Sabitlenmiş Tweet

Sebastian Furn

2.5K posts

@SebastianFurn

Obsessed with the BTC treasury space. 185 companies tracked across 33 countries. | @Halvex1

Strategy has acquired 1,550 BTC for $101 million to increase our $BTC Reserve to ₿845,256. We have also increased our USD Reserve by $100 million to $1.0 billion. $MSTR $STRC strategy.com/press/strategy…

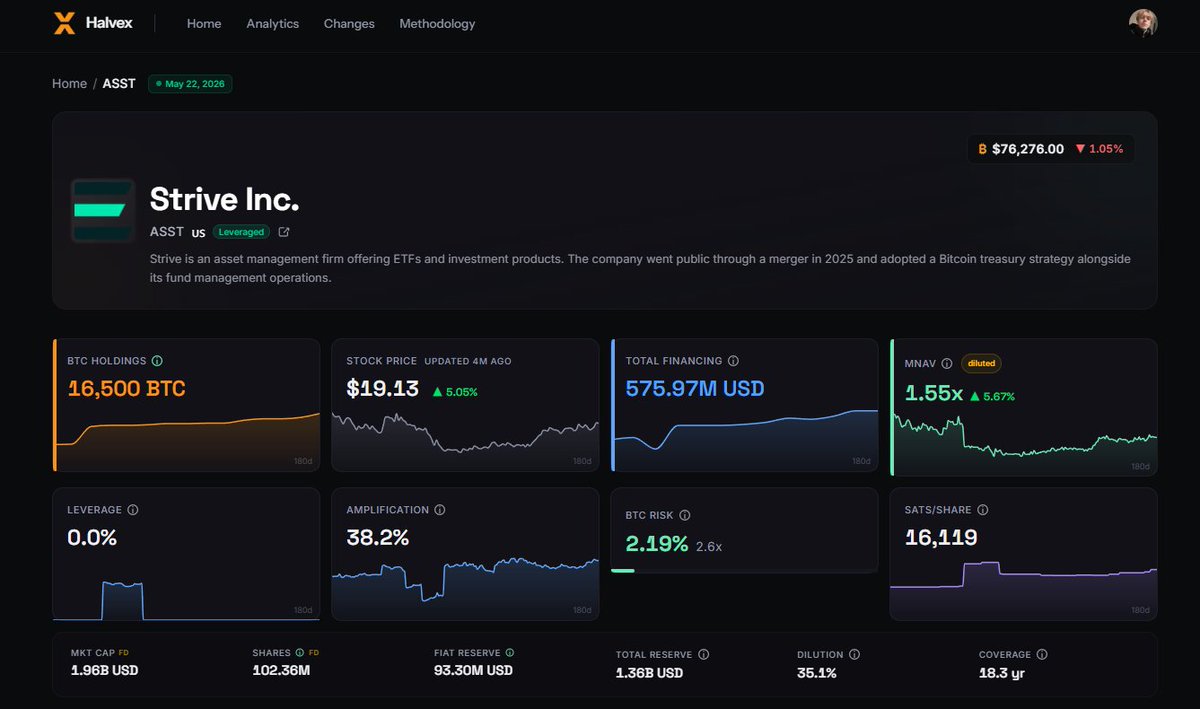

$ASST bought 2,500 BTC. Holdings: 19,000 BTC.

$MSTR sold 32 BTC. Holdings: 843,706 BTC.

I agree. We spend a tremendous amount of time thinking about downside risk, stress testing scenarios, and building protections accordingly. In our view, $ASST is not over-amplified. If anything, we believe it remains under-amplified relative to the opportunity set Bitcoin presents. It’s important to understand that risk management is a constraint, not the objective. The goal for Strive’s common equity, $ASST, is to outperform Bitcoin and maximize long-term shareholder returns. Importantly, we are not trying to optimize away every last basis point of risk. There is a meaningful difference between reducing the probability of failure from 10% to 1% and reducing it from 0.02% to 0.01%. The latter may technically cut risk in half, but from an expected value perspective it is immaterial if the tradeoff is materially lower upside. This philosophy informs every major capital allocation decision we make. We start by protecting against outcomes that could permanently impair shareholder value. Once that threshold has been met, our focus shifts to maximizing expected value. In our view, risk is not measured solely by the probability of loss. It is also measured by the opportunity cost of failing to fully participate in a highly asymmetric outcome. That is why we intentionally have no debt, maintain substantial dividend reserves, and run amplification aggressively. We seek to eliminate risks that could permanently impair shareholder value so that we can maximize amplified participation in Bitcoin’s upside. We believe Bitcoin’s return distribution will continue to be highly asymmetric to the upside. If there is a meaningful probability that Bitcoin compounds dramatically over the coming decades, the optimal capital structure is not the one that sacrifices substantial upside to marginally improve an already remote downside outcome. It is the one that preserves resilience while maximizing participation in that upside. This is also why we are focused on acquiring as much Bitcoin as we can while it remains below $100,000. We believe Bitcoin is likely to be substantially higher over time and that periods where Bitcoin trades near its 200-week moving average are precisely when amplification should be run as aggressively as prudently possible. We think in probabilities, expected values, and equity compounding. If you optimize around fixed income math, you should expect fixed income returns. We built the company we personally wanted to own: an engine designed to maximize Bitcoin per share growth, outperform Bitcoin, and maximize shareholder value across a wide range of bullish Bitcoin outcomes.

$ASST can pay $SATA dividends for 9 years even if Bitcoin depreciates 10%/year. So, no. $ASST is not overleveraged.

Much of the $STRC and $SATA market appears to be dividend capture traders. As div frequency goes up, the trade becomes less lucrative. That demand disappears. Rates will go up.

$SQNS sold 456 BTC. Holdings: 658 BTC.

$BTM Nasdaq to suspend trading May 26 and file Form 25-NSE.