Sabitlenmiş Tweet

Joey

4.4K posts

Joey

@jojocal19

Girl Dad, Cybersecurity Mgr, Cars, Real Estate, Sports, Traveling, Options and Futures. College Football, Gator Alum c/o 2013 #GoGators 🐊

Florida, USA Katılım Mart 2009

2.3K Takip Edilen370 Takipçiler

Become a Claude Certified Architect

Here are all the required resource in one place: (save it)

Training courses: anthropic.skilljar.com (13 free courses)

Cookbook: github.com/anthropics/ant…

Exam Guide: share.google/0eqIbebzRMUt8K…

Practice questions: claudecertifications.com (free)

MCP documentation: modelcontextprotocol.io (free)

API documentation: docs.anthropic.com (free)

Partner Network: anthropic.com/partners (free to join)

Link to join: anthropic.skilljar.com/claude-certifi…

Personal Playbook someone created after the exam: drive.google.com/file/d/1luC0rn…

English

Took first trim today on my $ARM position

I want to breakdown the setup to help you find your next big winner:

1. Trend Structure

The biggest thing I notice:

Clean staircase price action

You can literally see:

-Expansion

-Tight flag / consolidation

-Expansion again

That’s institutional accumulation behavior.

2. Volume Analysis

This is probably the strongest part of the chart.

Notice:

-Breakout candles have expanding volume

-Pullbacks have lighter volume

-Recent breakout candle exploded with volume

That’s exactly what we want.

3. The Tight Consolidation Before Breakout

The stock:

-Stopped pulling back deeply

-Started tightening

-Held above the 21 EMA

-Built pressure underneath resistance

This creates a coil like a spring...

Think the more compression --> the bigger the move.

Another thing that stood out on the $ARM chart was the weekly timeframe...

$ARM broke out of a massive weekly base.. then started consolidating right above that base

It waited for the weekly moving averages to catchup (8EMA) the ripped right off that spot

A lot of stocks get stretched from the weekly moving averages too quick and then a continuation move is pretty much unlikely..

1 monster trade like this can make your whole year

+$250k between shares and options!

English

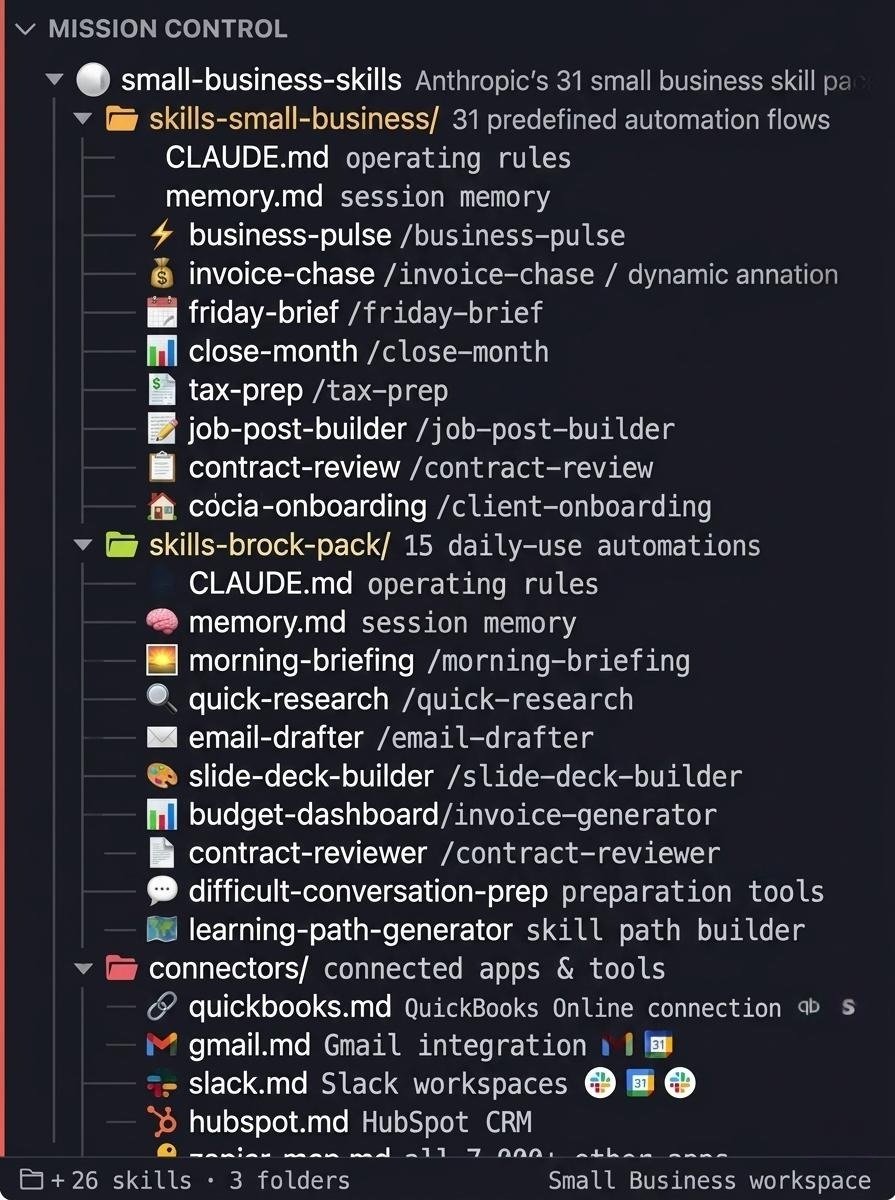

Claude For Small Business is INSANE.

I've built a complete breakdown of all 31 Anthropic Small Business skills that maps every workflow, connector, and automation in under 10 minutes.

The same skill stack that had 382,000 downloads on its first day.

Financial operations, sales and client work, HR and hiring, marketing and growth, reporting and dashboards.

Inside the breakdown:

- All 31 skills organised by function with the 5 to run first

- The 12 connector setup guide in priority order with permission settings for every sensitive action

- Worked examples for Business Pulse, Invoice Chase, and Job Post Builder with real output shown

Want a copy? Like + Comment "31" and I'll send it over ASAP

(Must be following)

English

@BryanJ361 Would you mind sharing your cost to build (inc land)? I saw on Lamont's post you do these for $100/sq ft build cost. I am interested in doing some affordable housing builds. I think it's a huge need nowadays.

English

we've spent the last few months building a new free playbook with @MrZincx.

it's his full IB 50 strategy on $ES and $NQ.

3 levels. one entry. every rule he uses, backed by edgeful data.

like + reply "IB 50" and we'll send it to you (must be following so we can DM).

English

10 piracy repos you should NEVER use

SAVE IT

This is NOT a recommendation list. This is a do-not-touch list.

1. Awesome Piracy

A giant index of piracy tools, sites, and “free” content. One click and you’re deep in DMCA territory, not productivity heaven.

Repo → github.com/Igglybuff/awes…

2. Seedbox‑Lite

A Netflix‑style UI on top of torrents. Streams straight from your seedbox. Also a perfect way to put your IP in every rightsholder’s crosshairs.

Repo → github.com/webtor-io/self…

3. Webtor Self‑Hosted

Pick a torrent, stream it instantly in the browser. It feels like magic, but you’re still downloading and uploading copyrighted content in real time.

Repo → github.com/webtor-io/self…

4. RapidBay

Self‑hosted torrent streaming with Chromecast and TV support. Clean UI, ugly risk. It turns your box into a 24/7 movie piracy hub.

Repo → github.com/hauxir/rapidbay

5. Cloud‑Torrent

Remote torrent client with a web UI. Great dev work, terrible idea on a paid VPS tied to your real name and card.

Repo → github.com/jpillora/cloud…

6. Mov‑CLI (with shady plugins)

The core is neutral, but third‑party plugins scrape gray‑zone and outright illegal streaming sites. One bad plugin choice, and you’re over the line.

Repo → github.com/mov-cli/mov-cli

7. Popcorn‑Time‑style forks

“Netflix but with torrents” never died, it just keeps forking. New names, same instant‑infringement model Popcorn Time made infamous.

Repo → github.com/popcorntime/po…

8. Anime streaming scrapers

Anime “APIs” and scrapers targeting free streaming sites get mass‑deleted after takedowns. If your stack relies on them, you’re building on legal quicksand.

Example → search “anime streaming scraper GitHub” / “aniwatch API GitHub”

9. Piracy “megathread” mirrors

Curated lists of warez, streaming, and cracking tools. Reading them isn’t the problem; using half the links absolutely is.

Repo → github.com/SeppPenner/awe…

10. “Netflix‑killer” stacks

Anything that advertises “self‑hosted Netflix that scrapes the whole web” is basically a UI wrapper on torrents and illegal streams. Slick, but not safe.

Repo → github.com/hauxir/rapidbay

Repo → github.com/webtor-io/self…

English

F*ck paying $149/month for credit repair.

AI does the entire thing in 5 minutes

Disputes. Letters. Legal codes. Bureau addresses. Settlement scripts.

For free.

Credit repair companies have been billing Americans $4 billion a year to copy-paste templates a robot does for free now....

Like + RT + comment "credit" and i'll send it to you (must be following)

English

🚨🧵Why America Can’t Stop Trump

Donald Trump is broadly unpopular.

That much is true.

His approval ratings are underwater. Independents are fleeing Republicans like they have herpes. The economy is dragging him down. Inflation from his dumbass tariffs are dragging him down. Gas price spikes from the Iran War is dragging him down. His billion dollar ballroom is weighing him down.

English

You can buy a house in America using only credit cards

No mortgage. No down payment. No income verification. No appraisal

The title closes in 7 days because you show up as a cash buyer

90% of americans think this is illegal. It's not. It's not even unusual

Real estate is the only major asset class in America where you can use unsecured credit to acquire it and the seller will never know how you paid

The bank that issued your Chase Ink card has no idea you used the credit line to wire $80K to a title company in Ohio. The title company has no idea you didn't have $80K in your checking account 5 days ago. The seller sees a cashier's check at closing and that's the end of the conversation

Here's the actual play:

Step 1: find an off-market or distressed property in a tier-2 or tier-3 market. Single-family in working-class neighborhoods of Cleveland, Detroit, Memphis, Birmingham, Toledo, Akron, Dayton, Buffalo. Average single-family with renovation needs: $35K-$90K

Step 2: stack 0% business credit. Chase Ink Cash + Chase Ink Unlimited + Amex Blue Business Plus + Capital One Spark = $80K-$150K in 0% credit at a 720+ FICO

Step 3: liquidate the credit lines through Trykashu (6.5% fee, 72-hour funding). On $80K of card capacity, Trykashu wires $74,800 cash to your business checking. Fee: $5,200

Step 4: close on the property as a cash buyer. Cash close gets you 5-15% discount over a financed buyer because the seller doesn't risk a financing contingency falling through. 7-day close instead of 45-60 day mortgage close. No appraisal contingency. No inspection contingency required (you can still do one)

Step 5: renovate to rent-ready. Most $50K-$80K single-family purchases need $5K-$15K in cosmetic work. Use the remaining 0% credit for materials and contractor payments

Step 6: rent the property. Single-family in working-class Cleveland rents for $850-$1,250/mo. Mortgage payment on a $0 mortgage is $0. Net cash flow before tax: $750-$1,150/mo

Step 7: refinance at month 8. Apply for a DSCR loan. DSCR loans don't check your income, don't check your W-2, don't pull your tax returns. They check one thing: does the rent cover the mortgage payment with a 1.0-1.2x coverage ratio. On a $1,000/mo rent, the lender will approve a 30-year mortgage at about $850/mo principal + interest, which on current rates means a loan amount of roughly $130K-$140K

Step 8: cash-out refinance pulls $75K-$95K of equity. Use the cash-out to pay off every 0% credit card you ran through Trykashu. Cards reset to $0. You own a free-and-clear cash-flowing rental property at a 30-year fixed rate with positive cash flow funded entirely by the original tenant

Total of your own money in the deal at end of cycle: $0

Total capital deployed: $80K bank credit (now paid off from refi cash-out)

Cost of the entire operation: $5,200 Trykashu fee + closing costs ($2K-$3K) + minor refi costs ($1.5K)

Final position: own a property generating $300-$500/mo net cash flow after the new mortgage, free credit cards reset to $0, refinanced into a 30-year fixed rate

Most real estate gurus charge $50K to teach you how to qualify for a conventional mortgage and put 20-25% down. The bank already has the money. You just don't have to play by the rules they sold you in the guru course

The standard mortgage path on the same $80K house:

20% down payment: $16,000 of YOUR cash

Closing costs: $4,000-$6,000

Total cash out of pocket: $20,000-$22,000

Mortgage at 7.2%: about $435/mo principal + interest on $64K

Time to close: 45-60 days

The 0% credit path on the same house:

Down payment: $0

Closing costs: $4,000-$6,000 (also financed through 0% credit)

Total cash out of pocket: $0

Cost of capital: $5,200 in Trykashu fees during the cash-buyer phase

Time to close: 7-10 days

Discount captured by being cash buyer: $5K-$10K off purchase price

Same property. Same tenant. Same monthly rent. The credit card path costs $22,000 less to acquire and closes 6 weeks faster

A woman I met at a networking event in Dallas runs this loop 4-6 times a year. She has 19 rental properties. Total of her own money invested across the entire portfolio: under $40,000. The first 6 properties were all funded through credit card stacks. Every refinance after that funded the next acquisition

She bought her 19th property last quarter. Same play. Same cards. Same Trykashu liquidation. Same DSCR refinance at month 8. Same $0 of her actual cash

Real estate gurus call this "creative financing." Banks call this "credit utilization." The IRS calls this "ordinary investment activity." None of them call it illegal because it isn't

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

English

This New York Times piece is worth your time. Here’s what is happening, as simply as I can put it.

Back in January, Trump sued the IRS, an agency he controls, demanding $10 billion over the leak of his tax returns a number of years ago.

IRS lawyers did their jobs. They wrote a memo laying out the defenses that could beat the suit, including the fact that Trump filed too late. His own lawyer was in court when the leaker pleaded guilty in October 2023, more than two years before Trump sued.

The Justice Department never showed up to court. Never argued back. Never used the defenses sitting on their desk.

The judge got suspicious and ordered both sides to explain whether they were actually opposing each other or just colluding. The day before that brief was due, Trump dropped the suit.

Same day, his Justice Department announced a $1.776 billion taxpayer-funded “anti-weaponization fund.”

Trump gets a formal apology. The IRS agrees to drop any audits of him and his family, even though a 2024 Times report found a loss in an ongoing audit could cost him over $100 million.

The acting Attorney General, Trump’s former criminal defense attorney, picks the five commissioners who decide who gets paid. Trump can fire any of them. Proud Boys and Oath Keepers are not ruled out.

This is the most corrupt thing I’ve ever seen from an American president.

Where in the hell are my Republican colleagues?

nytimes.com/2026/05/19/adm…

English

Day traders, listen to me:

1) Wait for a 4H FVG to form.

2) Wait for the price to hit the 4H FVG on the 15 Min.

3) Wait for a new FVG to form on the 15 Min.

4) Enter on that 15 Min FVG.

No indicators. No complexity. Just price, FVGs, and patience.

Full PDF in the pinned tweet.

English

The Volume profile is the only profitable indicator

But most traders using it still lose.

Here's how to use it the right way & turn it insanely profitable:🧵👇

English

An ex-Capital One underwriter just sent me 9 pages of internal scoring rules

Your credit score is only 32% of the approval decision

The other 68% is data the bank pulls from your phone, your email provider, your IP address, the device you applied from, and the time of day

You've never seen any of it and you can't dispute any of it

Here's what's actually scoring you that you can't see on your credit report:

Phone metadata score

Cap One pulls your mobile carrier data. Length of time on current carrier (longer = more stable). Whether you've changed phone numbers in the past 24 months (one change fine, three is a red flag). Whether your phone number was previously associated with a different identity (heavy negative)

If you got a new phone number 6 months ago, you're scoring lower than someone with identical FICO who's had the same number for 8 years. They never tell you this. There's no way to dispute it

Email address scoring

Free email providers score 3-7 points lower than custom domain emails for business card applications. Yahoo and AOL score lowest. Gmail is neutral. A custom @yourbusiness. com domain scores highest

Application device fingerprinting

The device you apply from is logged. Cap One tracks the device's previous applications, even from different account holders. If you're applying from a laptop that submitted 4 other Spark applications in the past 90 days, the model flags you for syndicate fraud and routes to manual review

Time of day

Applications between 11pm and 4am local time score 4-8 points lower than 9am-5pm applications. The model treats overnight applications as higher-risk because that pattern correlates historically with fraud rings. Most business owners apply at 1am because that's when they have time. They don't know they're being penalized for the timing alone

IP address history

If your IP has been used to submit credit applications for other people in the past 12 months, you're scored down. Significantly. This catches people who applied from a coworking space where someone else also applied last month, even if you've never met that person

Browser session length

A session under 90 seconds scores low (assumed bot or rushed fraud submission). A session over 22 minutes also scores low (assumed indecision or copy-pasting from elsewhere). Sweet spot: 4-9 minute application time

The actual scoring weights from the matrix:

FICO: 32% of decision

Annual revenue stated: 18%

Years in business stated: 11%

Existing relationship with Cap One: 14%

Device + IP + session data: 9%

Phone metadata: 7%

Email scoring: 4%

Time of day: 3%

Branch foot traffic (if walked in): up to 12% bonus

That 21% combined weight on data you don't see and can't dispute is enough to swing approval or denial on a borderline file

What this means for you:

Use a custom domain email when applying. yourname@yourbusiness. com beats gmail

Apply during business hours, not at 1am

Use a device that hasn't been used for other recent applications

Don't apply from a public IP (coworking, coffee shop, hotel wifi)

Take 4-9 minutes on the application. Don't rush. Don't linger

Have a verified business phone number that's separate from your personal cell

Same FICO. Same revenue. Same product. Following these adjustments routinely flips marginal denials to approvals because you're moving the 21% invisible score in your favor

The matrix only stays internal because nobody outside the underwriting team has read it. The ex-underwriter who sent me this no longer works there. Cap One can't sue him for sharing internal scoring rules that aren't trade-secret protected. The model has changed since he left but the basic categories haven't. Every issuer uses some version of this. Cap One was just the one that someone walked out the door with

The bank knows things about you that you don't know they know

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

English

There are 4 specific days a year American banks will approve almost anyone for credit

They'll approve people they denied 3 days earlier

They'll approve credit limits 60% higher than the normal algorithm allows

The 4 days: March 31, June 30, September 30, December 31

These are the last business days of each fiscal quarter. The day senior bankers, underwriters, and credit officers all have one objective: hit their quarterly origination targets

A Chase Ink Cash application submitted on March 15 gets evaluated against the standard underwriting model. Model approves you for $25K or denies you outright

The same application submitted March 31 gets routed through "exception" approval queues that bankers process manually because they've fallen short of their team's quarterly target. Marginal applications that would normally bounce get approved. Strong applications that would normally clear at $25K clear at $40K. Borderline files get one-time underwriting overrides

This isn't a conspiracy. It's a regulatory artifact

Every publicly traded bank reports quarterly earnings. Credit card origination volume is a KPI. Branch managers, regional VPs, and credit officers all have variable compensation tied to hitting quarterly numbers. If their team is at 89% of target on March 28, the entire department is in approve-everything mode for the next 72 hours

The end of Q4 is the biggest of the four because:

It's also year-end (annual bonus structures stack on quarterly targets)

Most banks run year-end credit card promotions to boost origination volume for shareholder reports

Federal lending quota compliance gets audited based on full-year numbers

Branch managers want to enter the new fiscal year with strong pipeline metrics

December 28-31 specifically produces routinely 20-30% higher approval rates than the average week. The data isn't published. You only see it if you've watched application volume across calendar years at scale

What this means tactically:

If your file is borderline (FICO 670-720, limited business credit history, recent inquiry activity), wait until the last 5 business days of the quarter to apply

If your file is strong (FICO 740+, clean utilization), you'll get approved on any day, but applying on a quarter-end day routinely increases your approved limit by 30-60%

If you've been denied recently, the same product at the same bank reapplied on the next quarter-end day often approves. The exception queue is run by humans who manually override the model's prior decision

The year-end walk-in script:

Walk into a branch December 29 or 30 at 10am. Ask for the small business banker. Open with: "I'm closing out the year and consolidating my business banking relationships. I'd like to apply for [specific product] and discuss the year-ahead opportunities for our relationship"

You just signaled: deposit relationship coming, multi-product interest, expansion mindset, quarter-end timing

The banker now has variable compensation incentive to make this work for you. They will route your application through manual underwriting. They will negotiate the limit up the chain. They will call the underwriting desk for an exception if needed. They want your application approved as much as you do because their bonus depends on it

A client ran the year-end loop last December. December 29 walked into Chase. Applied for both Chase Ink products plus moved business checking from BoA. Approved $68K combined. December 30 walked into Wells Fargo. Applied for Business Cash. Approved $45K. December 31 walked into BoA (still has accounts there). Applied for Business Advantage. Approved $42K

3 banks, 3 days, $155K in 0% credit, 0% APR for 12-15 months. Same FICO as 11 days earlier when an online application got him $32K total

The 4 dates aren't a secret. They're public information. The fiscal quarter system is the same one every public company runs on. Banks just don't advertise that their internal scoring relaxes when the team is chasing targets

You can apply 361 days a year and accept the regular price

Or you can apply on the 4 days a year when the bank is the customer

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

English

What is IB Trading & How to Master the IB50 Entry Method

Ever see myself or other traders post “IB remains GOATED ” with clean wins on $ES, $NQ, $MYM, or forex pairs? That’s Initial Balance (IB) Trading — one of the highest-probability intraday strategies in futures and forex.

What exactly is the Initial Balance (IB)?

The IB is the high and low price range set in the first 60 minutes of the regular trading session (9:30–10:30 AM ET for U.S. futures/indices).

IB High = highest price in that hour

IB Low = lowest price in that hour

IB50 = the exact 50% midpoint of that range (the “sweet spot” for entries)

This range shows where big players first “balance” supply and demand after the open. It’s NOT random — it’s auction theory in action.

Quick History Lesson

IB trading comes straight from Market Profile, pioneered in the early 1980s by J. Peter Steidlmayer at the Chicago Board of Trade (CBOT).

Steidlmayer created a way to visualize price + time + volume as a bell curve (the “profile”). The first hour became known as the Initial Balance — the foundation institutions use to decide if the day will trend or rotate.

What started as floor-trader wisdom in the 80s is now a core edge for modern day traders using futures, indices, and even London/NY forex sessions.

The IB50 Entry Method

This is the “IB by Rejection” setup — statistically one of the cleanest edges out there (~70-75% probability in many studies). How it works step-by-step: Wait for the full 9:30–10:30 ET IB to form (or London open for forex).

Watch which extreme forms first (high or low).

Look for a breakout + rejection of that extreme (price pokes out then snaps back).

Enter at or near the IB50 (50% level) in the direction of the opposite side.

Target: the opposite IB extreme (or 1.5–2x the IB range extension).

You can even front-run the 50% slightly (e.g., enter 10:23–10:27) if the candle is closing near it

Why IB50 Works So Well

High win rate on single-direction days (67–75% of the time the market picks a side after the first hour and sticks with it).

Built-in risk: stop usually just beyond the rejected extreme or opposite side of IB.

Works across $ES, $NQ, $MYM, $RTY, $GC, $CL, and forex $USDJPY $GBPUSD $EURUSD (London IB too).

Perfect for scalping micros or swinging bigger size.

Pro tip: Respect the money. Take the 50–150 point winner instead of holding for the moon.

Risk Management & Pro Tips

Only trade when IB aligns

Avoid choppy days or wide-range news days.

Use limit orders near IB50 — don’t chase.

Start small on a funded account

use @edgeful to find IB stats easily

$ES $SPY $SPX $MNQ $NQ $QQQ $RTY $IWM $MYM $YM $DJIA $BTC $BTCUSD $BTCUSDT $ETH $DOGE $XRP #trading #stocks #qqq #mnq #mq #es #mes #spy #spx #bitcoin #crypto #btc #djia #ym #mym #rty #wm #m2k #dxy #usdjpy #forex #eurusd #oil #mcl #cl #ethereum #xrp

English

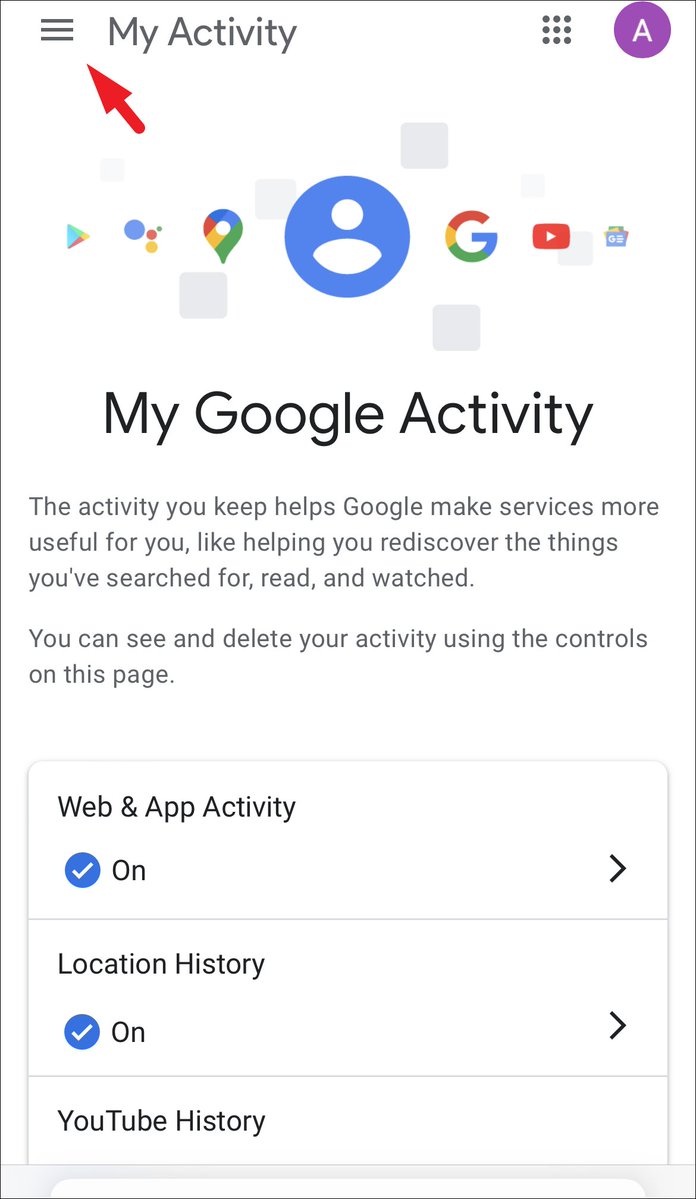

Google has a recording of every search you've ever made.

Every place you've ever been.

Every YouTube video you've ever watched.

Go to myactivity.google.com right now.

You'll find searches from 2015. Voice recordings. GPS coordinates.

All stored. All linked to your name.

A decade of your life is sitting in one file. Here's how to see it and delete it:

English

This $SPY 0–1DTE strategy is all you need:

Previous Day High/Low + 15 min ORB

Simple. Repeatable. High probability.

Here’s exactly how I trade it 🧵👇

English