Rahul Sondhi@RahulMarkets

🚀 Trade Recap: $CPSH

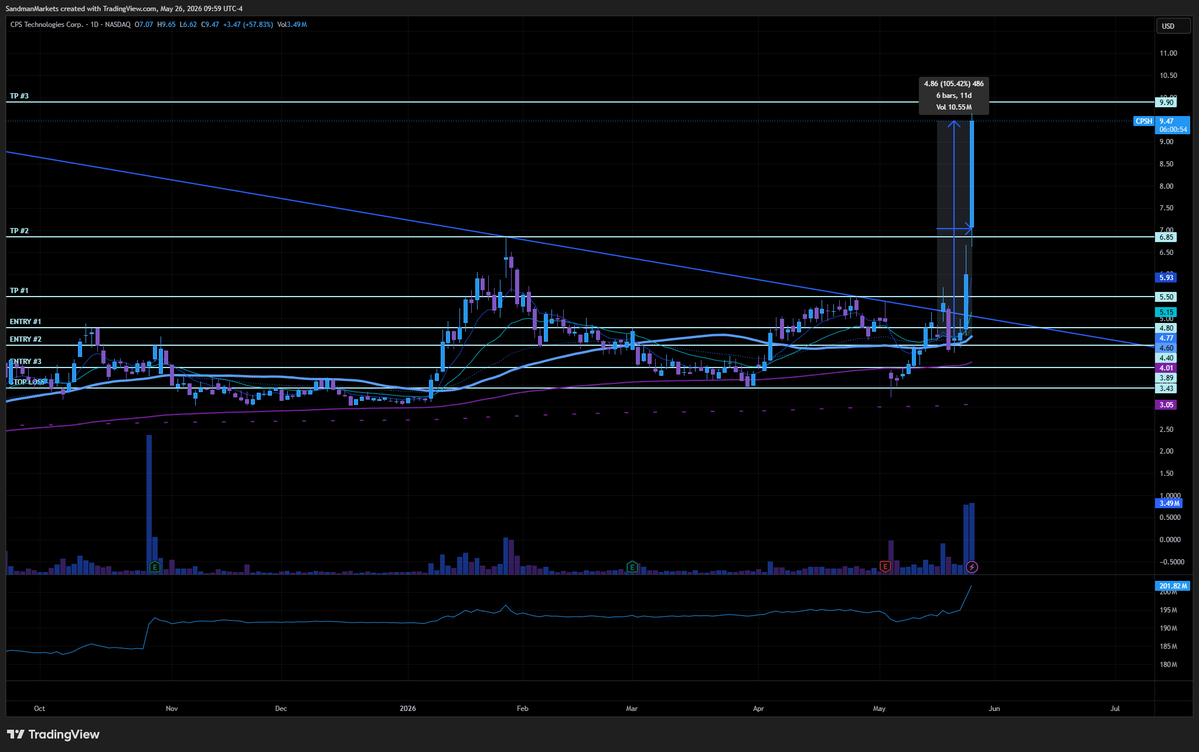

Before the market opened, I called out an entry on $CPSH at $6.75–$6.80.

🎯 Target: $10+

📈 Expected gain: 50%+

After the open, $CPSH surged to a high of $10.82.

✅ Peak gain: 75%+ in a single move

This wasn’t about chasing green candles — it was about identifying momentum early, managing risk, and letting the setup play out.

Entries matter. Timing matters. Execution matters.

Congrats to everyone who caught this move with me 👏

More importantly, stay disciplined. Protect profits and avoid getting emotional after big runs.

Who caught $CPSH today? 👇

#CPSH #Stocks #StockMarket #Trading #MomentumTrading