Angehefteter Tweet

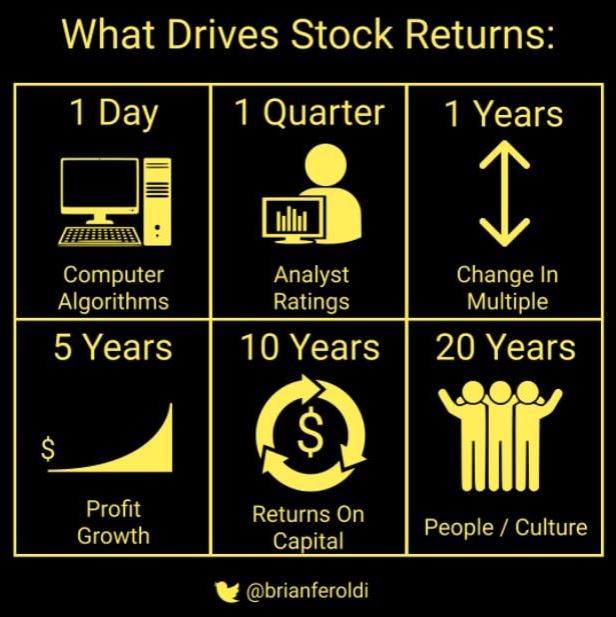

Take a moment to understand this.

Once you internalise this, your investment returns will follow suit.

$tsla $pltr

English

Chicken Little

19.1K posts

@Chicky_Think

Sharing my stream of consciousness as I learn to be a better investor, person and father with each passing day. Paying it forward.

From FY2022 AR $SMCI 🔸Key Points🔸 1)No other customers represented more than 10% of revenue 2)Working with leading processor vendor eg Intel ,Nvdia and AMD. 3)Believe to be only major server, storage and compute platform that design, develop and manufacture significant portion of the system in US. 4)58% of revenue from US, 21.9% from Asia 🔸Risk🔸 1)Competition from original design manufacturer (ODM) eg Foxconn which can scale and low cost production. These companies have longer operating histories and branding. ODM has previously supplied parts too. 2)Computer server industry has short lead time and quick delivery schedule. Coupled with global shortage in 2021/2, there is a need to shore up inventory. When the economy falters, the big inventory demands more storage cost. 3)Had a history of delay FS filing in 2017. Recorded liability of $17.5M with SEC. 4) The R&D as percentage of Sales is higher than most of competitors. 5)There are plans to target larger customers and sales, this implies ➡️Customer base will be more concentrated ➡️Cost of sales might increased ➡️Borrowing will increase ➡️Higher inventory risk 6)Vendor concentration risk Two companies for their work in contract design and management support and warehousing – Ablecom and Compuware. The management of these two companies are direct family members. In 2018, CEO Charles borrowed $12.9M from his sister-in-law. It was to pay off margin loans to financial institutional which the lenders called for in Oct 2018, with stock price suspension then. As of June 2022, CEO still owe $15.7M. The supply chain and company operation can be affected or held at hostage if the two vendors were to be acquired or change of management. 7)Supplier concentration risk - Two suppliers form 29% of total purchase in June 2022. 🔸Financials🔸 1) Income Statement Inventories at sky high at $1.5B with finished goods at $1B. Will have a big problem if unsold. Although current ratio is 1.9x but the bulk is from inventory at $1.5B. Remain interesting to see if the inventory will be sold off. 2)Balance Sheet Cash of $267M, short term debt $449M and long term debt at $147M. 3)Cashflow Borrowed $1.1B to pay debt of $650M. Negative cashflow form operating, largely contributed by high inventory ($519M) and receivables ($371M). To monitor whether the AR decreased in near future. 🔸Loan Repayment🔸 2023 $449M 2024 $36M 2025 $39M 2026 $39M 2027 $14M 2028 and beyond $16M 🔸Summary🔸 I don’t see any moat as is dependable of key vendors, competition can easily penetrate. Huge loan and debt to clear off. Not my cup of tea.