Angehefteter Tweet

PetePakCryptoⓣ

3.2K posts

@BMPCryptoExpert

$ETH $BTC $TEL $ETC $DFX $SOUL $MATIC $NAKA NFA-DYOR Tel Referral Code: 9f48d54f81e @Telcoin

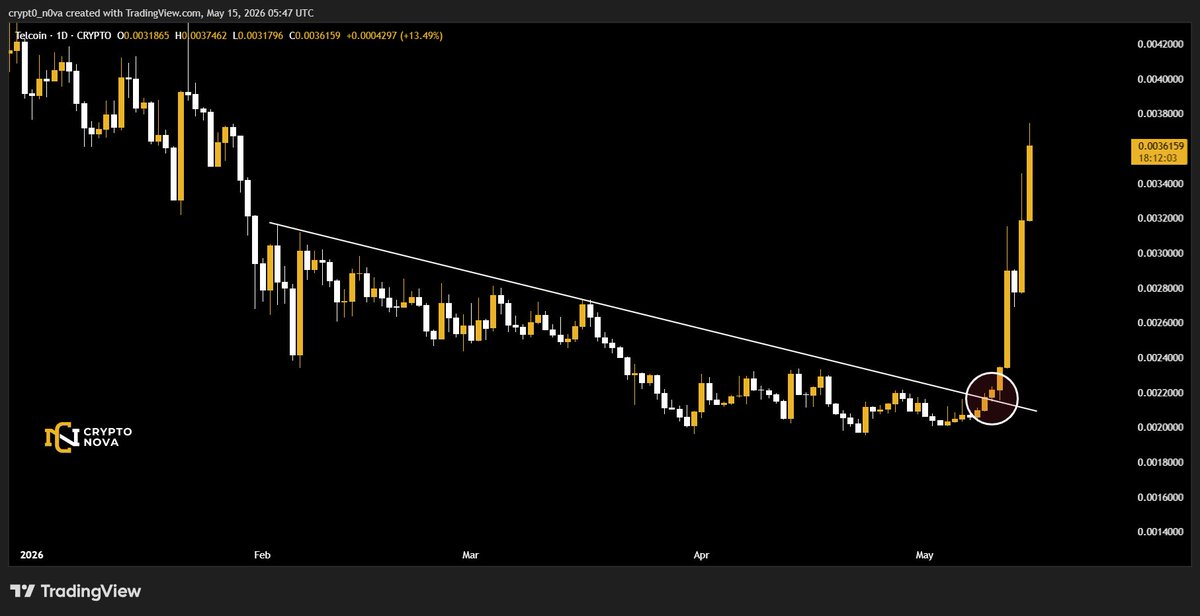

$TEL just had a 4 hour golden cross between the 100 and 200 moving averages. This is a strong bullish signal. Bouncing between well established old support and resistance levels. Break above $0.0032 to confirm the rally. Break down below $0.0025 to reject the rally. Imminent targets are $0.0038 and $0.0045 For long term targets see my pinned post. More detailed chart coming later this week. Trade, store, send money smarter with #Telcoin! Sign up, stake $TEL & refer users to earn fees! r.telco.in/iKouNrRsqVxY3W… Referral Code: cLUSbbjKi1V