Aaron Webb retweetet

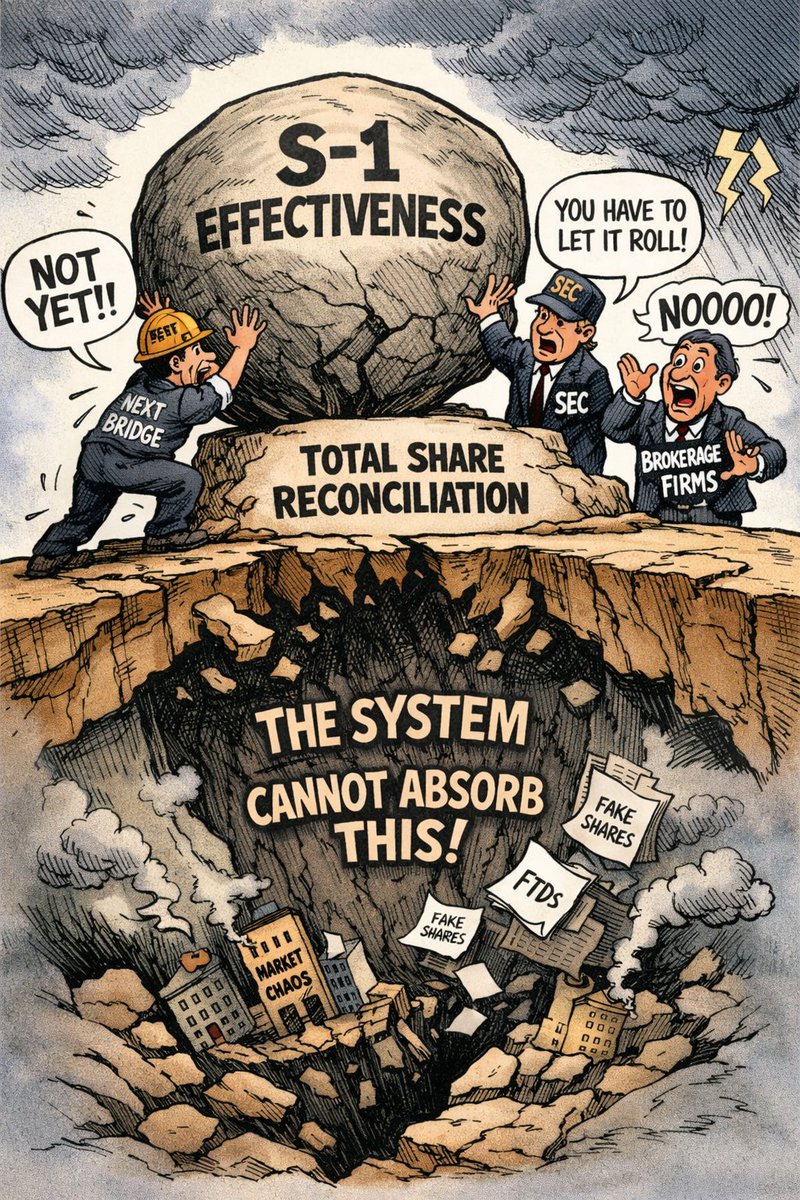

Delaying $MMTLP S-1 effectiveness looks counterintuitive at first.

Why do the work to get current, answer SEC comments, and clean up disclosures—only to pause at the end? Because S-1 effectiveness is not a finish line. It’s a trigger.

Once an S-1 is effective, it stops being a draft disclosure and becomes the legally relied upon source of truth for the company’s entire share reality. Not just new shares. All shares—authorized, outstanding, reserved, issuable—and how they’re distributed. From that point on, there can only be one truth and it must reconcile with real-world delivery through the transfer agent.

That’s the problem.

Today, share claims live in silos that don’t have to agree: broker customer ledgers, DTCC omnibus balances, transfer-agent records, issuer disclosures and FINRA halt data. A FINRA U3 halt freezes trading and prevents cleanup, but it does not erase those claims. It simply delays the moment when they must line up. S-1 effectiveness forces them to line up.

Important clarification: shares held at the transfer agent and shares held in broker street name are the same class of stock with the same legal entitlements. The difference is custody, not rights. Transfer agent shares are individually registered and strictly capped by authorization. Street-name shares are pooled, indirect claims that work only as long as totals reconcile.

When an S-1 goes effective, those two custody paths collide. The transfer agent can only issue up to the authorized amount. If broker street-name entitlements exceed that number, excess claims don’t become “pending”—they get rejected. That rejection creates a paper trail, and paper trails create liability.

With a U3 halt in place, there are no shock absorbers left. No trading. No buy-ins. No netting. No time decay. Only rejected entitlements and accountability. That’s why S-1 effectiveness is dangerous before reconciliation—and why pausing it is rational.

This is where safe sequencing matters. Safe sequencing means resolving share-entitlement risk before a document becomes legally binding, instead of using that document to force the resolution.

An S-1 delay creates space for only three real exits:

• Settlement, where mismatches are handled privately through cash, escrow, or claims processes before they become evidence.

• Position-close-only (PCO) trading, which can reduce excess claims—but only if it happens before effectiveness, not after the share count is certified.

• Forced reconciliation, via courts, regulators, or Congress—the least controlled outcome and the one everyone is trying to avoid.

Bottom line: an S-1 effectiveness pause isn’t stalling. It’s safe sequencing. Once the S-1 goes effective, the share count stops being a narrative and becomes evidence—and that’s a moment the system is trying to survive, not rush.

English