@KawzInvests I share my real-time buy/sell TRADE alert on WhatsApp, free to join ✅

➡️Copy search input Reply “2026” to WhatsApp: 13137460891

Here’s the link : api.whatsapp.com/send?phone=131…!

English

KawzInvests 🦑-AuelyeiaPrecise Market Analysis

108 posts

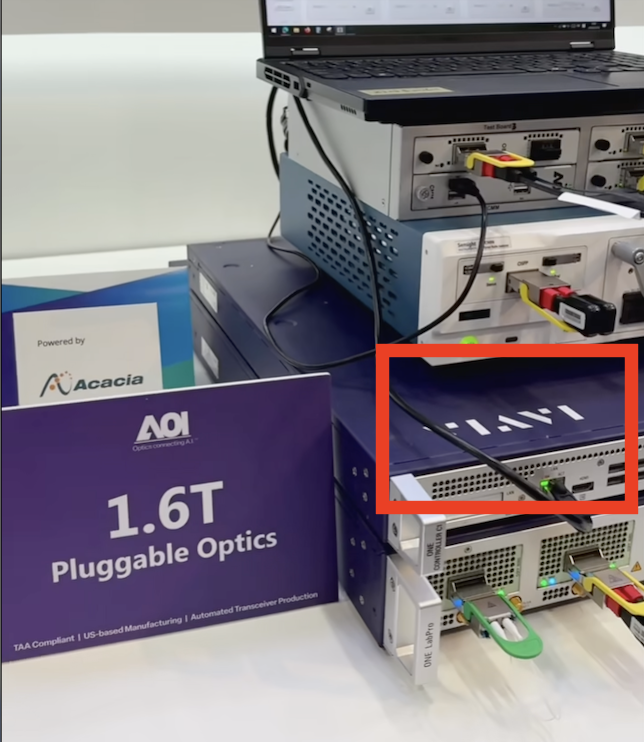

One question decides who wins the next decade of AI infrastructure. Who captures the 1.6T testing TAM? I asked a Cisco guy at GTC how $AAOI $LITE $COHR hold their margins when every new generation of optical parts does the work of four old ones. Fewer units should mean shrinking revenue. It doesn't. Every generation is harder to build and much more expensive per unit. The new high-power laser are priced at roughly four times the price of the older lasers it replaces. Fewer parts shipped, more dollars per part, margins expand. The same logic applies to the test equipment that validates every one of those parts before they ship. 400G test gear cannot test 1.6T. 1.6T gear cannot test 3.2T. Co-packaged optics adds an entirely new testing category that did not exist before. Fewer units, higher prices, new generations on an accelerating cadence. Interesting enough testing is just consolidated into a two-player market. $KEYS closed its $1.46B Spirent acquisition on October 15. The DOJ forced a divestiture of Spirent's high-speed Ethernet, network security, and channel emulation business, which $VIAV bought the next day for $425M. Three independent vendors became two. $VIAV $KEYS $COHR $LITE $AAOI