🚨A High Octane Set Up #ATERIAN #ATN

To Private Investors and LONGS:

You have watched your company deliver asset after asset, partnership after partnership, and milestone after milestone. And yet, the share price sits at a paltry 29p, obscenely disconnected from the fundamentals.

You have asked yourself: What am I missing?

The answer is nothing. You were never the problem.

For months, a silent, mechanical seller has been pressing the bid. Not a short seller. Not a bear. Not someone who understood the business. Just a highly efficient, highly rational machine, executing a trade.

That machine has now run out of shares.

And the management team — the very people who know the value of every license, every joint venture, and every pound of tantalum — are now openly discussing buying the whole company out from under everyone else.

This is the story of how the overhang died, how the warrants became a tailwind, and why the next few weeks could be the most consequential in Aterian's history.

1️⃣ PART ONE: THE PHANTOM IN THE REGISTER

Let’s go back to 31 December 2025.

At that time, Aterian had 16,684,000 shares in issue. The register was clean, tight, and committed. Altus owned 14.46%. Charles Bray owned 8.16%. Summerhill owned 7.97%. Dowgate owned 6.63%. These were not flippers. These were bedrock holders.

Then came 19 February 2026.

The company announced a placing: 1,000,000 new shares at 25p, plus 500,000 free warrants with a strike price of 32.5p.

The participants? A group of sophisticated retail investors operating under the Hargreaves Lansdown umbrella. They are not evil. They are not stupid. They are simply playing a different game.

Their game is this:

✅ Buy the placing at a discount.

✅ Receive free warrants.

✅ Sell the shares into the market ASAP.

✅ Keep the warrants as a free lottery ticket.

✅ Repeat with the next deal.

Yes, they are capital recyclers.

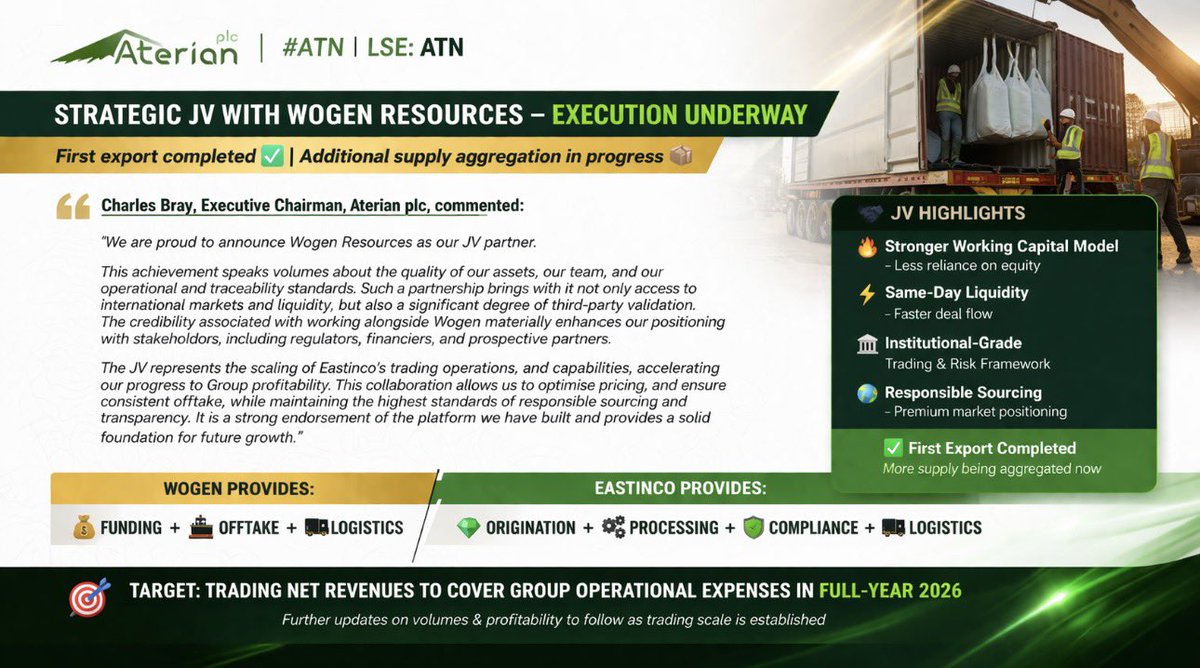

They are not long-term believers. And they do not care about Rio Tinto's sunk costs, or the Tantalum trading JV with the billion-dollar WOGEN, or the £26.1M sum-of-the-parts valuation attributable to the company.

All they care about is one thing: turning over their £250,000 as fast as possible. Period.

And so, beginning on 23 February 2026, they began to sell.

2️⃣ PART TWO: THE DREADED FIVE WEEKS

For five weeks, from 23 February to 01 April 2026, those 1,000,000 shares trickled into the market.

At ~40,000 shares per day, it was barely noticeable in isolation. But it was enough to cap every rally, absorb every bid, and convince the algo-trader that something was wrong.

It was not wrong. It was just a pipeline.

And then, on or around 01 April 2026, the pipeline ran dry.

Let’s be clear about what that means.

As of today, 09 April 2026, the Hargreaves Lansdown group holds a negligible amount of shares, if any, in Aterian PLC. I know. I’ve done the math. I’ve totalled-up the weekly block sales since February and it all adds up. HL are out.

Of course, you'll still have sellers in a normal functioning market, and which is key to any price appreciation. But overall, the big seller is gone.

3️⃣ PART THREE: THE SILENT BULL IN THE ROOM

But here’s where the story becomes truly elegant.

HL still hold 500,000 warrants.

Each warrant gives them the right to buy a share at 32.5p at any time before 15 February 2028.

They paid nothing for these warrants.

If the share price stays at 29p, the warrants are worthless.

If the share price rises above 32.5p, they become valuable. And if the share price reaches 50p for three consecutive days, the company can force them to exercise.

Do you see what has happened?

The very people who were selling shares are now incentivised to see the share price rise.

They have gone from being a headwind to a tailwind.

4️⃣ PART FOUR: THE MBO

Now we come to the most bullish element of all.

The Executive Chairman has publicly stated that the management team, represented by Summerhill Trust, is contemplating a management buyout should the company’s obscene undervaluation persist.

Let that sink in for a moment.

The people who run the company, who oversee every balance sheet, every license, every conversation with Rio Tinto and WOGEN, believe the market is so wrong that they are considering buying the entire business themselves.

This is not a marketing gimmick. This is not a ploy to support the share price. This is the ultimate insider signal.

And here’s how it would work:

Summerhill Trust and Charles Bray (already holding 15.21% combined) would partner with specialist private equity or debt financier.

They would make a cash offer to all shareholders.

To take the company private, they would need 75% acceptance.

At 29p, the entire company costs just £5.13 million.

At a realistic offer of 45p-55p, the cost rises to £7.9 million – £9.7 million.

But here's the kicker: the company’s SOTP valuation is £26.1 million, or 148p per share.

Even at 55p, they would be buying the company for a fraction of what they believe it's worth.

That's not a buyout. That's a heist.

And they are considering it because they know what you know: the market has made a catastrophic error.

5️⃣ PART FIVE: THE ASSETS

Let’s remind ourselves why 29p is absurd.

✅ Lithosquare licenses (8 licenses, 20% sold for €1.4M) → £6.1M

✅ HCK Project (Rio Tinto spent US$5M proving it up) → £2.0M

✅ Agdas copper-silver project (fully permitted) → £1.0M

✅ Tantalum trading JV with WOGEN (target £1M net profit in 2027) → £12.0M (12x PE, adjusted following Q1 2026 trading update)

✅ Remaining exploration acreage (Rwanda, Botswana, Morocco) circled by Tier-1 operators → £5.0M

👉 Total Fair Value → £26.1M (148p per share)

At 29p, the market says: All of that is worth £5.13 million.

That is a 5x upside just to reach a conservative, tangible, third-party-validated valuation.

6️⃣PART SIX: WHERE WE STAND TODAY

Let me lay out the current landscape as clearly as I can:

✅ HL placing shares → Fully exited

✅ HL warrants → 500,000 held → now a bullish incentive above 32.5p and a likely selling point at the 50p — 55p mark.

✅ Management alignment → 15.21% → and considering an MBO

✅ Market cap → £5.13M → a fraction of fair value

✅ Fair value (sum-of-the-parts) → £26.1M → 148p per share

✅ Upside to fair value → 5x

A FINAL WORD TO THE LONGS

You've held through the five weeks of relentless selling.

You've watched the share price refuse to reflect the obvious value.

But that phase is over.

The machine has run out of shares.

The warrants have flipped the incentive. And the management team, the people who know best, are openly discussing taking the company private because they believe the market is wrong.

They are right.

The market is wrong.

And when the market realises that the overhang is gone, the MBO is real, and the SOTP valuation is not speculation but arithmetic, you’ll need to buckle up, for what lies before you is a high octane set up.

English