed to rescue a damaged balance sheet.

When rates explode, the world begins to realize many “safe assets” were safe only in a falling-rate environment.

Once the rate cycle turns, those assets start behaving like risk assets.

At that point, gold becomes more than a commodity.

It becomes balance sheet protection.

The real question is not whether the financial system has losses.

It clearly does.

The real question is how those losses get absorbed.

Through defaults?

Through inflation?

Through liquidity injections?

Through financial repression?

Through currency weakness?

Through central banks forcing real rates lower again?

History shows fiat systems rarely choose honest liquidation.

They choose dilution.

This is why exploding rates create one of the strongest structural reasons to own gold.

Not because gold pays yield.

Because gold protects wealth when the yield-based paper system starts feeding on itself.

English

Marzevine retweetledi

Negara yang secara teknologi dan manufaktur merupakan direct kompetitor-nya US.

Dengan level setinggi itu pasar sahamnya di-diskon setebal itu.

Tiongkok adalah laboratorium paling nyata bahwa Listing-Venue sangat mempengaruhi cara investor memvaluasikan sebuah perusahaan.

Indonesia

Marzevine retweetledi

Coba lihat ini baik-baik, kadang-kadang musuh itu malah merancang supaya dibenci lebih besar lagi.

Bukankah ini strategi perang yang membuat kita sibuk membenci lalu akhirnya ga ngapa-ngapain.

Pak Mahmud kan anti isreal dan anti AS lalu justru dikondisikan jadi pemimpin Iran.

Kadang-kadang yang kita benci, justru membuat kita lebih benci dengan pernyataannya agar kita sibuk membenci dan tak mengerti aliran uangnya kemana.

Apakah saya masuk akal?

So berhentilah membenci dan mari kita lihat duit lagi, kalau kita benci duit, padahal duit itu jujur sekali, membongkar aib orang cara menghasilkan duitnya, masak gaji 20 juta motornya Harley, kalau kita benci duit, padahal duit itu jujur sekali, maka kita yang salah.

Money is honest. Emas adalah uang. Selain itu adalah utang.

Kata Emas boleh diganti sebagian dengan Bitcoin setelah Tiongkok adopsi.

Trita Parsi@tparsi

OMG! While Reza Pahlavi was pushing the US to bomb Iran, Trump and Pahlavi's main sponsor - Israel - had already planned to install someone else in Iran. None other than Mahmoud Ahmadinejad! nytimes.com/2026/05/19/us/…

Indonesia

Marzevine retweetledi

ADP: pertumbuhan gaji swasta meningkat cepat pada akhir Apr dan memasuki beberapa hari pertama Mei karena rata-rata bergerak 4-minggu naik menjadi 42.250/mgg atau ~169rb/bln; untuk semua pembicaraan tentang pemutusan hubungan kerja massal, itu belum muncul dalam klaim UI dan jelas sekali tidak muncul di sini:

Pekerja swasta naik kencang walaupun kata media banyak PHK.

Hmm….. antara media dipesan pemerintah atau Antoni minta jabatan kepala BPS lagi kek dulu.

Saya terus mengatakan ekonomi AS kontraksi-kontraksi, PHK = krisis keuangan 2008, utang ATH, Kartu Kredit ATH, dan banyak lagi yang saya jelek-jelekin.

Lalu laporannya Antoni merujuk pada datanya, ternyata jumlah pekerjaan swasta naik dengan cepat berikut gajinya.

Data apa yang bisa membuat kita independen dan menjadi kebenaran?

“Crowd is always wrong, kerumunan itu duitnya dikit”

Mirip kan sama Myanmar? 😆😆😆

E.J. Antoni, Ph.D.@RealEJAntoni

ADP: private payroll growth accelerated at end of Apr and into first couple days of May as 4-wk moving average rose to 42,250/wk or ~169k/mo; for all the talk of mass layoffs, it hasn't shown up in UI claims and it's certainly not showing up here:

Indonesia

Marzevine retweetledi

Marzevine retweetledi

Crazy times looking back at it.

70 to 80% of the portfolio still concentrated in BUMI, FILM, ARCI, TINS, and ASSA.. then early February, aggressively calling FX dealers for USD! NOW!!

Bold call.

All praise belongs to Allah alone.

Cheytax Management LLC@Cheytax_1

@NotYetCapital That line would’ve worked 3 months ago, but today it’s off. See the chart, USDIDR weakness on the domestic factor is worse than the 1998 collapse. - The good thing is, our gov might finally learn a thing or two about how bad policy always ends with a kaboom.

English

Marzevine retweetledi

JUST IN: 🇺🇸 SEC prepares to allow blockchain-based tokenized stock trading.

English

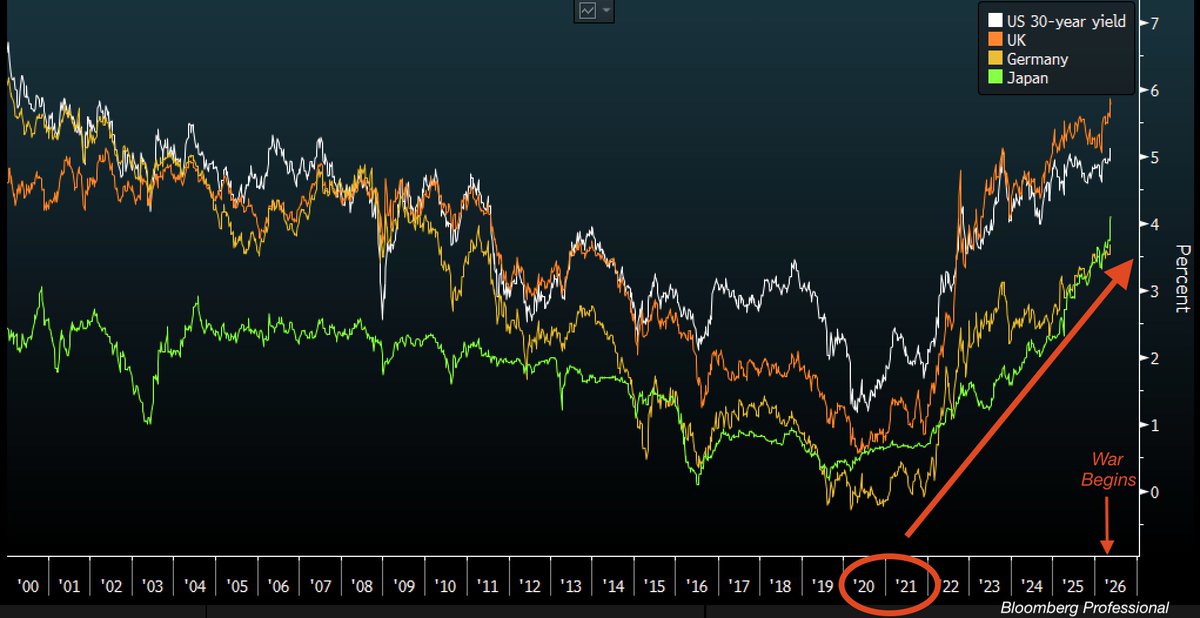

Marzevine retweetledi

Good morning.

Yields on government bonds did not start rising 'because of the War'. They, in fact, began to skyrocket higher after massive central bank money printing in 2020/2021 and continue higher because of relentless government (deficit) spending.

Have a great day.

English

Marzevine retweetledi

Why did we say in our letter that value names could generate seriously outsized returns if short selling were available in Indonesia?

Take a look at the KOMPAS100/JCI ratio. In a bull market, a steepening ratio is normal (two red squares). Why? Because JCI contains more than 900 stocks, while KOMPAS only holds around 90–110 names.

JCI naturally moves more aggressively because small and mid-caps inside those 900 stocks can quickly evolve into large caps. Names like $MORA are a perfect example, once mid-cap, now among the largest by market cap.

But today, JCI is already in bearish territory. Logically, if the market is weak, names like MORA or BREN should get hit harder, dragging JCI market cap down more aggressively than KOMPAS.

Instead, what we've seen since mid-February is the exact opposite (red arrow). KOMPAS been underperforming JCI, causing the ratio to steepen further.

In other words, the weakness in the JCI is no longer just about speculative names like MORA or BREN.

The pressure is shifting toward heavyweight blue chips like BMRI, BBNI, and BBRI. Not just one major name. Not just several. But almost the entire class of legendary Indonesian blue chips getting sold together.

That's exactly why value names could create extreme return dispersion if short selling existed here.

English

Marzevine retweetledi

Sama tolong gmn passive funds works 😔

Apa itu concentration risk di passive funds 😔

"MSCI deletion, capital hasil deletion dimasukin ke yg masih ada"

Apa gak digampar itu sama bosnya sortino rationya ancur2an 😔

Sarjana Eksu@SarjanaEksu

Kalian bearish karena news flows jelek, rupiah melemah, dan outflow MSCI sih gw pahami Kalian bullish karena pada banyak banget yang nebar fear, IHSG turun 26%an, dan kondisi terkesan kayak mau begini terus selamanya sih juga gw pahami TAPI KALAU KALIAN BILANG HANYA BI YANG BERTANGGUNGJAWAB UNTUK NILAI RUPIAH ARTINYA KALIAN HARUS TINGKATKAN LITERASI DENGAN MEMAHAMI APA ITU CURRENT ACCOUNT, BALANCE OF PAYMENT, CREDIT SPREAD, FOREIGN DIRECT INVESTMENT FLOWS, POLICY TRILEMMA, REAL INTEREST RATE DIFFERENTIALS, SOURCE OF GOVERNMENT FINANCING, ETC ETC

Indonesia