I saw the Dow Jones just passed 50,000 for the first time. Here's the chart of the Dow vs Gold rebased to zero from the day that Nixon closed the Gold window.

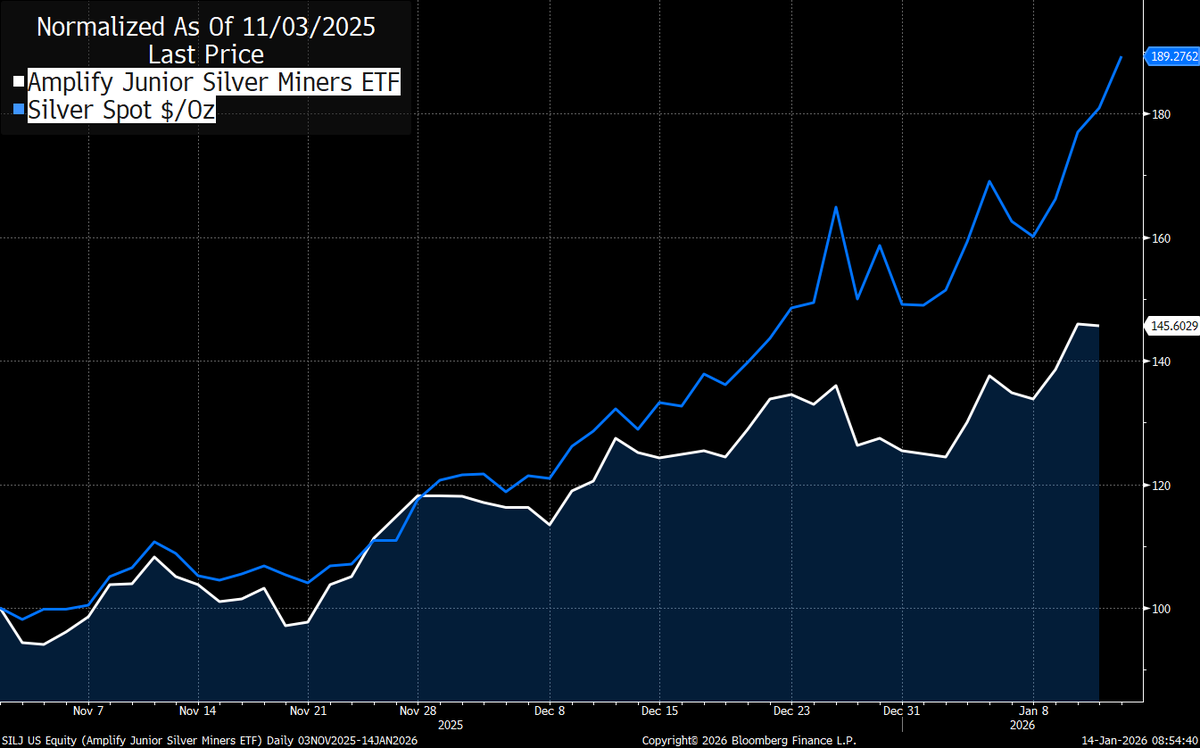

There's widespread scepticism in Western equity markets about the sustainability of recent moves in metals prices. Chinese investors on the other hand don't seem so cautious.

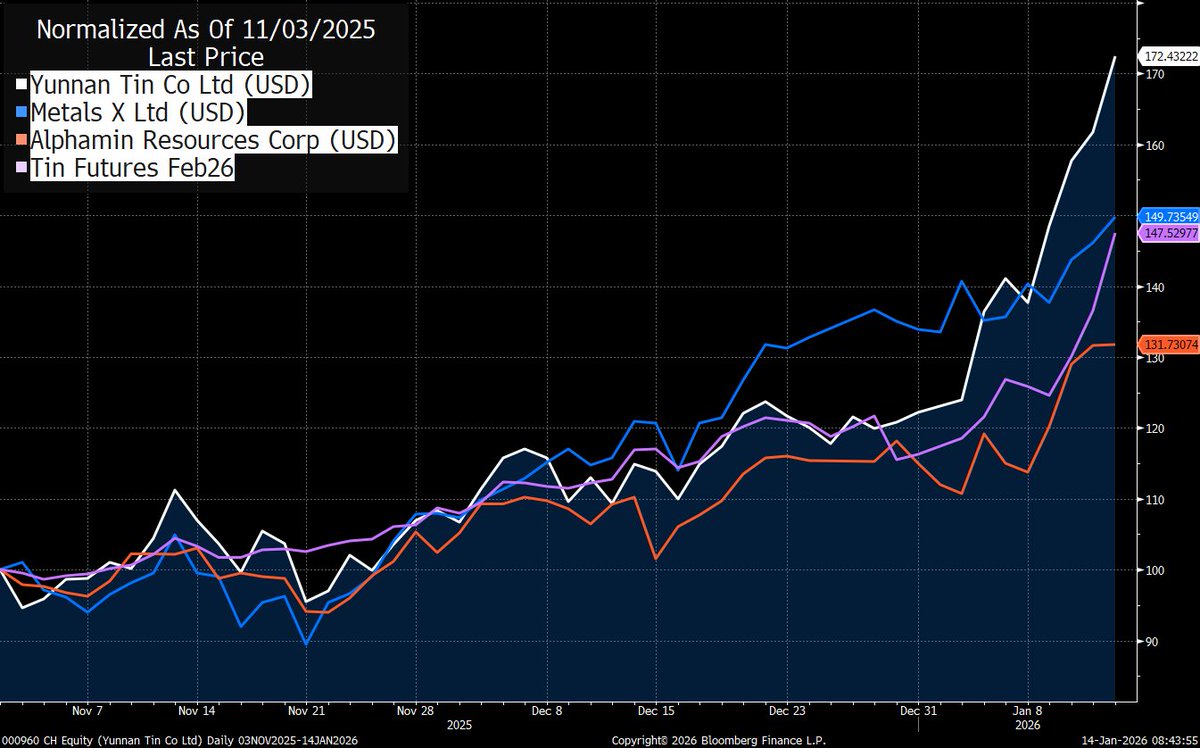

Chart shows the three producing tin stocks and Shanghai tin futures rebased to 0 as at 1st Nov.

Only Yunnan has provided any leverage to the tin price while AFM has undeperformed the metal badly.

Let's see who is right.

Western miners face a brutal reality: their cost of capital is up to 66% higher than peers in Asia. That gap is reshaping who gets to build the next generation of mines.

Imagine trying to finance a billion-dollar copper project while your competitors borrow at half your rate. The result? Asian industrial capital (Japan, Korea, China, Indonesia, Saudi etc.) is stepping in where Western markets can’t.

In this episode, veteran banker Michael Willoughby explains how a multipolar world of capital is changing the game:

• Why Western equity markets are structurally capped

• How Japanese trading houses and Middle Eastern funds are reshaping deals

• Why metals may become the new “store of value” for sovereign capital seeking inflation hedges

Listen now to hear how geopolitics, capital flows, and mining strategy intersect, and what it means for the next decade of resource investment.

YouTube 👉 youtu.be/h6JpJVmZjNc

Spotify 👉open.spotify.com/episode/3pPHD3…

@WVerily As @YellowLabLife points out in his reply above, it is a transfer of value from exisiting shareholders to new shareholders without the exisiting shareholders' consent.

$MAI Minera Alamos - it's not the deal in itself that is bad - Fiore is an ok asset, or the price paid - which seems reasonable, but the horribly dilutive terms of the deeply discounted financing + warrants. A company that had a good knowledge of its shareholders and good relationships with them would have been able to have a sensible discussion pre-deal and finance this with an at market-price issue. It's ironic that one of the distinguishing features of MAI in the past was the fantastic IR job that Doug @dougcan consistently did and the relationship he built with the shareholders. But he seems to have disappeared from the scene.