@Aaronwei3n This is not what Nvidia CFO said though, in a follow-up interview after their earnings call:

finance.yahoo.com/news/nvidia-cf…

Where is your quote from?

English

sigma capitalist

389 posts

@phithetasigma

tech nerd 🤓 building my own trading/invt portfolio after 20+ years in sell-side IB & equities. not investment/financial advice. DYOR

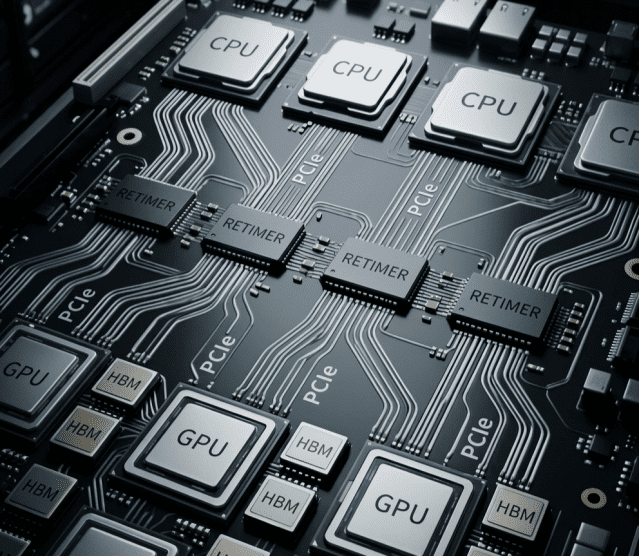

An interesting shift in data center architecture emerged from $NVDA ’s latest earnings. The company expects $20B in revenue this year from its Vera CPU infrastructure. Meaning NVIDIA, in its very first year of selling CPUs, is already on track to become the world’s largest data center CPU vendor.

JX Advanced Metals $5016.T • Raised ¥250B ($1.6B) from two equal-sized convertible bond tranches, one maturing in 2029 and the other in 2031 • The zero-coupon convertible bonds were offered at the top of the marketed range (113.25% for the 2029 bond against 111.5% - 113.25% range; 114% for the 2031 bond, against 112% - 114% range). Issue prices for the 2029 / 2031 bond were at 110.75% / 111.5%. What this means is JX had effectively sold these bonds at a premium to par • Conversion price was set at a 20% premium to the reference close on Monday, i.e. at ¥4,860/share • Shares underlying the CB = 51,440,329, versus the tender offer size of 57,300,022 shares. That is, JX is buying back more shares (from ENEOS/other minorities) that it is effectively issuing - at a 20% conversion premium - as a forward pursuant to the CB. The CBs may or may not be converted, which in the latter case, means JX's outstanding share count could potentially fall by max ~57.3M shares, ~6.2% of NOSH (good for EPS/ROE) The pricing terms underscore strong investor demand for JX paper As to why JX stock trades down today, I believe it's due to delta hedging by the hedge funds (perhaps with asset swaps for embedded call vol exposure)

I think HBM is a mistake.

OPENAI OFFERS $2M IN TOKENS TO EVERY CURRENT YC STARTUP The Information reports OpenAI is offering startups in the current Y Combinator batch $2M worth of OpenAI tokens in exchange for equity through a SAFE. Sam Altman announced the offer to YC founders and said he wants to see what “tokenmaxxing startups” build. The pilot covers the spring and summer YC batches, which together include hundreds of early-stage startups. For startups, the value is obvious: less cash burned on inference. For OpenAI, it gets equity exposure to a large batch of AI-native companies while keeping them building on OpenAI infrastructure.

Volcker shock incoming