Sally struthers returns أُعيد تغريده

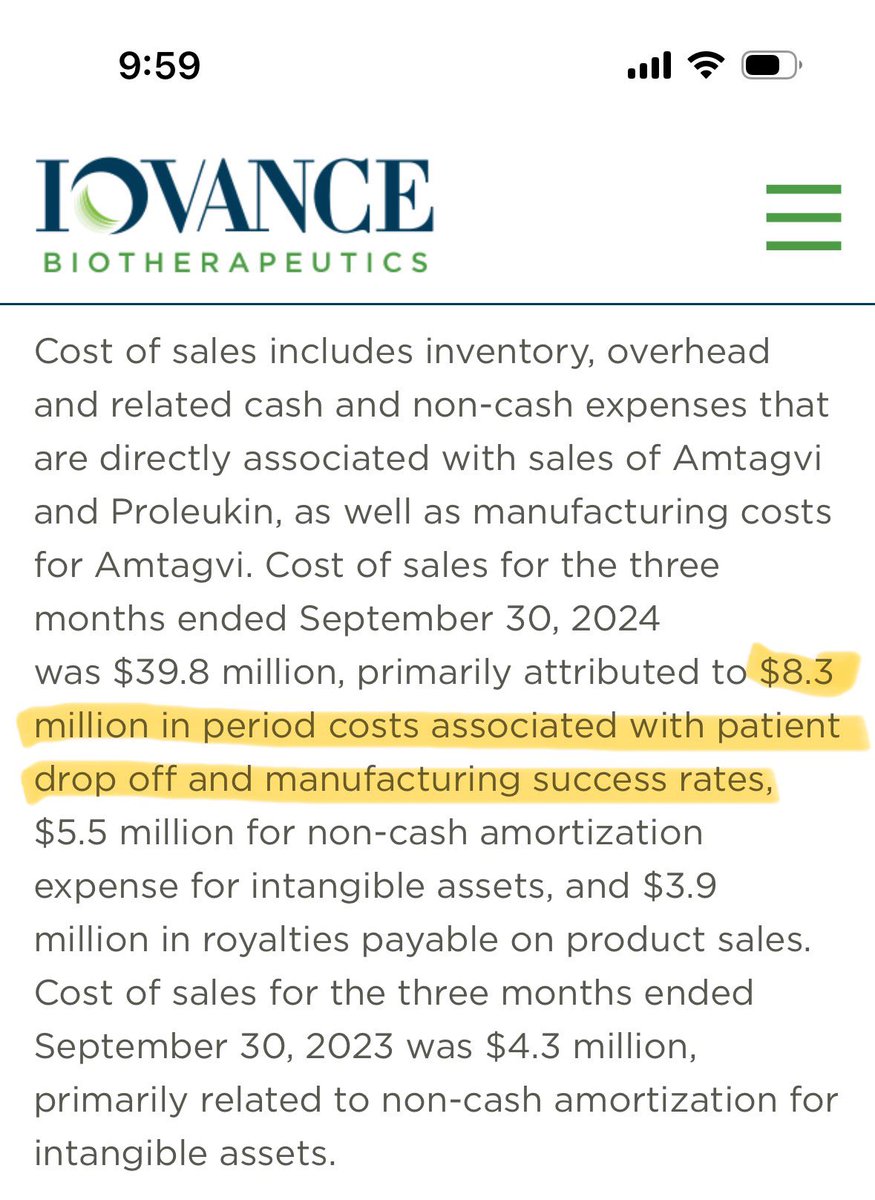

$IOVA is a gift at the current levels $3.80-$4. It will be over $10 by end of year. There are so many massive catalysts coming. Most importantly, Amtagvi adoption is accelerating and that means when NSCLC is approved sales will be through the roof. The sales and marketing infrastructure is already being built and fine tuned with the advanced melanoma indication. It will be a well oiled machine soon.

Patience…

English