@TradersParadise @eyedoctalk Congratulations guys

English

Theo Le Roux Coffee Afficionado

2.8K posts

@theoglr1

"Qualified SCA Barista | Coffee Taster | Public Speaker | Business Owner | Coffee Educator | Lifelong Learner"

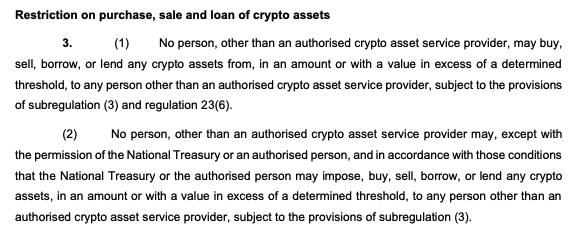

I am frankly dumbstruck by the news out of South Africa 🇿🇦 that newly proposed regulations would upend self custody in that country. South Africa's National Treasury has published draft Capital Flow Management Regulations (treasury.gov.za/public%20comme…) to replace its 1961 exchange-control regime, and the proposal extends sixty-five-year-old capital controls designed for gold bullion and foreign banknotes directly onto self-custodied crypto. The result is one of the most invasive treatments of non-custodial wallets proposed anywhere in the world. The mechanics are clear and severe. Any purchase, sale, loan, or transfer of crypto above a Treasury-set threshold must run through a licensed "authorised crypto asset service provider." Cross-border movement of crypto requires permission. Holdings above the threshold must be declared within thirty days, and Treasury can compel their sale at market price. Crypto can be attached by administrative order, without prior judicial process, on reasonable suspicion of contravention. Penalties run to R1 million, five years in prison, or the full value of the crypto involved. The provision that is the real showstopper is Regulation 25(5). Where crypto has been forfeited to the state, the owner must "furnish full particulars in writing of all and any passwords, personal identification numbers or codes" necessary to give Treasury access. That seems to be a statutory compelled disclosure of seed phrases and private keys. There is no carve-out, no judicial check inside the regulation itself, no recognition that the keys are not separable from the user's right against self-incrimination or right to privacy under the South African Constitution. The reason that provision appears to exist is Treasury understands that, without it, the rest of the framework cannot reach a self-custody user. Exchange-control logic depends on gatekeepers — banks, dealers, intermediaries that the state can appoint and command. Self-custody removes the gatekeeper by design. So the regulation reaches the only places it still can: the on-ramp, the holder's declaration, and ultimately the holder's body and devices at the border. Regulations 4 and 5 give enforcement officers the power to search travelers entering or leaving the country, demand they "produce" any crypto in their possession or control, and seize it on suspicion alone. As you well know, this is not how most of the rest of the world is approaching self-custody. The EU's Markets in Crypto-Assets framework regulates issuers and crypto-asset service providers and explicitly leaves self-custody alone. The UK's financial services regime regulates exchanges and custodians and treats unhosted wallet software as out of scope. The US has spent the last two years walking back its most aggressive theories — the SAB 121 reversal, the broker-dealer rule rollback, the IRS DeFi broker rule rescission — precisely because policymakers across both parties recognized that you cannot regulate non-custodial software the way you regulate a bank. FATF's own guidance distinguishes wallet software publishers from custodial intermediaries. South Africa's draft does the opposite. It very much intends to reach through the software to the user. The technical reality the draft ignores is that a non-custodial wallet is a key-management tool, not a financial intermediary. @MetaMask does not hold user funds. It does not see private keys. It cannot freeze, seize, or surrender anything to a regulator. Compelling its users to declare, surrender, or hand over keys does not make Treasury more effective at managing capital flows. It makes ordinary South Africans criminally liable for using software the rest of the world treats as legitimate self-custody infrastructure. Treasury has opened a public comment period, and anyone with a dog in the fight should ask that the compelled-key provision be struck. The cross-border search-and-seizure regime should not extend to self-custodied wallets. And the framework should distinguish — as nearly every other major jurisdiction now does — between intermediated services and the user's own software.

I don’t think people truly understand what’s about to happen with 𝕏 Money. This is Elon going back to his roots - back to x.com - and building what he always wanted in the first place: one place that runs your entire financial life. When he rebranded Twitter to 𝕏 in 2023, he said straight up that we’re adding the ability to conduct your entire financial world. He even said you may not even need a traditional bank account. Most people brushed that off. And now it’s becoming real. 𝕏 Money has already been live in closed beta internally within the company. A limited external beta is expected soon, and they’ve already secured money transmitter licenses in over 40 states plus DC. 𝕏 Payments is registered with FinCEN. Visa is officially partnered. You’ll be able to fund your wallet instantly, send peer-to-peer payments, move money to your bank, and eventually use a debit card. And I think this is just the beginning. This will probably start as a simple wallet where you can send money as easily as sending a DM. With this technology, you can pay creators, pay subscriptions, pay whatever bills, shop inside the app, get paid inside the app, and much more. Then, there will be high-yield savings, you can invest, you can get loans, have money market accounts, maybe even treasury access, cool smart cashtags that let you see live stock prices in your timeline and execute trades seamlessly, crypto integration, potentially full asset management… the list goes on and on… Elon literally said this is meant to be the central source of ALL monetary transactions. Bro… think about that for a sec. Your 𝕏 profile becomes your financial identity. Everyone you follow is already there. Everyone you interact with is already there. That social graph becomes your distribution engine. Like, you won’t need a separate banking app, no need for a separate investing app, no need for a separate payment app… this all lives where you already spend your time. Right here on 𝕏. Look at WeChat in China, which Elon always alluded to. Payments, messaging, shopping, investing - all integrated in one app. It handles $ trillions in volume and became deeply embedded in everyone’s daily life. Now 𝕏 is building the Western version of that, but with a more global reach, and xAI’s AI layered on top of all this. Before you call me crazy, you have to understand how big this opportunity is. Digital payments globally are measured in the tens of $ trillions of dollars annually. Even just capturing a small slice of that across hundreds of millions, and eventually a billion, users can change everything. 𝕏 already has the audience. That lowers customer acquisition costs significantly. Add fintech revenue on top of ads, plus float, plus lending, plus investing tools, and we’re talking about a completely different valuation profile. Now, $44B for this company looks like the bargain of the decade… this was one of the main reasons I invested in 𝕏. And if they execute the way they’ve executed at Tesla and SpaceX, this could truly fundamentally redefine how people handle $ . Most people today still see 𝕏 as just a social media app. I see it as the foundation of a financial system layered on top of a global network. Ultimately becoming the “everything” app. And this I believe is a once-in-a-generation opportunity. Elon is calling this a game-changer. I believe him.