Angehefteter Tweet

Robin

3.3K posts

Robin

@Robin54573990

Growth investor, undervalued AI stocks Europe without USA hype, early Bitcoin investor and OG (2017), energy investor, smallcap finder before x talks about it

Frankfurt on the Main, Germany Beigetreten Aralık 2019

9 Folgt331 Follower

Robin retweetet

I’m beginning to think that $NRGV is a better investment for the BESS space than $EOSE purely based on valuation.

The price to sales for NRGV is 3.4 compared to 17 for EOSE. Eose has more cash but more debt as well comparatively.

Technology-wise, NRGV focuses on a diversified tech mix (gravity-based G-Vault for long-duration, electrochemical B-Vault, and hydrogen/hybrid H-Vault) plus AI-driven software (Vault-OS, etc.). EOSE specializes in proprietary zinc-based (Znyth) batteries as a lower-cost, non-lithium alternative for 3–12 hour discharge applications, with supporting software and services. NRGV is predominantly in Utilities-Renewable; EOSE is predominantly in Industrials-Electrical Equipment.

No position in either for now and I traded EOSE through options and made some $ all through last year. It probably comes down to if you’re bullish on EOSE’s Zinc tech’s differentiation.

English

$CRWV $IREN

Both good looking setups

Only have position in coreweave 👍

English

Robin retweetet

@Ren_aramb Solid breakdown. I’d add $XFAB to that 800V watchlist. As the lead foundry for GaN/SiC, they own the capacity that $NVTS and $AOSL rely on. You can't have an infra rebuild without the fab space. Power is the new bottleneck.

English

First place that money goes to is the leading stocks...

BUT

In a hot market... it starts to find its way into lagging sectors and stocks

Any little bit of momentum can ignite a new theme and these stocks start to play "catch up"

You will see this happen in the next few days.

English

@moninvestor Thanks for your mention. I will post more about my opinions in the future 🤭👋👋

English

Robin retweetet

Bought a new stock today: $NRGV.

An under-the-radar energy storage name I’ve just started researching.

At a simple level, Energy Vault stores electricity when there is excess supply and releases it when demand increases. This is critical because renewable energy sources like solar and wind are intermittent, and storage is what makes them usable at scale.

What makes this more interesting is the company’s shift toward owning and operating energy assets, which introduces recurring revenue instead of one-off project income.

Historically, Energy Vault generated lumpy, project-based revenue. It is now transitioning toward more predictable cash flows through its “Asset Vault” strategy, where it builds, owns, and operates storage assets rather than just delivering them.

Revenue reached about $203M in 2025, up over 340% year-over-year, and the company delivered its first positive EBITDA quarter in Q4.

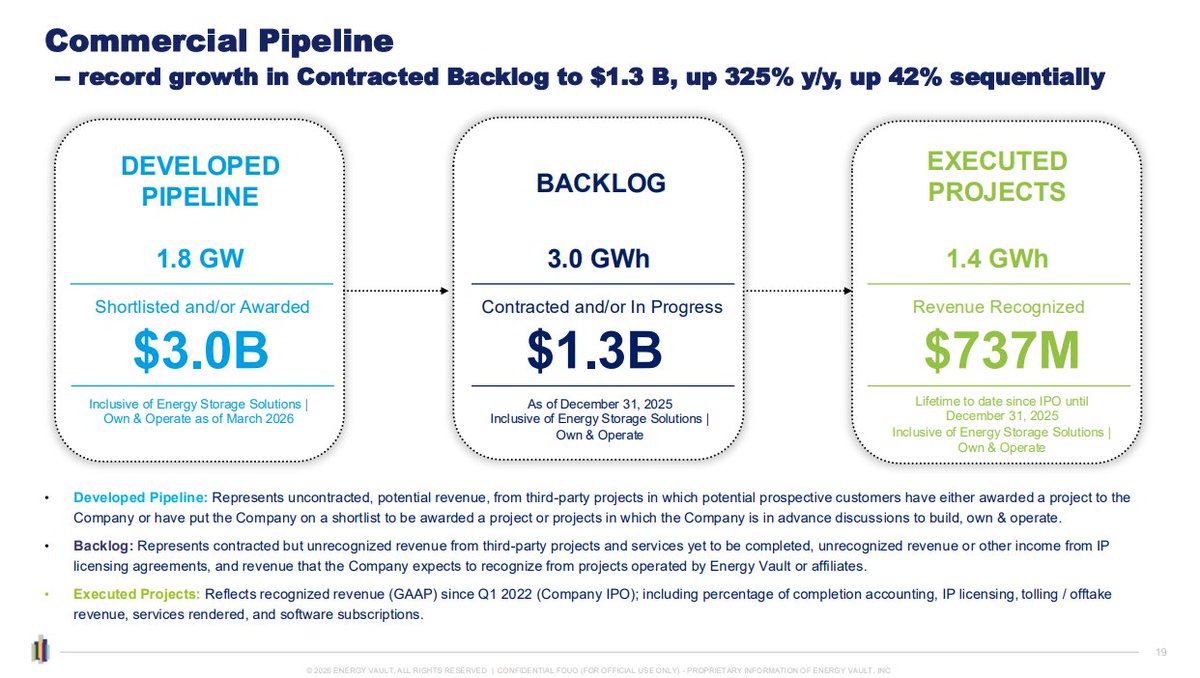

The key driver behind that inflection is the backlog, which has expanded to roughly $1.3B, up over 300% year-over-year.

A major catalyst is its partnership with Crusoe Energy Systems. Energy Vault is now building power infrastructure for AI data centers. These deployments are expected to generate 10–20x higher EBITDA per MW compared to traditional storage projects.

AI data centers are increasingly power constrained. If Energy Vault can successfully serve that demand, it shifts into a higher-value infrastructure player directly exposed to AI-driven energy demand.

On top of that, the company is working on next-generation storage through sodium-ion battery partnerships, which could reduce costs and lower supply chain risk over time.

The balance sheet has also strengthened, with cash above $100M, providing runway to execute on this transition.

Putting it together, the bull case is straightforward.

This is a company that has already proven it can scale revenue, is turning profitable, and has a large and growing backlog. At the same time, it is moving into higher-value markets like AI infrastructure, where the economics are significantly more attractive.

The key risk remains execution. The company needs to convert backlog into cash flow and scale its asset ownership model without funding stress.

If that works, it shifts from a small speculative energy stock to an infrastructure platform exposed to two large structural trends: renewable energy buildout and AI-driven power demand.

Not financial advice. I’ve just started researching and this is my first purchase.

Market cap: $770M

Thanks to @Robin54573990 for bringing this ticker to my attention.

English

Robin retweetet

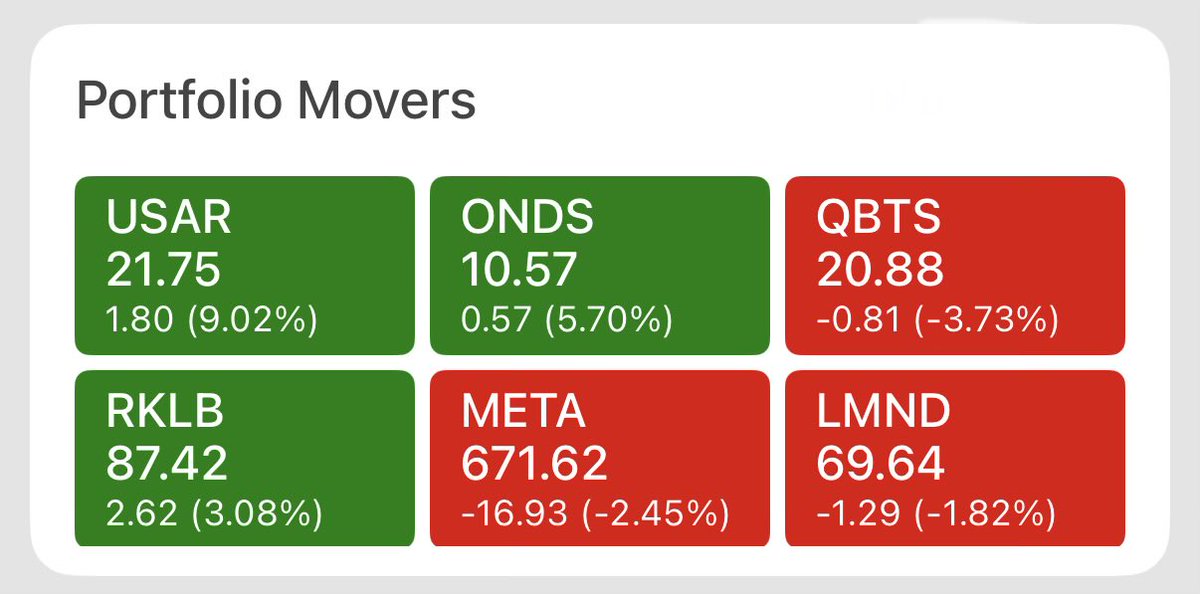

$USAR +71% in 3 weeks now 🤫

Sniped the entry here. My other entry from the same day is doing well too but not like this. Maybe I’ll announce that one soon 😆

Dr J Rould@jrouldz

I think this is an appropriate time to announce publicly one of my new entries in the long term portfolio Entered $USAR at end of March (near market lows) with average under $15 🔥 Posted all my research and trade setups in advance in the sub as always 😁

English

Robin retweetet

Robin retweetet

English

Robin retweetet

@yarvin_stoltz $NRGV jetzt noch unbekannt aber in ein paar Wochen werden viele darüber sprechen 🤭

Deutsch

Robin retweetet

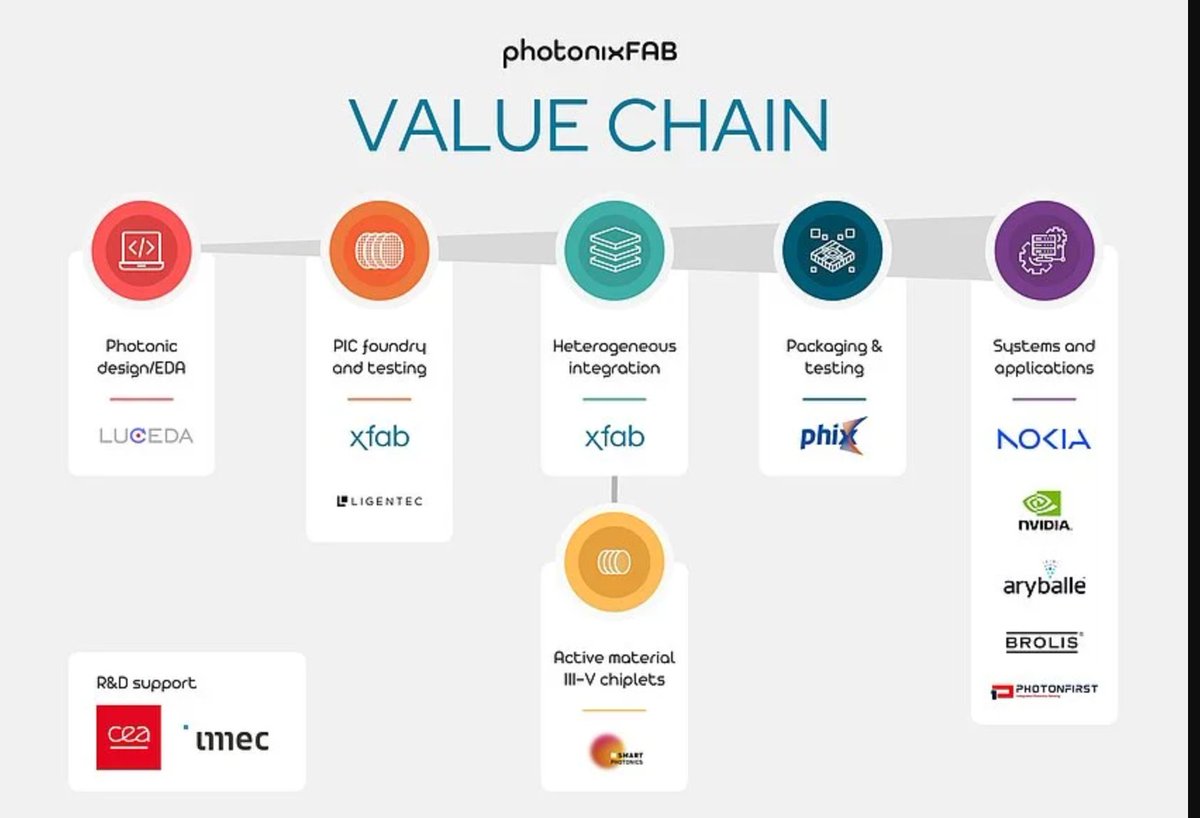

The "Specialty Foundry" Play: Is $XFAB Following the $TSEM Blueprint?

Scanning the European Photonics supply chain for deep-value plays, X-FAB $XFAB stood out last week.

While the market still labels them as a legacy automotive supplier, their operational roadmap suggests they are aspiring to become the European equivalent of Tower Semiconductor $TSEM.

X-FAB is essentially the "younger brother" in the specialty foundry space - smaller in market cap, but aggressive in its technological pivot.

1⃣The US Connection:

It’s no longer a secret - NVIDIA is officially integrated into the $XFAB ecosystem via the photonixFAB consortium.

They are using X-FAB’s SOI platform to tape out layouts for next-gen AI optical switches and transceivers.

2⃣The Technology Leap:

In Jan 2026, X-FAB scaled Thin-Film Lithium Niobate (TFLN) on 200mm wafers. TFLN is the physical enabler for 1.6T connectivity.

By combining this with Micro-Transfer-Printing (MTP), X-FAB is solving the "on-chip light source" problem that has bottlenecked AI clusters.

3⃣Beyond Automotive:

While the market labels them a "car chip maker," X-FAB just finished a $1B CapEx cycle to pivot towards high-margin Specialty Tech.

Their Microsystems segment (SiPh/MEMS) recently crossed the $100M revenue mark, signaling a massive shift in product mix.

4⃣Comparison to TSEM:

Like Tower, X-FAB leverages fully depreciated assets to run specialized processes.

However, X-FAB’s lead in Silicon Nitride (SiN) and Heterogeneous Integration gives them a distinct advantage in the EU's sovereign AI supply chain.

5⃣The $IQE/LIGENTEC Synergy:

By integrating IQE’s epitaxial wafers and Ligentec’s SiN designs, X-FAB provides a turnkey "Foundry-as-a-Service" for the optical era.

Bottom Line:

$XFAB is trading at a discount to legacy foundries, yet it sits at the epicenter of the optical roadmap in Europe.

Pep Invest@PepInvestStocks

$XFAB Key edge: Strategic partnership with $IQE on GaN power devices (650V+ platform for automotive, data centers & consumer). This creates a European supply chain for next-gen power electronics - huge for de-risking and scaling in a geopolitically sensitive world.

English