Angehefteter Tweet

This "every big trade is insider trading" narrative is everywhere. You’ve got a conspiracy hammer, so everything looks like an insider nail.

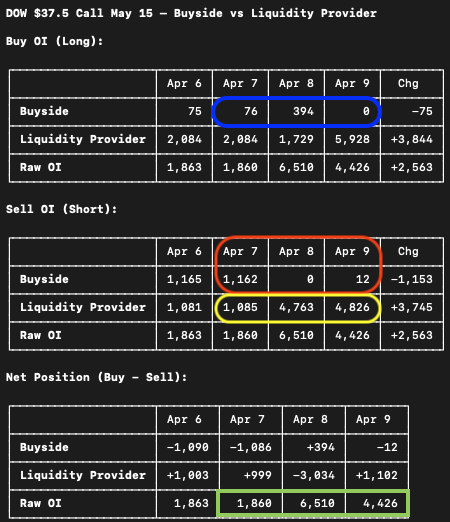

Take this DOW May 37.5 Call that blew up on April 8th. Someone claims “they” bought 5k contracts, stock bounced, and “they” made 80%. Classic robber baron story, right?

Not quite.

A huge chunk of options volume isn’t buyside (retail or hedge funds) piling in. It’s liquidity providers (banks, market makers) trading against themselves or facilitating flow.

Here’s what actually happened with the DOW $37.5 May calls (see table):

Open interest jumped from ~1,860 on Apr 7 to 6,510 on Apr 8 → yes, ~+5k contracts traded.

Then it dropped to 4,426 on Apr 9. If this was some genius insider long who “knew” the bounce… why didn’t OI collapse when they supposedly cashed out?

Also… why ignore the ~10k flow in the May 42.5 calls or the 8k in April 40 calls that printed around the same time? More insiders throwing us off the scent? Or maybe it was just a spread.

Back to the 37.5s:

Our data shows buyside (customers) went into Apr 8 SHORT ~1,000 of these calls. By close, they were net +394.

So it looks like someone covered their ~1k short (makes sense — stock was down ~10%, short calls were getting crushed), and buyside ended up modestly long ~400.

That explains ~1,500 of the 5k. What about the other ~3,500?

Liquidity providers stepped in. Some bought, some sold. They’re the ones carrying a big chunk of that open interest now — not some singular “they” with inside info.

Not every large print is a shadowy cabal front-running the market. Sometimes it’s just market makers doing their job, providing liquidity, and hedging.

The insider trading obsession ignores how options actually work.

unusual_whales@unusual_whales

English