MicroCapDanmark

491 posts

Mark Leonard almost never speaks publicly. When he does, you listen.

In this clip he shows you the exact playbook AI agent companies will run against $CSU. His case study: Veeva.

Leonard was wargaming at all-time highs. Before anyone was worried.

This is not a man who got blindsided.

English

Populær investor: Aktie kan stige mindst 1000 pct. #Echobox=1773987044" target="_blank" rel="nofollow noopener">ekstrabladet.dk/penge/populaer…

Dansk

$ABX with a brutal takedown of a short and distort campaign

Abacus Global Management@AbacusGM

@KarstResearch posted a bear case on $ABX. Respectfully, the analysis has some material errors. Let's walk through it claim by claim using the actual 10-K. CLAIM: "No real cash generation — OCF negative $25.7mm" Under ASC 325-30, life settlement policy purchases flow through operating cash flows — not investing, unlike virtually every other asset-intensive business. The 10-K shows $49.2mm of net policy deployment embedded in OCF. That's deliberate capital deployment into income-generating assets, not operational burn. Adjusted EBITDA was $132.6mm on $235.2mm revenue — a 56% margin. And OCF improved $183mm year-over-year (from -$208.8mm to -$25.7mm). That directly contradicts the narrative of deteriorating cash dynamics. CLAIM: "135% of EPS is unrealized gain — EPS is vapor" The far more important number is realized gains on policies actually sold: $178.6mm in 2025. The unrealized gains ($49.3mm) are marked using a 13% discount rate calibrated directly to actual historical transaction prices — not a theoretical actuarial assumption. Weighted average realized gain on policies sold rose from 24.9% in 2024 to 32.5% in 2025 — the portfolio outperforms the model. Grant Thornton verified fair value and reviewed lookback analysis comparing prior valuations to actual sale prices. This is grounded in 1,000+ real transactions, not vapor. CLAIM: "86 cents of debt per dollar of policy assets" This ratio is intentionally narrow — it measures only policy assets against all debt, ignoring $38mm cash, $18mm AR, $21.5mm management fee receivables, and the acquired businesses generating real revenue. Carlisle alone generated $26.4mm in recurring management fees on $2.4B of longevity fund AUM. FCF Advisors manages $850mm in ETFs. These are durable, fee-generating platforms — not inert paper assets. You can't strip them out and call the balance sheet levered. CLAIM: "TBV per share = $0.42" The standard TBV calculation starts from total stockholders' equity — which already nets all assets against all liabilities — and subtracts intangibles: Equity: $418.5mm Less goodwill: ($252.8mm) Less intangibles: ($66.4mm) TBV = $99.4mm → $1.02/share Karst got $0.42 by starting from non-current assets only and subtracting selectively — omitting $38mm of cash and other current assets while including all liabilities. That's not how TBV works. The goodwill represents Carlisle, FCF, NIB, and AccuQuote — all revenue-generating, all passed impairment testing, all independently reviewed by Grant Thornton.

English

While $RMS is one of the best companies in the world, right now is just a better time to find beaten down tech stocks :)

MicroCapDanmark@MicroCapDanmark

@CCM_Brett Because right now there is a lot of good deals, while Hermes is only relative "cheap" to where it has been. If it was 6 months back i could justify it. Also we pay taxes here 🤣, lets use the P/E

English

@CCM_Brett Because right now there is a lot of good deals, while Hermes is only relative "cheap" to where it has been. If it was 6 months back i could justify it.

Also we pay taxes here 🤣, lets use the P/E

English

Why are we not buying Hermes here?

Chit Chat Stocks@chitchatstocks

Hermes now trades at an EV/EBITDA of 23 Why does the stock not work from here?

English

40g of protein? yeah these are protein bars if you think about it

English

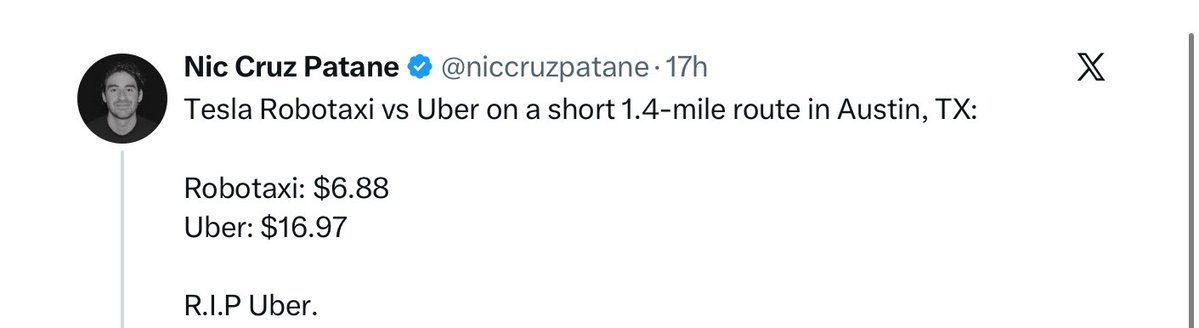

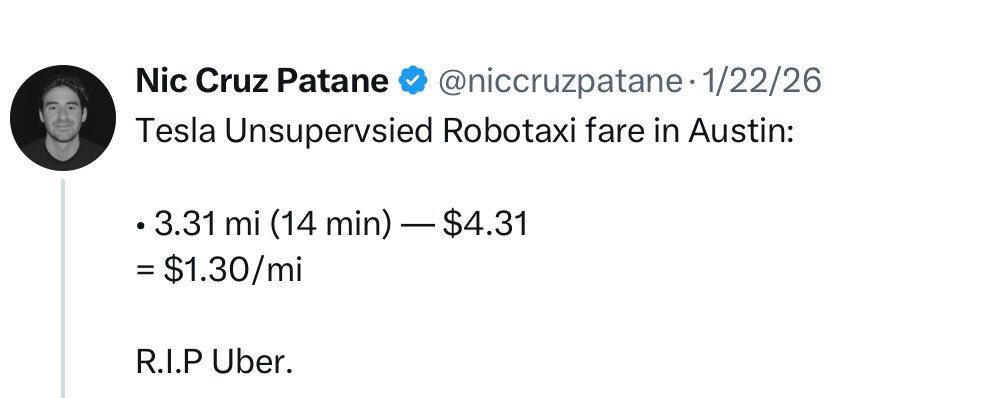

@CashFlowKingsYT Omg dident you see Elongs new $TSLA prediction? FSD next year! $uber will not survive this!

English

It’s incredible how this $TSLA shill can continue to put out the same tweet trying to damage $UBER reputation and sentiment.

Not only are you glazing Elon, but you’re re using and recycling the SAME tweet.

Average Tesla investor who has no morals, no brains, and no logic.

English

@wealthmatica @stknbd_thomas We should have a MEME for people who just take a TTM P/E without any context and calls it cheap.

@stknbd_thomas You need to look at operating leverage, Margin expansion and what the future earnings could be. Analyst thinks we have a forward P/E on 13.

English

@stknbd_thomas $ZETA is not priced for perfection right now?

English

40% growth catches the eye. But margins only just broke even. Priced for perfection.

Wealthmatica@wealthmatica

I don’t know what else to tell you… $ZETA is an insane opportunity. Buy the stock or not, I don’t care. I talk about it daily – probably piss most of you off, but I can’t help myself. It’s my most studied investment. Period. I have absolute confidence, that in 10 years I’ll look back and this will be the investment that made me a millionaire. If not… I’ll take that on the chin. $ZETA

English

@DrewCohenMoney @Matkinvest Kommer en Palantir om lidt...

Dansk

🚨Vote on the next deep dive and content schedule:

We will be releasing Palantir tomorrow morning (8am PSD)

FICO is coming next Wesnesday!

Vote for the following Saturday:

Comment other tickers to get in future votes.

English

@DrewCohenMoney You have such a good taste Drew :P ! Having a feeling we own a lot of the same company.

Anyways, voted Reddit. Bought last week :) !

English

@Matkinvest @chitchatstocks We cant buy it on @NordnetDK @Nordnet same with a lot of other exchanges and airports

English

@wealthmatica @earthscitizen17 @Sam_Badawi @dsteinberg10000 So in short it creates shareholder value because executives turn up to watch Kevin Hart and they $zeta is the ads here? If yes it will provide shareholder value, i thought it would be like a fireside chat with Kevin about zeta or something like that...

English

For new shareholders this may seem ridiculously odd to you, I get it… this was me last year when they booked Tom Brady.

However, the outcome of $ZETA live 2025 was millions and million in revenue generating opportunities.

Which I did not anticipate.

Turns out, executives want the opportunity to just see headliners, while $ZETA uses the opportunity to cross-demo their products.

English

@earthscitizen17 @Sam_Badawi 100% agree, as someone who is buying shares at the moment this is a red flag. Why does hiring Kevin Hart create long term shareholder value and what does he know about the industry?

@wealthmatica @dsteinberg10000

English

@Ashton_1nvests The crazy part is on a EV/S $ttd is STILL more expensive than $zeta

Can we please give $zeta the $ttd premium ;) ?

English

I love $ZETA and charts like this are exactly why.

Look at revenue growth vs $TTD:

2021

ZETA: ~24%

TTD: ~43%

Fast forward to today…

2025

ZETA: ~30%

TTD: ~18%

$ZETA is accelerating while $TTD is slowing.

That matters.

To me, this is what early-stage winners look like:

• Taking share

• Scaling fast

• Still under the radar

And the best part?

The market still doesn’t price them the same.

That’s where the opportunity is.

$ZETA is a high conviction long-term holding for me.

English

@KonradJaku11615 @dsteinberg10000 @ZetaGlobal @KevinHart4real $zeta more of a WHY? Why not a industry expert, honestly this is often mentioned as a red flag...

English

GIF

English

Athena made one thing clear: we’re leveling up this year. @ZetaGlobal

Zeta Live 2026 returns October 8 with @KevinHart4real headlining at one of NYC’s most iconic venues.

LG 🚀🚀🚀 $ZETA

businesswire.com/news/home/2026…

English

@QualityInvest5 How dare they make long-term decisions when Wall Street wants to be fed every quarter.

English

@QualityInvest5 Snap CEO have burned 12 billion $ the past 10 years building a 8 billion $ company that runs on shares and is full controlled by a CEO who dont care about minority shareholders.

I dislike both by the way ;)

English

I have a video coming out in about an hour

I will NEVER touch anything that has the name Jack Dorsey on it 🤣

$XYZ

Rohan Paul@rohanpaul_ai

Jack Dorsey’s Block quietly rehires few from 4,000 fired staff according to LinkedIn posts.

English

@wealthmatica s it’s a fairly complicated company at first glance, and I’ve had some bad experiences with ad-related companies, your explanation really helped me. I had looked at it a couple of times over the past year and put it in the “too hard” pile before buying in the last couple of weeks

English

I don’t know what else to tell you…

$ZETA is an insane opportunity.

Buy the stock or not, I don’t care.

I talk about it daily – probably piss most of you off, but I can’t help myself.

It’s my most studied investment. Period.

I have absolute confidence, that in 10 years I’ll look back and this will be the investment that made me a millionaire.

If not…

I’ll take that on the chin.

$ZETA

Wealthmatica@wealthmatica

I like to buy "LEGACY disruptors". Traditional workflow SaaS is dying, and AI-Native infrastructure is taking the crown. Here are 7 legacy killers eating their lunch... 1) Zeta Global: $ZETA Legacy players challenged: Adobe, Salesforce, Oracle, TTD → Marketing/Ad Technology. → First-party data MOAT. → Growing 40% YoY

English