z

70 posts

@PawlukZenon @ThePoorBG @BrownMarubozu Happy to send him an email. Do you have a template email that I could try-use?

English

$ACD.TO has one more deal after the sale ⬇️ before they can refinance the debt. The banks gave them until the end of March but will likely extend if needed. Before then we should get an update with Q4 results. The next logical step is an MBO as the returns are compelling.

BondIt Media Capital@Bondit_film

"MEP Capital has closed a majority stake acquisition in BondIt Media Capital, the independent film and television financier." Full Variety article: ow.ly/7mzb50YpjFq

English

@chesir3cat @ThePoorBG @BrownMarubozu David@oakwest.ca might be worth reaching out and pledging your support for preserving minority shareholder value through a complete sale of the Canadian platform.

He owns a quarter of the equity but only $3mm in subordinated debt and appears to want out per resignation.

English

@ThePoorBG @PawlukZenon @BrownMarubozu I wonder how much he cares about his reputation? Seems hard to try a debt for equity swap and not end up making a bunch of enemies.

English

@ThePoorBG @chesir3cat @BrownMarubozu Beutels desire (clean sale) gets us $3 in immediate cash.

Hitzig plan gets our shares likely diluted by half (if they covert debt to equity at current share price) and we are passengers in a sub-scale operator until they take it private for peanuts.

English

@ThePoorBG @chesir3cat @BrownMarubozu Problem is more we fuck around and wait the more the ice cube melts.

English

@chesir3cat @ThePoorBG @BrownMarubozu I directly asked the CEO months ago if once the US assets are sold if his family/ the BOD is open to a sale of the Canadian platform and he answer was "yes it is."

So no we see. I own 50k shares that I acquired on the thesis they sell. So now I get $150k or diluted shitco shares

English

@PawlukZenon @ThePoorBG @BrownMarubozu Reading the tea leaves it seems like he’s going to try to screw us. Hopefully I’m wrong

English

@chesir3cat @ThePoorBG @BrownMarubozu Even a conservative napkin math gets $3/ share in a portfolio sale after wind down costs. Canada book is the best asset and the US stuff sold at or near book.

So how would diluting common equity to near zero in a refinancing be beneficial.

English

@chesir3cat @ThePoorBG @BrownMarubozu Argument would be made refinancing is done to preserve Hitzig operational legacy instead of selling Canadian platform to preserve value of common equity.

Unless Hitzigs pull something out of a hat I can't foresee, I can't see how they'd argue a refinancing is beneficial...

English

@chesir3cat @ThePoorBG @BrownMarubozu My understanding is under Canadian corporate law, former directors remain bound by ongoing obligation of confidentiality regarding non-public corporate affairs.

Once a public refinancing proposal is made he is now freed to use his 25% share block to protect Oakwest capital.

English

@PawlukZenon @ThePoorBG @BrownMarubozu Wouldn’t it be more appropriate for them as board members to state that publicly?

English

@chesir3cat @ThePoorBG @BrownMarubozu Maybe @BrownMarubozu can comment as he is a director of a public company. But my MBA understanding is directors need to balance shareholders and creditor expectations at this stage. If a sale satisfies full repayment of debt and creates most shareholder value...

English

@chesir3cat @ThePoorBG @BrownMarubozu Then Beutel and Spivak are honoring their fiduciary duty by resigning. A portfolio sale is the means of preserving exit value for common equity.

English

@chesir3cat @ThePoorBG @BrownMarubozu I just can't fathom keeping this thing public. In a perfect world if they refinance the bank facility, reduce SG&A and normalize credit losses it may generate a few million in cash a year. How do you refinance the convertibles without debt/ equity swap.

English

@ThePoorBG @chesir3cat @BrownMarubozu The merchant and investment banker both resigning... maybe the Hitzigs are crazy and emotionally attached enough to try and pull off 'Accord 2.0.'

English

@PawlukZenon @chesir3cat @BrownMarubozu And now David Spivak has resigned from BOD. Sadly this looks like the smart guys jumping ship to distance themselves from what's to come.

English

@chesir3cat @ThePoorBG @BrownMarubozu I wonder if Beutels and Hitzigs had a falling out. The last year has been pretty disastrous for Accord and Hitzigs were the architect behind the failed US expansion and ultimately the operators who drove this to the brink of default.

More will be revealed.

English

@PawlukZenon @ThePoorBG @BrownMarubozu What even is a lowball offer at this point given their options?

English

@chesir3cat @ThePoorBG @BrownMarubozu Beutel (co-founder who represents Oakwest/ 22% of shares) resigned as chairman of BOD. A take-private bid from Oakwest is imminent.

The issue is what leverage do the independent directors on a special committee have to argue against a low-ball offer?

English

English

Hmm…I don’t think this is as serious as you think and it certainly doesn’t mean that all interactions are like this either

Iv been using SpoiledChild products for months now and never been asked to submit a score for anything

I think they will diversify away from Meta after this disaster, I doubt they will allow themselves to be in this position again. They managed it for 8 years with zero issues. No reason to think they won’t find a way around this

English

$ODD

Something is happening with SpoiledChild

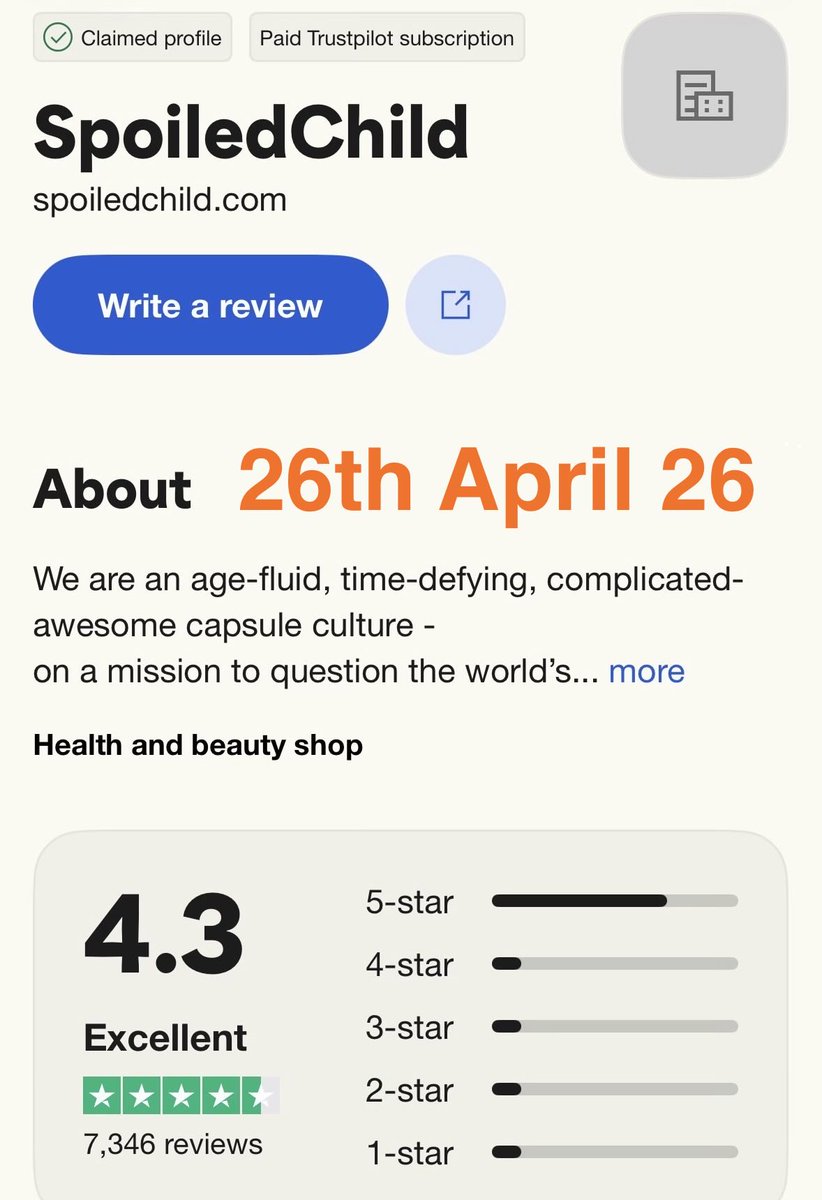

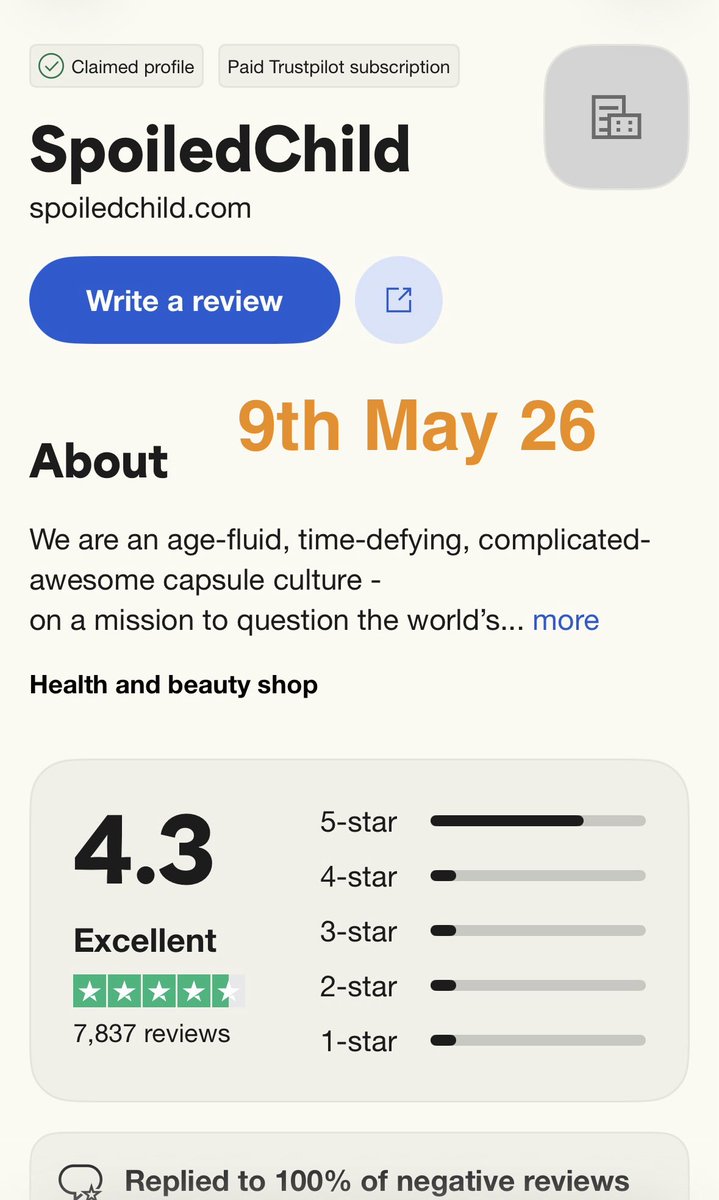

Iv been tracking TrustPilot review data since November last year when I started seriously looking at the company

Back then, they had a total of 3,668

In the space of just 6 months, that number has reached 7,837, with 500 reviews being added in the last 2 week period alone

For context, in January 2025 they only had around 150 reviews. It took them less than a year to bring in 3,500, a more than 20x from the start of the year

But in only 6 months since then, more than double that amount of reviews has been pulled in

This is a massive implied acceleration and seems to correlate with the explosion in data we have seen in internet traffic Q1 metrics

In the last 6 months they have grown faster than the previous 3 years combined in terms of review volume. Their avg. score has also ticked up from 4.2 to 4.3 in that time period

This is only a small snap shot of actual business. The sample size here is likely a small fraction of total sales volume. But one thing is for sure, growth looks to be exploding at SpoiledChild

The same is happening with METHODIQ at an even higher trajectory as per my recent post

In a year or two, I don’t think IL MAKIAGE growth is going to matter anymore. There is a good chance METHODIQ is disrupting and pulling business away from IL MAKIAGE.

Normally, this would concern me. But in this case, you are trading fickle, more unlikely to remain loyal makeup customers for potentially lifetime users as a result of health issues being resolved and effectively managed. Longer term, I think METHODIQ will become far stickier and higher margin than IL MAKIAGE. And that’s why I don’t care that the two brands are effectively competing with each other right now

Very excited to see what data we have on SC and METHODIQ at Q1 and potential guidance for Q2. I suspect SpoiledChild will outperform this year by a wide margin

I am not really concerned at all about the slowdown in IL MAKIAGE. At present, it is a funding vehicle for SC and METHODIQ. Once the two newer brands have scaled, it’s their future I am excited about, not IM. I would not invest in this company if IM was their only brand

Based off of their recent hires, I suspect brand 4 is going to turn some heads when it’s finally announced and launched. I don’t know what it will be, but I suspect it will be a further move into the medical/science field, moving the company even further away from makeup as its primary identity

I am happy for a delay in brand 4 if that happens. It makes sense now to scale SC and methodiq. They don’t need a 4th brand right now. But that is their decision. I am fine with either route.

The plaintiff deadline is on Monday. Following that we may see a retort from the company and a move to dismiss. We should also get a PR for earnings either next week or the week after

Not financial advice

Not financial advice

English

@weary_centurion @tang_syd Girlfriend likes the concealer, doesn't like their foundation.

So she will be throwing them some recurring revenue going forward 😀

Hope it works out for you longs.

English

@weary_centurion @tang_syd I hope I'm wrong. I took a position at 11.70 after last earnings and sold it yesterday.

It's after having my girlfriend order products to kick the tires on the business model my spidey senses question if this is a survivable business strategy.

English