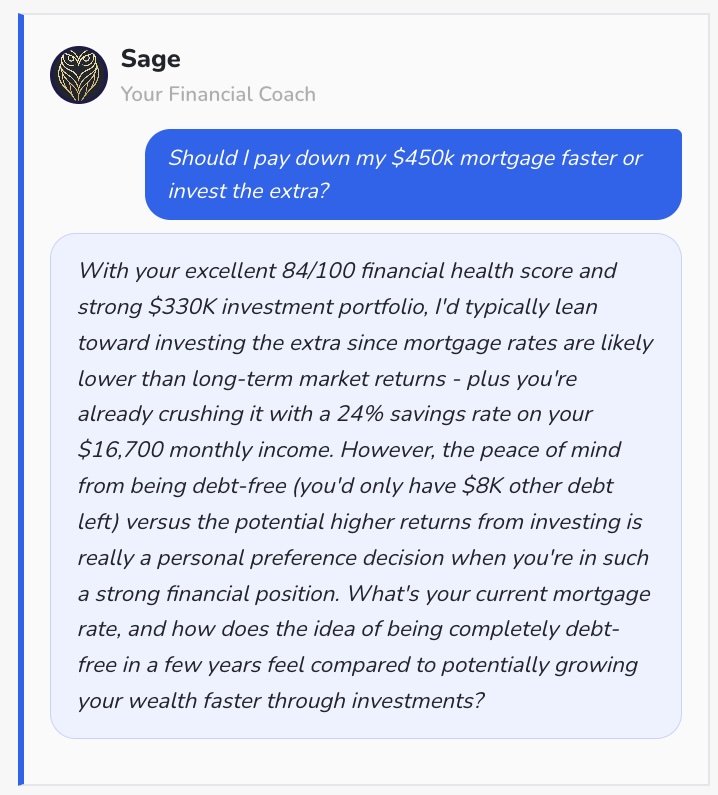

This is exactly the kind of question I see all the time from high earners:

“Should I pay down my $450k mortgage faster or invest the extra?”

Sage gives a solid, balanced answer — lean toward investing if rates are low, but peace of mind from being debt-free is personal.

But here’s what’s often missing: the *big picture impact* on when work actually becomes optional.

English