@uphillmarket_ @wliang $0.60 to $$2.30 in a couple months is an insane run. Needs to consolidate a bit

English

Jim

226 posts

So I posted $MU back in August 2025 when it was sitting around ~$118, calling a soon-to-come reversal from that choppiness. Two weeks later, the first Startup.io buy-signal came in at ~$130. We're sitting at $746 today (~570%). Not a bad 8 month return on a large cap... Back in August, $MU was sitting near 52-week lows around $130B MC. CHIPS Act funding was still uncertain, and this whole AI memory thesis was still pretty speculative. Again, sometimes technicals come in faster than fundamentals... so let's see what fundamentally changed after our buy signal: > HBM3E became the dominant growth driver, and HBM4 ramping into 2026. Huge shortage, and hyperscalers (+ $NVDA and $AMD) were literally fighting for allocations. > DRAM/NAND prices surged 4-10x. Capacity got pulled toward HBM and the rest of the market got squeezed. > Big Tech started locking in 2027 NAND allocations... $MU's CEO confirming customers receive only "50% to two-thirds of their requirements." Reaffirming the structural supply deficit until 2027. > CHIPS Act delivered $6.1B in finalized funding for $MU. > Agentic AI workloads tripled CPU demand overnight. GPU-to-CPU ratio went from 8:1 toward 1:1, sending HBM demand for $NVDA and $AMD GPUs through the roof. Very little of this was priced in back then. > $725B in confirmed Mag 7 AI capex for 2026 alone as mentioned in previous posts - $META, $GOOGL, $MSFT, and $AMZN. Now, $MU is at an ~$840B MC and one of the top 10 most valuable U.S. tech companies in the world. People buying here might still be early (DA Davidson just set a $1,000 price target)... But anyone who followed me back then absolutely printed. I told you before, it pays to pay attention. As usual, I'll do my best to explain the fundamental thesis and technical alignment on any trades taken. Don't miss the next run.

$SLNH @SolunaHoldings CFO Michael Picchi just bought 100,000 shares (21/05) of Soluna on the open market at an average price of $1.632, worth roughly $163k. After the purchase, he owns 1,381,250 shares. This is the CFO putting real money into the stock shortly after joining Soluna at what could be the most important inflection point in the company’s history. Picchi was appointed CFO in January 2026 to support Soluna’s capital strategy as the company scales its behind-the-meter, renewable-powered data center model and expands into AI infrastructure. His background is directly relevant: • Former CFO / CAO at TECFusions, a sustainable high-density AI infrastructure/data center developer • 30+ years of finance experience • Capital formation • Debt and equity financing • M&A • Infrastructure and energy-adjacent businesses Soluna is now moving from a small Bitcoin/renewable data center operator into a larger AI/HPC infrastructure story, with major project financing, customer announcements, and Q2 catalysts ahead. When the CFO with this background buys shares in the open market, investors should at least pay attention. Form 4: sec.gov/Archives/edgar… CFO appointment: solunacomputing.com/news/michael-p…

I think the SpaceX IPO trade will create a LOT of new millionaires in 2026. $ASTS to $200+ $PL to $100+ $RDW to $20+ $RKLB to $200+ Will be choosing my favorite tickers soon and charting them daily... 🫡📈

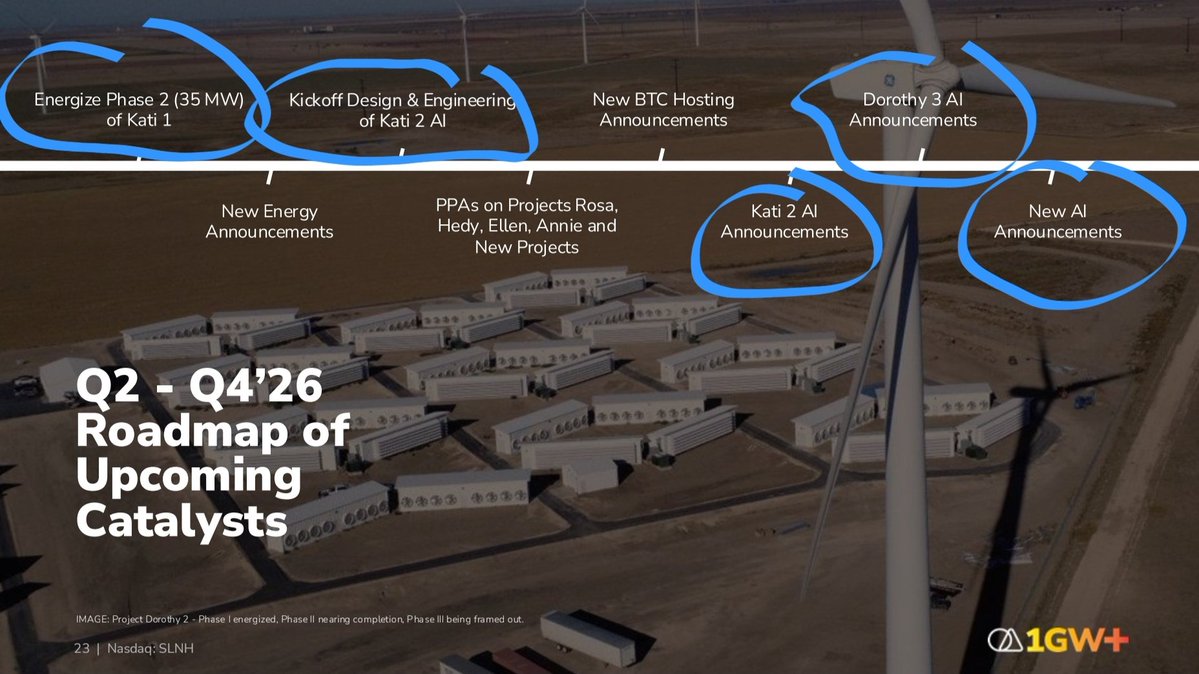

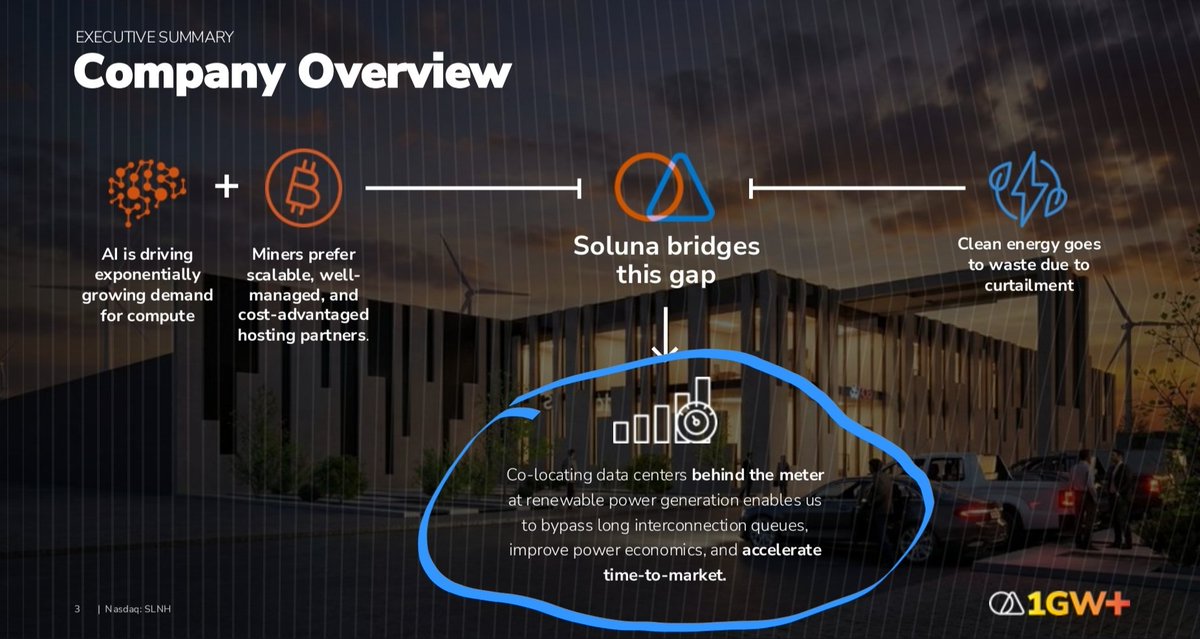

$SLNH @SolunaHoldings Big update from Soluna today. Soluna acquired the remaining 49% of Project Dorothy 1B for ~$8.8M, giving the company 100% ownership of D1B and completing the equity consolidation of the Dorothy 1 campus. This directly connects to what John said in the Q1 McNallie Money interview: Soluna does not want to sell its strategic power assets. They want to consolidate ownership, gain control, and convert the best campuses into AI/HPC infrastructure. With Briscoe Wind Farm providing 150 MW of owned renewable power and now 100% control of both Dorothy 1A and 1B, Soluna says it has assembled the full generation-to-compute ownership chain for 50 MW at Dorothy 1. That matters because the company specifically said this unencumbered ownership is a prerequisite for converting the campus to AI/HPC workloads and marketing Dorothy 3 to prospective AI customers. @jbelizaireCEO ’s quote today says it all: “We can now decide when and how we convert, bring in the right partners on our terms, and present Dorothy 3 to AI customers as a fully controlled, powered campus.” This is exactly the AI transformation thesis from the interview: ▪︎ More control ▪︎More vertical integration ▪︎ More power ownership ▪︎ Better AI/HPC optionality ▪︎ Stronger position with future customers Soluna is not just adding assets. They are building a controlled power-to-compute platform.

$SLNH One of the most important parts of Soluna’s McNallie Money interview was the financing discussion around Kati 2. This is where the AI/HPC story starts to move from hype to real infrastructure economics. CFO Michael Peachey made the scale very clear: «“Kati 2 just for phase one would be $1.0 billion to $1.2 billion.”» That is only phase 1. The reason is simple: AI/HPC data centers are not Bitcoin mining capex. Anthony framed it perfectly: «“We’re not talking Bitcoin mining numbers here, we’re talking HPC numbers.”» AI/HPC buildout costs were discussed around $10–12M per MW. So Kati 2 phase 1, targeting roughly 100 MW IT, could represent a $1.0–1.2B infrastructure project. That is the scale many investors still do not understand. This is not about adding a few more Bitcoin containers. This is about Soluna trying to move into billion-dollar AI/HPC data center development. The key question is obvious: How does a company of Soluna’s current size finance a project this large? Peachey answered that directly. «“We do think we’ll be able to get 80% funding on the debt side of it.”» That matters. If phase 1 costs $1.0–1.2B, then 80% debt could imply roughly: • $800–960M debt • $200–240M equity Still a large equity requirement, but very different from funding the whole project with common equity. And importantly, the equity may not all need to come at the Soluna Holdings level. Peachey also said: «“Conversely, we might accept an equity investor to partner with us at the Kati 2 level.”» That is a key point. A project-level equity partner could reduce parent-level dilution while still allowing Soluna to develop the asset. This is why the first AI/HPC lease is so important. Without a lease, Kati 2 is still a development project. With a lease, Soluna gets: • A customer • Contract value • A clearer construction timeline • Financing visibility • Bankability • A path to capital formation John said it clearly earlier: «“Once that lease is signed… we now have to go do capital formation.”» That is the real unlock. The market should not look at future capital raises in a simplistic way. There is bad dilution, and there is growth capital. Bad dilution = raising equity just to fund losses. Potentially value-creating capital = raising equity/debt around a signed AI/HPC lease to finance a contracted billion-dollar infrastructure asset. That is a completely different situation. Peachey also said Soluna raised $142M in fresh capital in 2025 through multiple sources, including ATM, share equity purchase agreement and project-level debt. Then he called it: «“A dry run for 2026.”» That tells me management sees 2026 as the year where capital formation becomes much larger and more directly tied to AI/HPC. Another key quote: «“I do think we would do it in phases.”» That lowers initial risk. Soluna is not talking about building all of Kati 2 at once. The first contract is expected to focus on the first 100 MW. Then future expansion could follow. Peachey said the next phase could be another 250 MW, requiring an additional $2.5–3B. But he also made an important point: «“At the time we go back to raise money for that next incremental 250 megawatts… the company Soluna will be much, much larger.”» That is the core of the bull case. If Soluna lands a major AI/HPC lease, starts construction, and shows a credible financing path, the company may no longer be valued like a small Bitcoin hosting name. It could begin to be valued as an emerging AI power/data center infrastructure platform.

$AMPG just received full FCC and ISED Canada certifications for their 5G Native DAS Solution. Their entire hardware stack is now approved for commercial sale across North America. Phase 1 of the valuation gap fill towards $1B MC... still 10x away. Did you listen?

Plenty of people ignored me. If you didn’t, you made an insane amount. I hope you never doubt me again… March 30th $SATL was at $2.96. May 18th $SATL is at $9.54. I wouldn’t miss the next trade. Tomorrow.

$SLNH TECHNICALS: - FALLING WEDGE (REVERSAL PATTERN) - DEMAND ZONE (REVERSAL) - PSYCHOLOGICAL SUPPORT (STRONG SUPPORT) THIS IS MY USUAL A+ SETUP, DON'T KNOW MUCH ABOUT THE COMPANY, BUT TECHNICALLY BULLISH! IMPORTANT LEVELS; $1.85 (STRONG SUPPORT) $1.99 (RESISTANCE) $2.35 $2.75