Sameer

1.2K posts

Sameer

@Sameer9398

AI, Engineering, $SIVE $IREN $TSLA 🚀, Cats ♥️ NFA

Hyderabad, India Katılım Ağustos 2020

687 Takip Edilen258 Takipçiler

Charlie Munger was right, the first 100k is a bitch.

But today… I finally achieved it!!

Thank you $RKLB, $NBIS, $ASTS and $OUST.

English

@IkaKnight_ @aleabitoreddit Shilled in $5k in $LPK, Let’s see where it takes us.

English

@aleabitoreddit Bought some $LPK today. Looks like another wave up

English

Sameer retweetledi

When I see comments like this (and there are a lot) from retail investors:

I immediately think they lack the technical depth.

I'll walk through each one from $SIVE to $LPK:

1. Photonics TAM goes from $14B -> $154B In just two years time, and it's likely going to keep scaling past 2030 as it's the next generation architecture of choice.

It's not going away in 1 year. It's not going away in 3 years, which is why $LITE premiums keep going higher since they're backlogged into 2028.

$SIVE supplies CW lasers and is highly tethered to CPO and now pluggable transcivers for 1.6T and 3.2...

For expected companies like $JBL, Ayar, Lightmatter, Lightelligence, $POET, $MRVL Celestial, and $AMD.

This isn't a "trade", it's the core chokepoint and IP holder for the next generation of photonics.

And it's a comfortable hold for the next few years as they scale to become the next $LITE.

The risk I personally see (since they're already qualified with so many players), it's mainly how much TAM they can capture of the overall optical supercycle. (And potential risks with Win Semi volume ramp, but Win is massive so I can sleep tightly there).

As just supplying lasers isn't enough to justify valuation.

It's TAM expansion downward into making the entire ELS or entire pluggable transceiver that makes these laser companies so valuable.

Then afterward, they can vertically integrating upward for gross margin expansion upward like $COHR into doing the laser fabs or even substrate level.

And that in my view is a very asymmetric risk/reward ratio as we've already seen this done with $LITE as they went from $2B to $80B.

2. $LPK - Is the purest exposure, without the messy financials of SKC Absolics, as the next advanced packaging shift for glass substrates.

Almost every single major semi company from $INTC to Samsung are adopting glass substrates.

$LPK is basically $ASML of this chokepoint, since they supply to ~80% of the global players currently.

Yes, there's "trade cycles" for equipment suppliers like $ASML, where if there's more foundry capex, ASML scales up. But if there's downturns, these tend to perform poorly, and don't capture all the volume ramp that happens after.

However, if the MC is $650m and they're making $100-200M, revenue per costumer volume ramped, the amount they make from the glass substrate cycle will likely exceed current valuations.

And they'll have baseline fundamentals (as more companies adopt the packaging shift), that keeps their valuation up.

It's just a waiting game for volume ramp at this point.

3. $AAOI - This is literally $INTC but for America + Photonics. It's like saying Intel is not a long term investment.

Guess where all your optical transcivers are made?

China. Thailand. Malaysia. If you look at Innolight, Eoptolink, $FN, and others.

AOI is building the largest Made in America supply chains for both CW laser fab, as well as 800g, 1.6T assembly.

Yes, there are pluggable cycle ups and downs to this as well. There's going to be a wave for 1.6T next year, then CPO cannibalizes pluggables down the road.

But since they make the entire supply chain in house, they have extreme optionality for other segments. And like $NVDA older gen-GPUs, there's going to be sovereign DC requirements for older gen pluggables from names like $AAOI.

It's likely going to keep rising as it hits that $400m+/month revenue target H2 2026.

There's just a lot of different short term volatility along the way like the $600m dilution.

4. $IQE - ??? It's one of the most important players in the Western word for epiwafers.

$MTSI went out of their way to pay off IQE's debt because they can't have them going under. $IQE is also supplying to $LITE.

The world is currently bottlenecked both on the epiwafer level from Landmark comments and InP substrate levels.

Their financials were track but the raw book value, and value they hold to the entire Western supply chain... completely justifies their valuation. And other optical companies will not let their core upstream supply chain go under.

As these tens of millions worth of materials would screw up tens of billions worth of downstream products.

Again photonics is the next generation architecture required to scale AI. It's not Quantum where it's just "In development".

It's literally here and the architecture of choice by $NVDA.

I would not be surprised if all of these are a lot higher in 3-4 years time.

People who think it's one and done in 3 months time "only because I mentioned it" don't know what they're talking about.

Institutions would have bought up the name eventually (like Point 72 on $IQE) and retail would only find out after their valuations are 600% higher.

Should really do the research before adding comments like these:

These are all forward growth companies that require in-depth supply chain knowledge.

Sancet@Million_Sancet

This is my current portfolio As I said, I wouldn't sell any positions And I’ve kept my word, the money for the new position in $PENG does not come from my existing investments At the moment, I don’t see better opportunities in the market than what is already in my portfolio At least not at these prices I have on my radar things like $KOPN $DGXX $SOI etc

English

$LPK / $LPKF

You're not bullish enough.

This is easily going to $180 within a year.

English

@Agrippa_Inv @danroberts0101 We’re always excited for new Agrippa drop 🔥

English

My take on @danroberts0101 new post

$IREN Co-CEO just dropped a beautifully written thread on the company's compounding competitive advantages.

Seriously, a must read for every $IREN investor or folks who are on the fence.

My highlights:

- Dan confirmed that the 60 MW cloud contract with $NVDA is in fact measured in 'gross' MW, not IT. That was already obvious to me based on the earnings call material, however, it's great to get definitive confirmation.

The implications of this is ENORMOUS. The $NVDA contract has incredible economics, something I've analyzed extensively in my upcoming $IREN deep dive (released in a couple of days on Substack).

- Dan firing shots at the likes of $NBIS & $CRWV:

"And the asset-light neocloud trying to compete by renting capacity is discovering that sites were locked up years ago, and the operators utilizing them aren’t subletting. By the time new entrants solve for land, power and permitting, IREN will have gigawatts online, execution track record, and customer relationships that took years to build. That gap doesn’t close. It compounds."

This is by far my favorite quote coming out of Dan. Eventually, everyone will realize that the real advantage $IREN has over the rest of the neo-cloud sector, is the fact that they are the only provider that's 100% vertically integrated.

They don't have to deal with any land-lords. They don't have to pay billions to $BE to secure fuel cells in a desperate attempt to salvage a project that is tied to a large customer contract. $IREN is in control of its own destiny, and eventually that will show up in the bottom line (profits).

The “asset-light” model never works in an infrastructure-heavy industry. It works for hardware, when you are the high-margin designer and outsource the manufacturing process to a specialized entity. But it doesn’t work when the infrastructure itself is the product.

In cloud, the value is not just in having access to GPUs. The value is in controlling the full stack, which mostly consists of physical infrastructure.

If you outsource all of that to colocation partners, you are not building an AI factory. You are renting someone else’s factory, layering a spread on top, and hoping the economics still work after the landlord, the power provider, the OEM, and the lender have all taken their share.

That model can look attractive in the early innings because it allows rapid capacity announcements without heavy upfront CapEx. But structurally, it leaves the operator with the worst part of the value chain.

I'm really looking forward to comparing the net income lines between $IREN, $CRWV, and $NBIS a few years from now. I wouldn't be surprised if two out of the three remain unprofitable by then.

- I really enjoyed Dan's section about becoming a global cloud provider.

He did a great job in explaining the importance of being locally present in the markets you want to source customers from. Not just due to local proximity for inference, but also due to compliance & sovereignty.

These were my highlights, I'll let you discover the other gems yourself. This is easily Dan's best post and I think it does a lot in terms of IR, especially as it's coming from him; the co-founder and co-CEO of $IREN.

As mentioned earlier, very soon I'll be releasing a new deep dive on $IREN. It goes deep into the implications of the $NVDA partnership and Mirantis acquisition, including a bunch of different topics worth exploring. So far, the report is 30 pages long (including graphs / images) and I'm in the process of finalizing it.

Honestly, one of my best deep dives to date. I know I'm saying that for each release, but the depth and quality of our work is undoubtedly increasing. Can't wait to publish it.

Cheers guys! ✌️

Daniel Roberts@danroberts0101

𝐓𝐡𝐫𝐞𝐞 𝐋𝐚𝐲𝐞𝐫𝐬. 𝐎𝐧𝐞 𝐂𝐨𝐦𝐩𝐨𝐮𝐧𝐝𝐢𝐧𝐠 𝐀𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞. 𝐓𝐡𝐞 𝐈𝐑𝐄𝐍 𝐓𝐡𝐞𝐬𝐢𝐬. There's been a lot happening at IREN recently. Expansion across North America, Europe and Asia-Pacific. The NVIDIA partnership. The Mirantis acquisition. New GPU deployments. New customer discussions. A growing global footprint. Underneath all of it is a fairly simple view of where the world is heading, and a deliberate strategy for how we position IREN within it. That strategy is built on three layers. Together, they compound into a structural advantage that gets harder to replicate every quarter we execute. Layer 1: Physical infrastructure. Power, land, substations, data centers, cooling. The foundation that everything else sits on. Layer 2: Compute infrastructure. The GPUs, servers and networking that go inside those buildings. Deployed at scale. Generating revenue. Building execution track record. Layer 3: Software and operational capability. The orchestration, deployment tooling and enterprise expertise that makes the first two layers work harder for customers, and opens the door to a broader, higher-value market over time. Layers 1 and 2 are where the overwhelming majority of IREN's value is being created today. Layer 3 is where that advantage compounds further over time, but only because Layers 1 and 2 are built, owned and controlled at scale by IREN, not subscale nor contracted from a third party. Think of Amazon. They didn't win e-commerce by building a great website. They won it by controlling the fulfilment infrastructure at a scale nobody else could replicate. The foundation you don't control becomes the ceiling on your business. That is exactly how we think about IREN. The physical infrastructure - the land, the power, the substations, the data centers - is owned and controlled by us. The compute deployed into it generates the revenue and execution track record. And the software, orchestration and enterprise capability we are more methodically building on top is what turns the total product into a vertically integrated AI Cloud platform that compounds over time and deepens into a competitive moat. AI is still early. The bottleneck is increasingly physical. And we have spent eight years building the foundations.

English

@Ayouubb_ @aleabitoreddit Check if your broker supports it and enable share lending if possible

English

A guide by Serenity on becoming a true Swedish local:

1. See crown jewel photonics company in $SIVE?

2. Get angry about 2024 revenue numbers, ignoring forward growth.

3. Encourage everyone to transfer control to America at the bottom, before the CPO supercycle

4. Be angry that the stock keeps rising

5. Have local hedge funds short 17%+ of free float on way up

6. Their funds loses 20%+ of value, and faces infinite losses

7. Face sudden realization America now dominates ownership with MSCI inclusion / NASDAQ listing coming up.

8. But see new news Jabil mass producing 1.6T LRO for hyperscalers with $SIVE H1 2027?

9. Don’t change your mind: keep focusing on 2024 revenue numbers and local accounting offices while executives are in America.

10. Become a meme on X.

Serenity@aleabitoreddit

English

Sameer retweetledi

@user637826 @Haenco1 We have $SIVEF on webull, but with a $50 fee to buy it everytime.

English

@Haenco1 Only in IKBR and Fidelity AFAIK. There’s lots of retail waiting to buy in WeBull, Robinhood etc and big US Institutions.

English

$SIVE short squeeze thesis.

Short interest: ~17% → $255M in short positions

• Modest squeeze: 75 SEK (+50%) → shorts lose ~$130M

• Strong: 150 SEK (+200%) → shorts lose ~$510M

• Full squeeze: 300 SEK (+500%) → shorts lose ~$1.3B

→ MSCI inclusion = index funds MUST buy automatically

→ Nasdaq NY listing = millions of US buyers suddenly have access

→ CHIPS Act backstop = institutional legitimacy

→ Q1 earnings May 29 = first US-standard audit report

Catalysts converging + forced institutional buying + short covering = rare asymmetric setup.

English

Just putting it out there:

$SIVE short interest is probably higher than 17%+ now.

As lot of local Swedish hedge funds are very underwater, shorting Sivers.

They're about to meet US institutions through:

> MSCI inflow in 2 weeks.

> NASDAQ Listing.

> US CHIPS Act backstop.

alongside core revenue driver from the optical supercycle revenue ramp from likely $AAPL, $JBL, $POET, Ayar, Onet/Enablence, Lightium, $AEVA, $MRVL, Lightmatter, Lightelligence, and $AMD over the next year or two.

I personally don't think it's going to end well for the Swedish locals shorting (and some random algos) at this early stage.

And the popular saying is every one stock short turns into a long eventually.

Serenity@aleabitoreddit

$SIVE short interest is around ~17% of free float apparently from some third party data, which is enormous (probably higher after yesterday). IMO they're prob fked doing it so early on. Now with MSCI + CHIPS ACT + NASDAQ Listing cataylsts. There was another local Swedish hedge fund that was down -20% off their shorts last month, so it might go under if things continue as is.

English

@Jornka329996 @aleabitoreddit Cut some exposure last month & rotated into $SIVE

Serenity@aleabitoreddit

A good looking guy that would mog Clavicular side by side has no impact to any fundamentals. I cut some exposure too in $LITE $COHR like Leopold, last month. But rotated it to a specific optical theme with CPO names like $SIVE / Foci. The entire photonics supply chain is in the start of a massive supercycle and there’s nothing more compelling going long on CPO as an architectural paradigm shift. Markets conflate two companies as the entire theme and sell off anything with it. Great buying opportunity for people who understands the nuance though. I still think there’s upside for Lumentum and $COHR, just less likely to double at current prices as fast if you’re going shares only.

English

@Sameer9398 @aleabitoreddit Can you tag me where he indicated this?

English

@Jornka329996 @aleabitoreddit He’s already indicated that he’s been increasing his position. Just look at his previous tweets.

English

@aleabitoreddit @aleabitoreddit stupid question why dont you just double down and increase your position so Shorts burn?

English

@aleabitoreddit Anyone figured out how much flow the MSCI inclusion will trigger?

English

I'm 100% sure if I met all you "photonic memory" experts in real life.

498 out of 500 of you couldn't explain CXL memory pooling or KV cache infrastructure and what $PENG actually does to derive revenue off that.

This is why I'm seeing all these random $RKLB, $HIMS, or non technical AI experts on my timeline now.

Backseat commenting completely wrong things about M7U MOCVD capex and $TSEM that aren't related.

Or conflating every single term like an $SMCI integrator with photonics IP.

Then just pitching buzzwords every under every one of my posts.

#silentlystacking@TheMindofMatt

@aleabitoreddit I bought some PENG for: * KV-cache infrastructure, * memory expansion, * inference bottlenecks, * CXL memory pooling, * or external memory appliances,

English

@Fadi_Finance @Sofigoodboy @DanilSer33 Article is bullish for $SIVEF, Expects a 70% upside if well executed by the company.

English

@Sofigoodboy @DanilSer33 Don’t have a seeking alpha account. What’s the TLDR?

English

@aleabitoreddit $AXTI returns are insane

I have picked $SIVE for now and will find out in 6 months to a year

Am I doing the right thing?

English

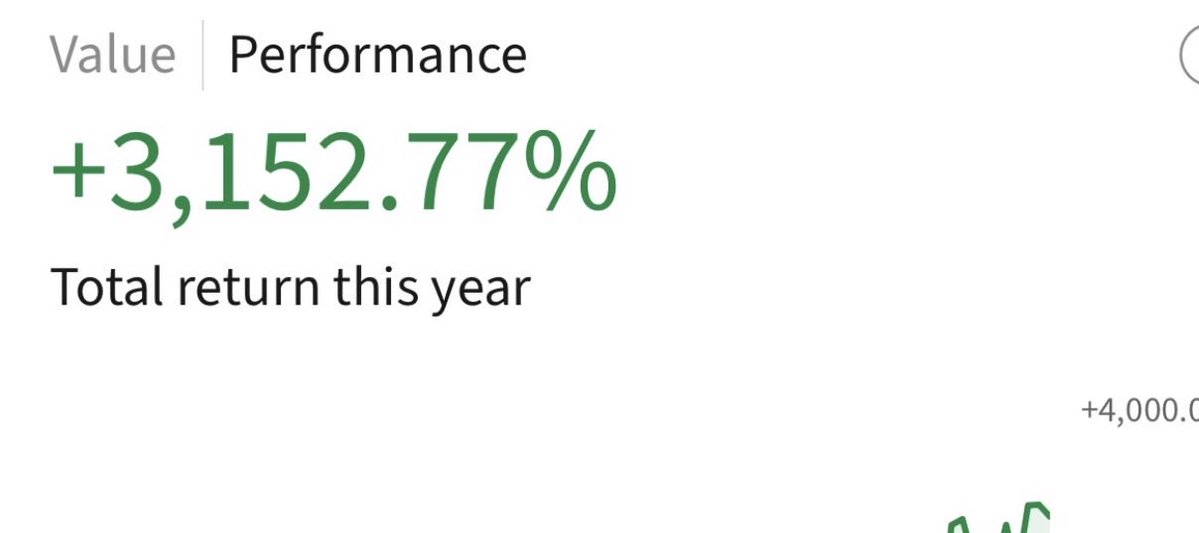

Leopold Aschenbrenner is a legend, but I'm not quite sure he can beat 3152.77% YTD in the Serenity Awareness fund.

That being said, I've hit 23 different longs this year with 100-1000%+ YTD.

1. $AXTI

2. $AAOI

3. $SIVE

4. $LITE

5. $IQE

6. $AEHR

7. $CRCL

8. $EWY

9. Unimicron

10. Nitto Boseki

11. $OSS

12. $GDRZF

13. $RPI

14. $SOI

15. $ALRIB

16. $SNDK

17. $SIMO

18. $VPG

19. $TSEM

20. $ARM

21. $MRVL

22. $INTC

23. $LPK

Do you remember all of these anon?

Sam@Quantrarian52

Wait wait wait….. could Leopold be the infamous @aleabitoreddit ?

English

Portfolio update: $5.4M

Officially 50% of my original $10M goal.

I set that goal back in 2017, not long after I started investing, and seeing it now within reach feels surreal.

A thing I have to talk about is option selling, mainly CCs, while they generated nice returns during a draw down, they have capped my upside massively during the recent run, I believe that without them I could be at around 6.5M today.

The lesson learned is to utilize them on lower portions of my positions.

I’m not stopping here though. The goals will keep getting bigger, and I’ll keep sharing my journey, research, and ideas publicly for free like I always have.

That said, I’m also launching a subscription service for those who want beyond what I already do:

• Live buys & sells

• Ideas shared earlier

• Direct access to DM and discuss anything.

Some of my friends here got backlash over launching a subscription service, be gentle with me, it's definitely optional, non-subs get the same as always. 🫡

I genuinely appreciate everyone who’s followed along, engaged with the posts, challenged my ideas, and made this journey a lot more enjoyable.

Hopefully we continue winning together for many more years.

English