@Million_Sancet What do you think will happen once earnings are announced? Will there likely be a drop for people to get in on Friday?

English

Bradley Murphy

27 posts

@mur60674

keeping up with legal Twitter!

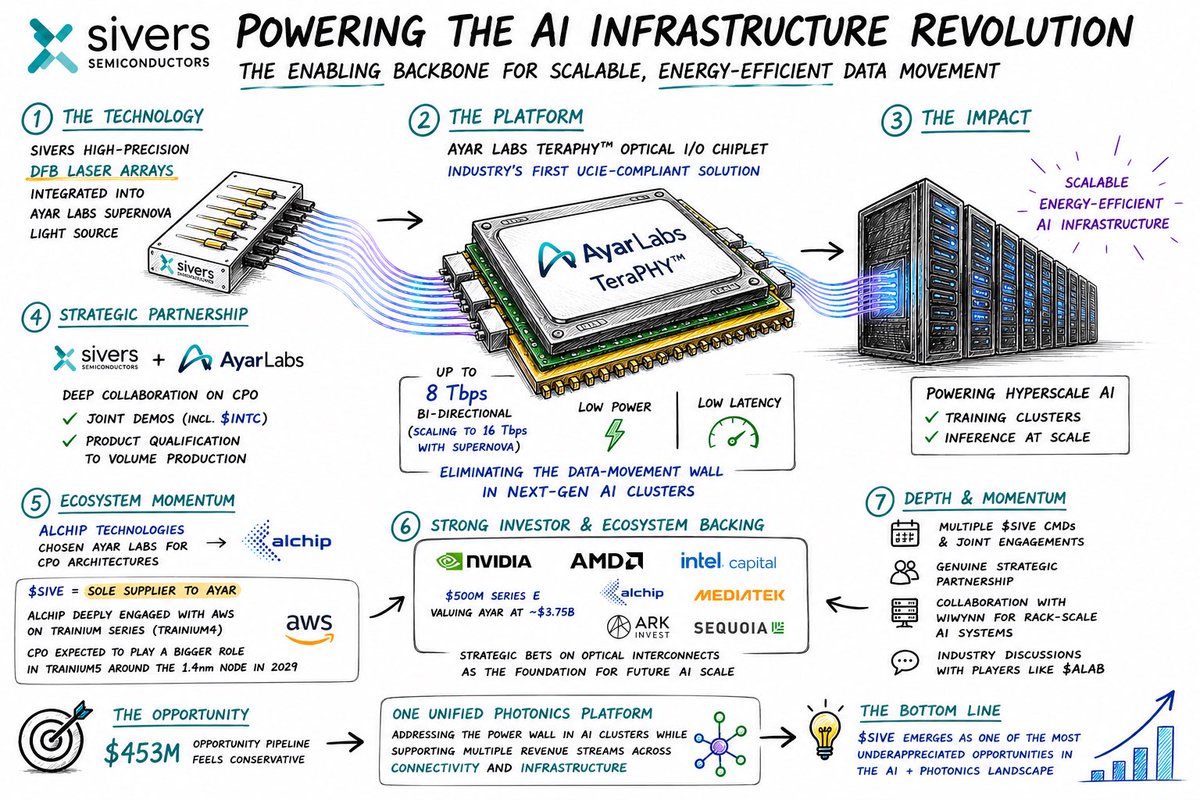

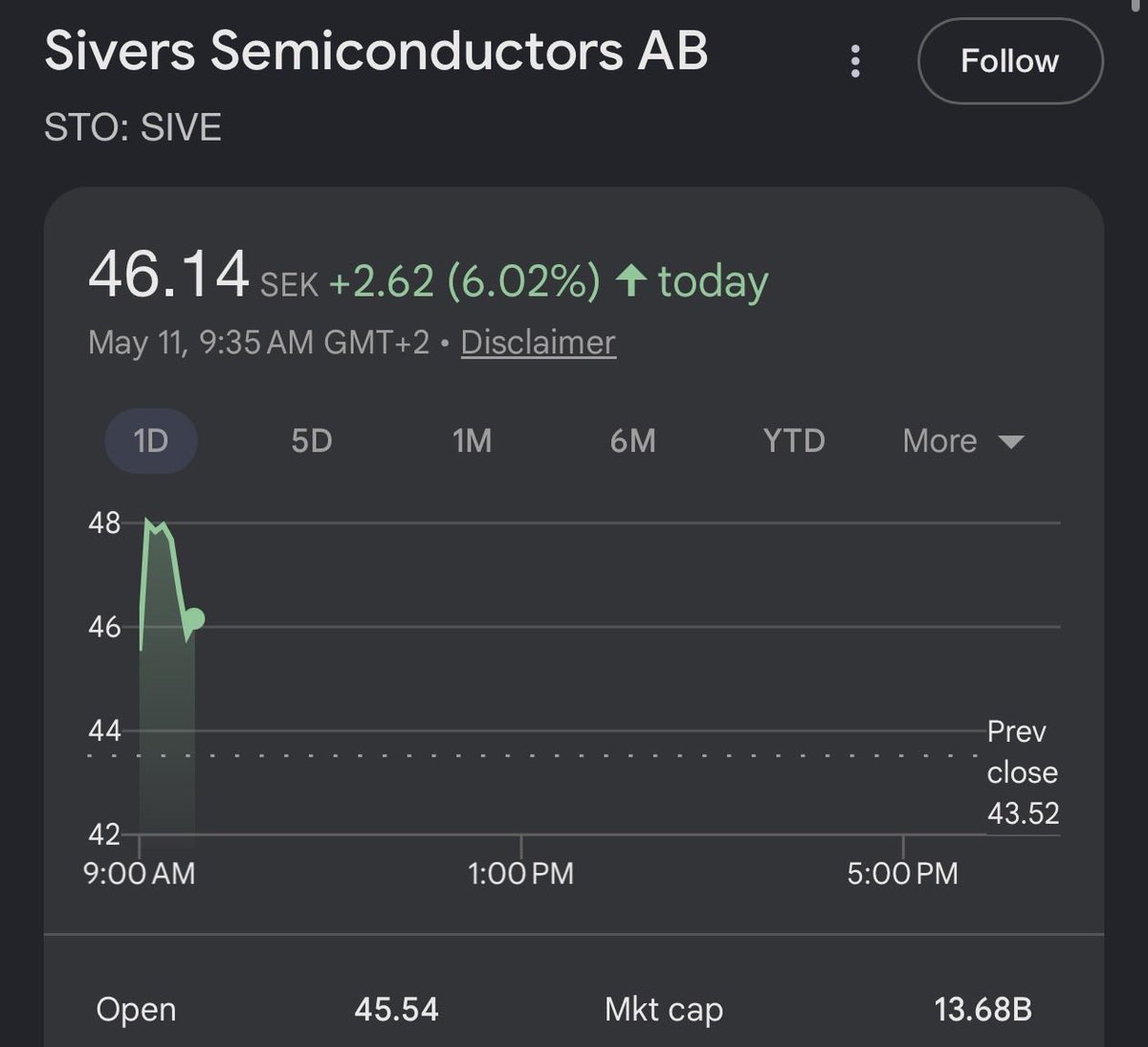

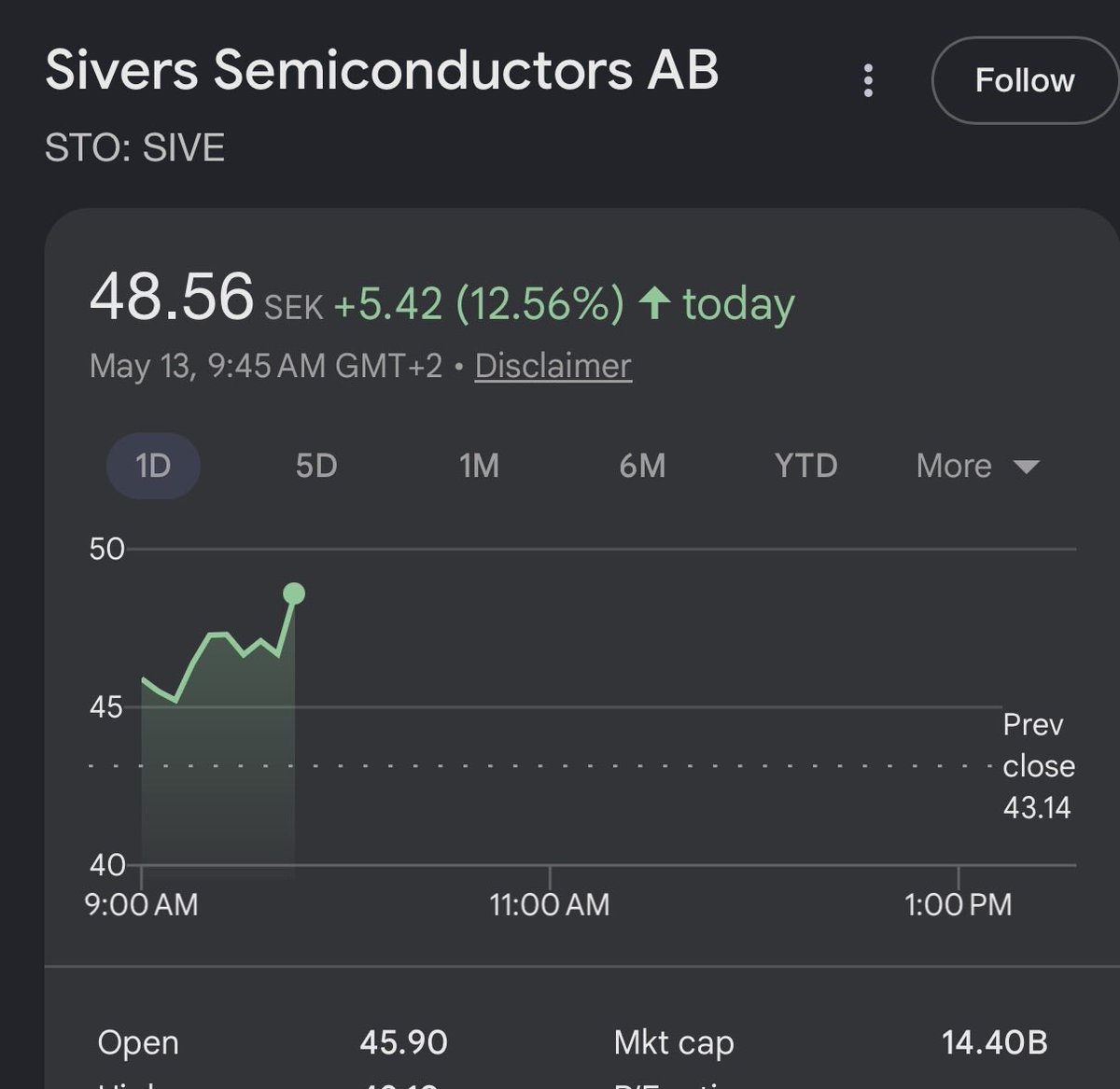

For $SIVE to become the next $80B+ $LITE. Sivers is the current laser kingmaker of the optical transition to CPO and 1.6T. They basically supply lasers to the leading players in the CPO space. From likely $MRVL Celestial, Lightmatter, Lightelligence, $POET, and others for CPO. before they got big. And now with large players like $JBL for 1.6T LRO + more test/qualifications underway for pluggables. They've finally solved the Catch22 problem, and have the attention of the market to pull off foundational CPO related IP acquisitions downstream on NASDAQ listing (or now with equity). And expand revenue as much as possible from the laser source into: -> Optical Engine/ELS value. -> Optical Transceiver IP Just like $LITE did to drive their valuations from $2B -> $80B in 2 years. But instead of EML + pluggables, Sivers is doing this for the CPO supercycle, the fastest TAM expansion in history for photonics. I'm following the story for them to pull this off this David vs. Goliath shift catching up to $LITE. More than I care about little MC % returns that's happening currently.

This vicar doesn't hold back on Tommy Robinson.

@aleabitoreddit So is $SIVE the best play for CPO

$SIVE se va a hundir. Buena suerte con los calentamientos que os dieron