arun E.

173 posts

@Alpha_Condensed @googlecloud Yes, FinSights will be available to anyone who wants to subscribe.

English

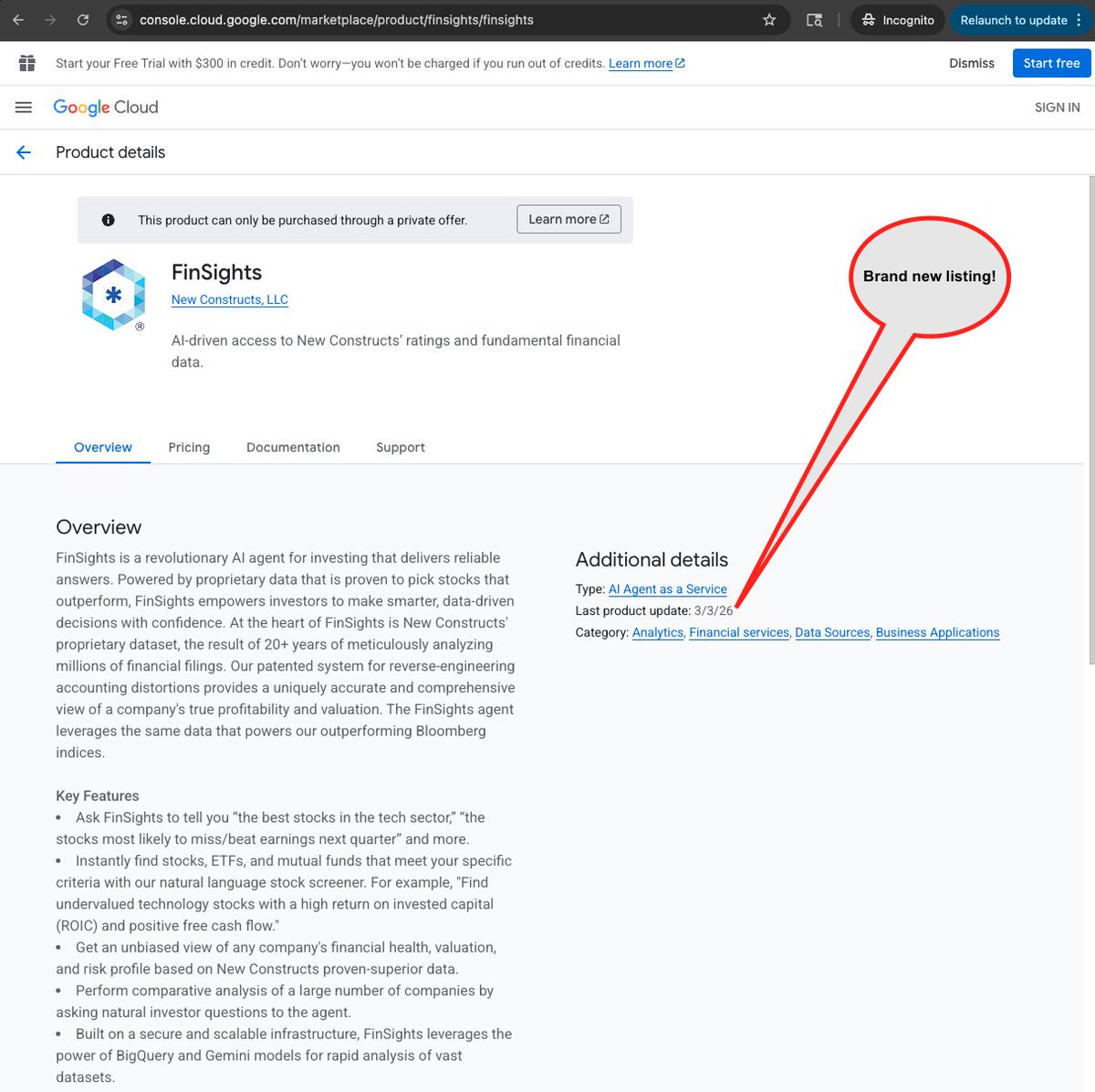

Guess what was officially published to the Google Cloud Marketplace this afternoon? FinSights. The AI Agent for Investing that @googlecloud paid us to build to show the Art of the Possible when combing our proprietary data with their tech.

console.cloud.google.com/marketplace/pr…

Huge thanks to @bradlittletx and his fantastic for making this happen.

English

@DDBlakeFischer @askjussi That’s straightforward to account for just assume reinvestment of dividends standard practice

English

@Alpha_Condensed @askjussi The S&P earnings growth is going to steeply outpace the reit ffo growth because REITs distribute the majority of ffo as dividends, whereas S&P constituents generally retain those earnings and reinvest them into their businesses

English

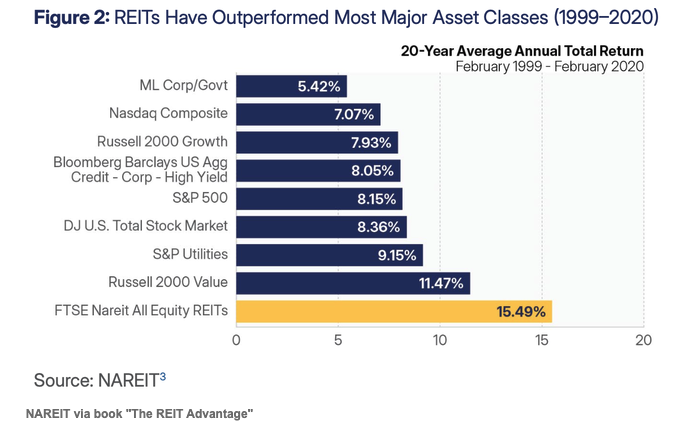

REITs just endured one of their worst 5-year stretches.

Recency bias now has many investors calling them “poor investments.”

But over 20 years pre-pandemic, REITs earned 15%+ annually, outperforming the S&P500, Tech, bonds, and gold.

The long-term math still works.

English

English

Time to tank more stocks

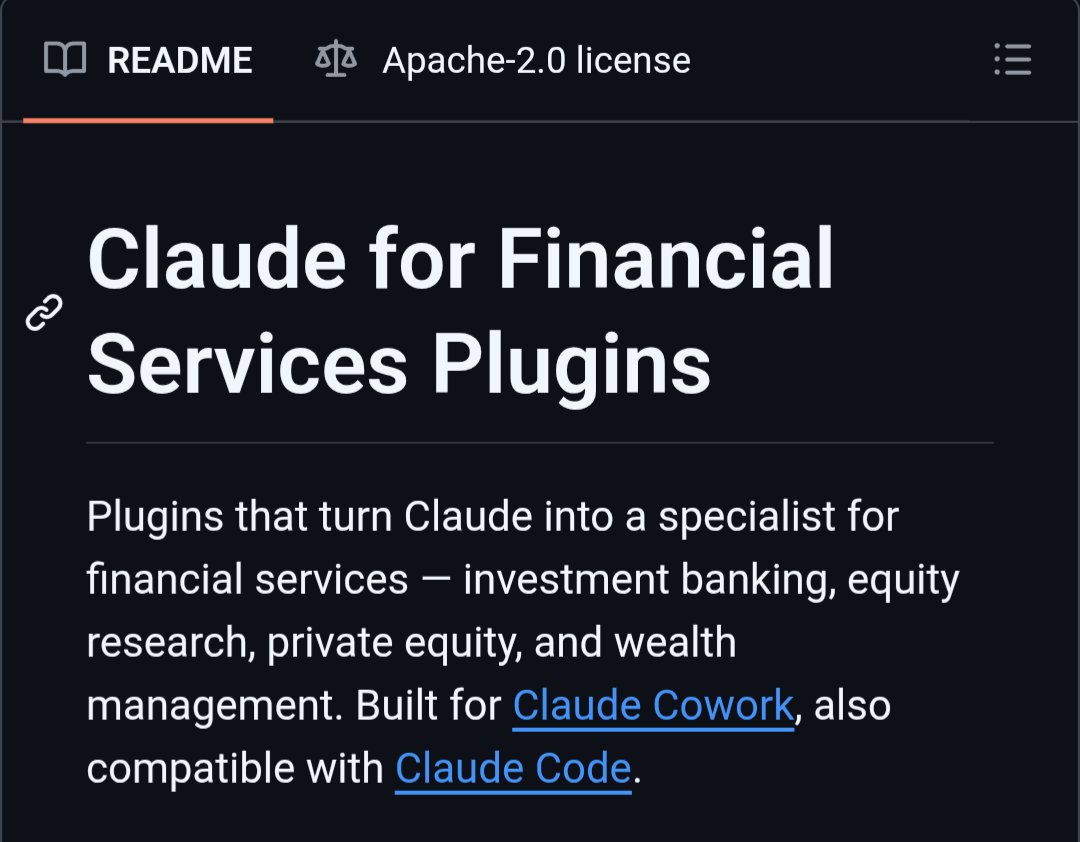

New Anthropic Repository for Financial Services

github.com/anthropics/fin…

English

I've used Claude Code to build 20+ projects in the last 6 months. Thousands of new users across them. And I've never written a single line of code.

I just dropped a 24-min video with my top 10 tips for non-developers — the exact playbook I use every day to run multiple AI agents that handle work that used to take me a full week.

This is the best beginner guide to learning and building with Claude Code out right now. Every tutorial I found assumes you're a developer. This one doesn't.

I cover everything from first install to running multi-agent workflows — with live demos and real examples for every single tip. How I set up new projects, how I got Claude to match my writing style, how I automate repeatable workflows with one command, and how I run multiple agents working on different tasks at the same time.

I also built a full resource repo to go alongside the video — curated video tutorials, the best skill libraries, plugin directories, MCP server guides, written docs, community links, and a starter CLAUDE.md template you can copy-paste into your first project today.

Comment "GUIDE" and I'll send you the full guide with everything you need to learn Claude Code!

(make sure we're connected so I can DM you)

English

There are no more software companies.

There are only ontologies now.

Antonio Linares@alc2022

Every industry is going to be dominated by an Ontology in 5 years. Predictions: 1. $HIMS ontology dominates healthcare. 2. $SPOT ontology dominates media. 3. $DUOL ontology dominates education. 4. $PLTR ontology dominates industry. 5. $TSLA ontology dominates autonomy.

English

My team went through and cleaned this sheet up to make it even clearer. I had made it years ago before I had people to help with this kind of thing, and so it's even easier to follow now:

docs.google.com/spreadsheets/d…

David Orr@orrdavid

I made this convenient spreadsheet so people can see my Seeking Alpha track record easily. It includes screen shots of when I said I quit each bet for each position in the article's comments. On average, longs beat the SPY by 42, and shorts 45%. docs.google.com/spreadsheets/d…

English

THIS STOCK SCREENER FINDS EVERY LEADER

$MU $SNDK $WMT $INTC $CCL $GME

It shows momentum before it’s obvious

I’ll share the screener RT + comment BANKS so I know who actually wants it

English

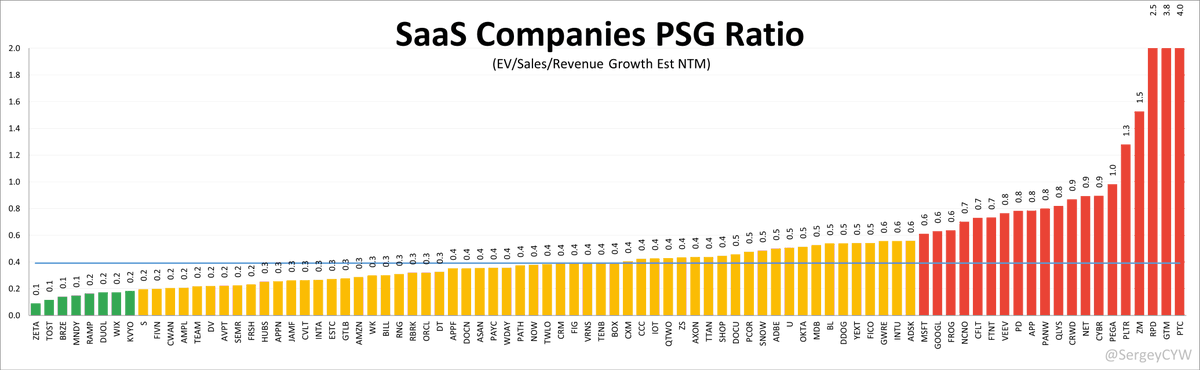

PSG offers a cleaner way to think about SaaS valuations

Price-to-Sales alone misses context.

PSG (EV/Sales ÷ NTM Revenue Growth) adjusts valuation for growth expectations.

This chart ranks SaaS companies by PSG, highlighting where the market may be paying too much — or too little — for growth.

Key observations:

• PSG dispersion is wide (~0.1 to 4.0)

• The market appears most comfortable around 0.3–0.6 PSG

• Above ~0.8, valuation assumes sustained execution

• >1.0 PSG requires exceptional durability or narrative support

Better positioned by PSG (growth relative to valuation):

$MSFT (~0.6)

$GOOGL (~0.6)

$DDOG (~0.6)

$ZS (~0.5)

Higher PSG / more demanding setups:

$PLTR (~3.8)

$SNOW (~0.9)

$CRWD (~0.9)

$NET (~1.0)

Interpretation framework:

• <0.4 → growth more than compensates for valuation

• 0.4–0.7 → fairly priced, execution matters

• >0.8 → expectations leave little margin for error

PSG doesn’t predict returns, but it clarifies where growth expectations are already embedded in the price.

English

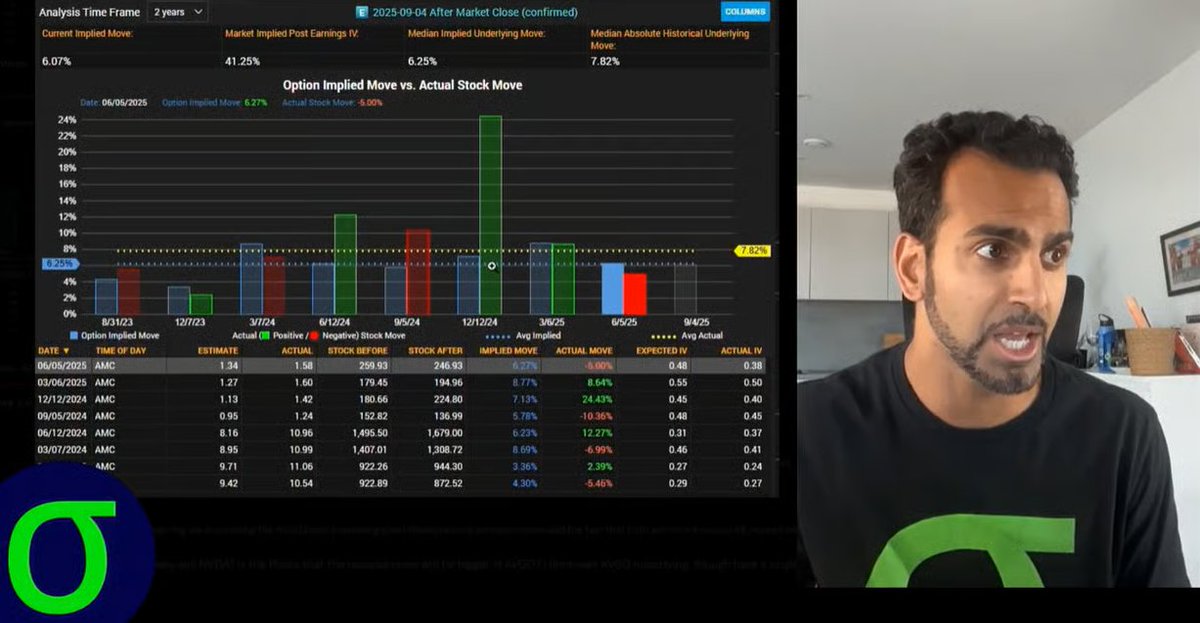

Earnings season’s here. Big moves expected and most option traders will get the structure wrong.

Buying a straight call before earnings looks asymmetric: limited downside, unlimited upside.

Reality: IV is pumped sky-high. You nail direction, the stock gaps your way... and you still lose or barely break even.

Why? Theta decay, then IV crush wipes out gains overnight.

Seen it a hundred times - right call, wrong result.

Real asymmetry comes from multi-leg setups: spreads, flies, calendars, diagonals.

These let you sell expensive premium, define risk, lean on dealer positioning, and navigate vol crush or path - not just direction.

That’s how we approach earnings: choosing structures that still work when you’re only mostly right.

If you want to see how we actually do this in practice, comment EARNINGS and I’ll send the video.

English

@KeithMcCullough Great what product has this ETF recommendations please

English

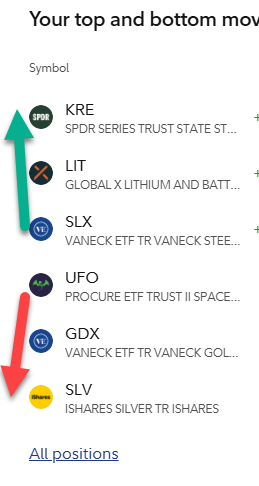

Here's what drove The Fam's All-Time Highs (Retirement Account)

The key here is diversification across Macro ETFs

Who else had Regional Banks and Lithium on their bingo card? They took over for Silver and $GDX

English

$ORR launched just 1 year ago and has already reached $245 million AUM. Thanks for putting so much trust into me, I do not take the responsibility lightly!

Learn more: militiaetf.com.

English

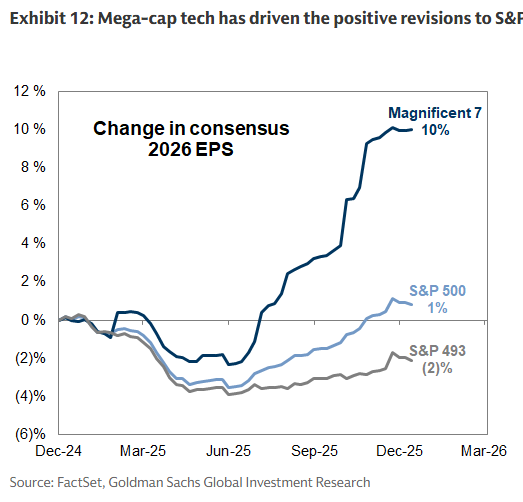

Not impressive S&P 493 earnings revisions lately GS

English

Weekend @Qullamaggie scan: Top 3% of stocks with the biggest price growth over the last month (sorted by dollar volume)

*I use the scan to find the best moving stocks I may have missed, add them to my watchlist, and wait for next entry opportunity

English

@realroseceline @CapexAndChill Awesome articulation of duration sensitivity 👏

English

Fair points, but too short sighted imo because Uber’s strategy only works if AV economics never get good enough to justify owning supply. If/when AV utilization improves and unit costs fall enough, the optimal model flips from aggregation to vertical integration, and the aggregators margin naturally collapses. I agree, demand volatility is a big deal, but capital markets can subsidize overcapacity for a very long time if the prize is platform control (ie market gave $Nflx a decade long hall pass). 🌹

English

Convinced $UBER bears have no idea what $UBER's strategy has been since they are hyper-focused on AV's killing them but I will share some thoughts...

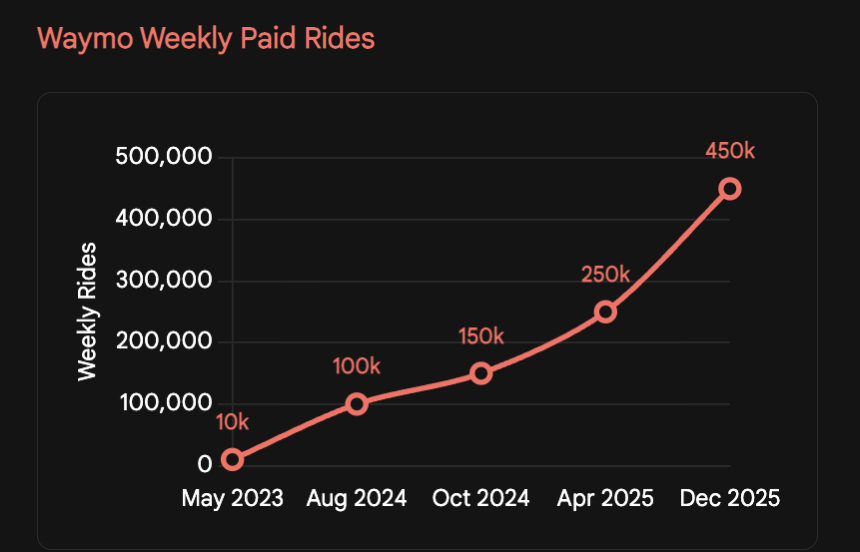

The Q3 '25 numbers... gross bookings are up 21% to nearly $50B. That doesn't look like a dying business. In fact, they are reaccelerating despite Waymo marketshare being the largest it has ever been in markets where it is not partnered with $UBER.

The logic of $UBER being the demand aggregator is very sound:

Utilization: Robots are expensive assets. You can't have them sitting idle. This will be tough for bears to understand 🤣 but the demand for ride-sharing fluctuates A LOT. Relying on AV networks would likely mean there would be an oversupply of AV's a majority of the time (and most of the time these depreciating assets will be fighting each other to fill demand during a majority of the non-peak hours)

How does Uber fix this issue? Uber uses AV's for the predictable base demand and human drivers for the peaks (rush hour, weird routes).

That's why Waymo partnered with them in Austin and Atlanta. Waymo gets instant volume/utilization without having majority of idle depreciating assets (wait what Uber network actually has value???). Uber keeps the customer interface.

They aren't getting replaced. They're becoming a bigger/better aggregator.

Another extremely large (and largely ignored) plot-hole in AV's dominating $UBER to consider is climate. AV's have only proven to work in sunbelt states (ideal climate conditions). They are beginning to map out in harsher climate cities but places like the mid-west during the winter would likely never work for AV's in the near future.

My last thought is Avride entering Texas (partnering with Uber in both delivery and rideshare) is pretty much the last nail in the coffin for the thesis that AV's are killing Uber. Before when it was just TSLA and waymo in the market there could have been a chance of a duopoly squeezing Uber out. With Avride plugging into the Uber network along with other future OEM projects that will come online very soon it is very clear that the market WILL be fragmented for most use-cases. It doesn't matter if waymo is better at inter-city travel because a majority of use-cases all AV's will be a commodity. The fragmented market essentially takes the the AV issue out of the equation and makes Uber the dominant demand aggregator that it already is.

I tried to keep it simple for $UBER bears but prove me wrong that none of these hold. Please, I am a reasonable/logical person 🤣

English

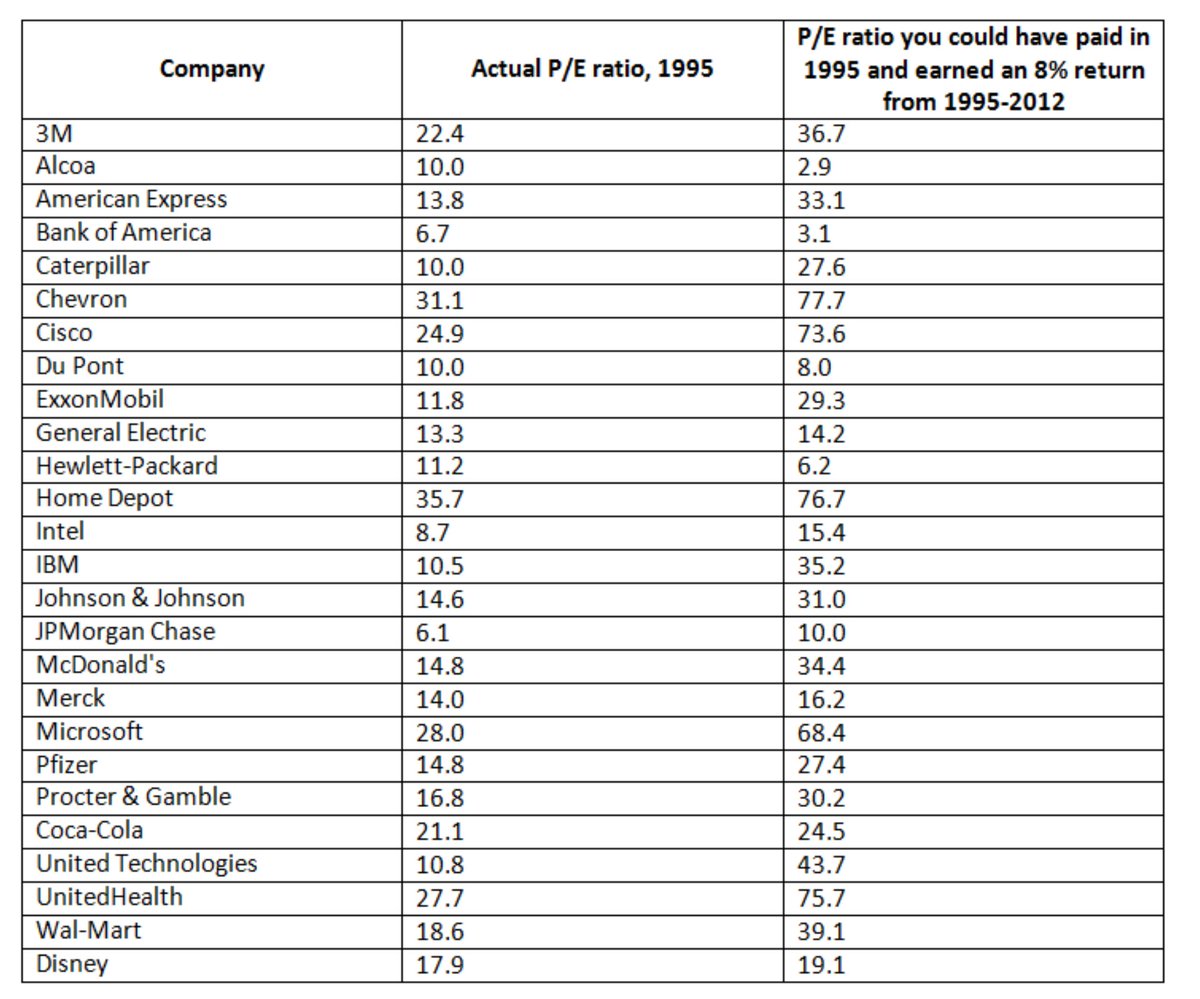

@ReneSellmann @morganhousel To be fair comparison need to show end of period P/E also

English

This chart by @morganhousel is a cheat code for humility: the right price for a great business is almost always higher than you think in the moment.

English