Sree

108 posts

@ParrotStock Parrot, isnt $CRWD overstretched? Any consideration for trimming?

English

If you had invested $10,000 in $AMD on the day they went public, you would have $7.5 million today.

If you had invested $10,000 in $SoFi on the day they went public, you would have $6,800 today.

me who chose to invest in SoFi:

English

@StockMarketNerd Seems your statistics are solid. Very less likely here you are wrong.

English

@Ticker_Analytic Maybe I’m wrong! 🙂

Has happened before will happen again. 🤷♂️

English

$CBRS:

1) 76% 2025 revenue growth.

2) 15x the 2026 + 2027 revenue they expect to recognize from backlog.

3) About 290x trailing GAAP EPS.

4) 200X+ 2025 revenue.

$NVDA:

1) 66% 2025 revenue growth (much larger base).

2) 6x 2026 + 2027 revenue. 51% 2026-2027 expected revenue CAGR.

3) About 45x trailing GAAP EPS. PEG well below 1x.

4) 25x trailing revenue.

Not perfect comps. But newly public so limited estimate data to work with. And if I'm picking between one or the other.. the choice feels pretty easy.

Go with the king. Not the wildly expensive new kid on the public block, in my always could be wrong opinion.

Are you buying this IPO?

English

Will $SOFI still be a +$50 stock by the EOY regardless of the dips?

English

I turned $20,000 into $2,000 in just 3 years from $SoFi

Ask me anything.

English

What’s the worst performing stock you hold in your stock portfolio right now? 👀

English

@EmmaStockNotes @HolySmokas Yeah. I would take $NU over $SOFI any time

English

@HolySmokas Jeremy’s two hypergrowth picks are $SOFI and $CELH.

I like $SOFI, but if I had to pick one fintech compounder, I’d lean $NU.

The business already looks more mature fundamentally.

English

2 HYPER GROWTH STOCKS I just bought‼️

"This will be my next AMD"

$QQQ $SPY $AMD $NVDA $CRM $NOW $SOFI $$CELH

English

$SE +16% OMG 🟢 🤯

Total Revenue: $7.1B, +46.6% vs $6.45B estimate.

Net Income: $438.2M, +6.7%.

Adjusted EBITDA: Reached $1.0B for the first time in a single quarter, +9.3%.

EPS: $0.68, missing the analyst consensus of $0.75.

EPS miss doesn't really matter with such strong top-line growth.

English

2/ Mark Grether - GM of $PYPL Ads

Previous role: Built Uber's ad platform from $0 to $1 BILLION in revenue in just 2 years.

Now he has access to 26 billion transactions per year and data on past AND future shopping habits.

The advertising opportunity here is staggering.

English

🧵1/ The most underrated story in fintech right now:

PayPal's complete leadership transformation.

CEO Alex Chriss replaced the ENTIRE previous leadership team.

And he brought absolute killers with him. Here's who:

English

@Mr_Derivatives Semis taking portfolio up and software is taking it down. Net net not in extreme greedy.

English

“Dad, $AMD is $400.00 now. Weren’t you able to buy it for $80.00?”

“Son, I was too busy buying $SoFi at $15.00 and it’s still at $15.00”

English

@SwissKnifeInv Yeah. Wish new mgmt shows that sense of urgency and executes flawlessly. Time will tell.

English

@Ticker_Analytic Then it would be yielding 7% free cash flow. This is definitely the best case. Free cash flow collapses faster than mgmt can turn the ship around and buyback shares. Time will tell. $PYPL

English

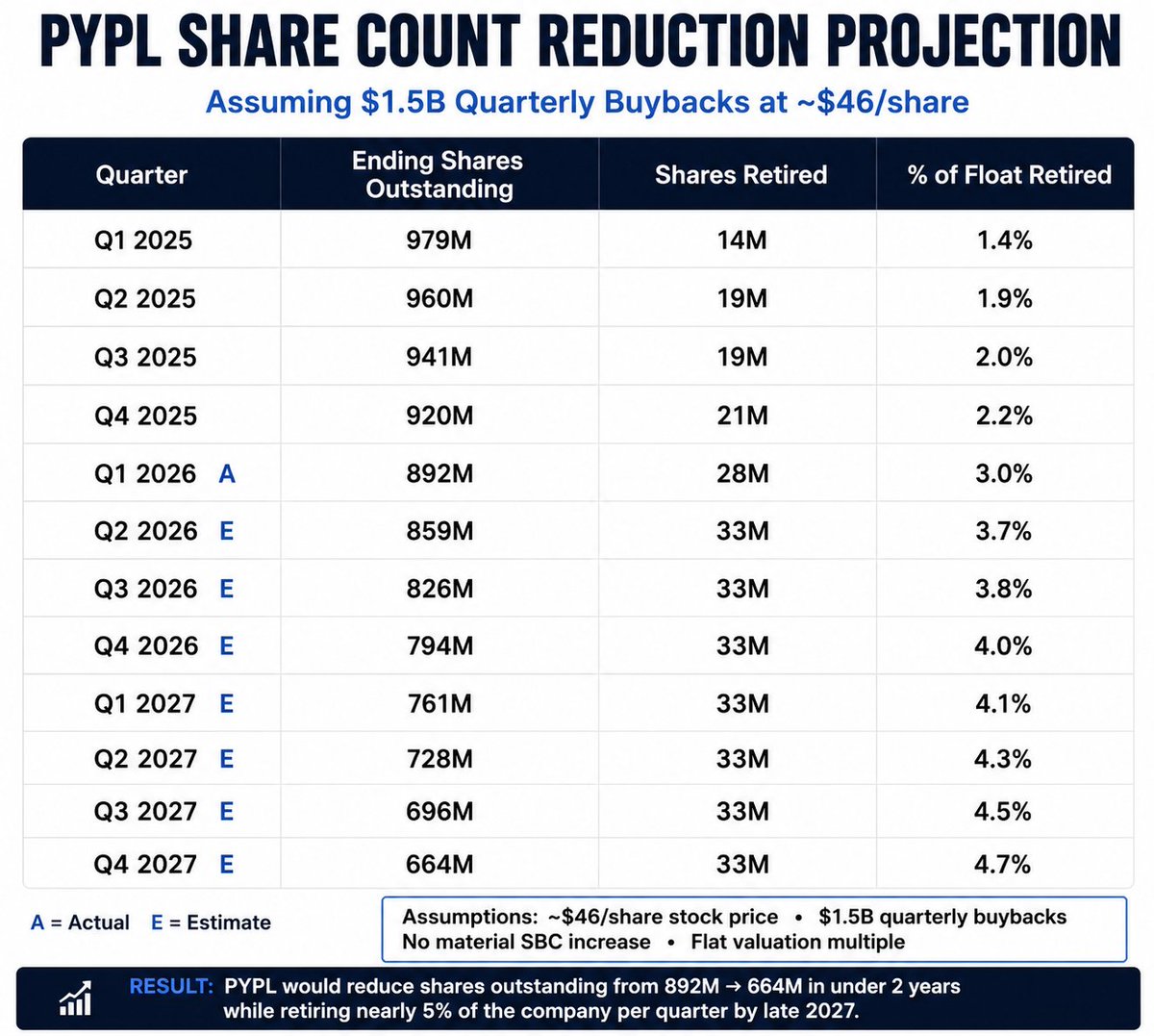

$PYPL is retiring 3% of shares per quarter. By 2028, that hits 5%. Total shareholder yield clears 20%.

English

Just got off the phone with a millionaire tech bro who is all in on $MU and $AMD, he said that we are just getting started and we haven’t seen anything yet.

BULLISH.

English