May’s market performance was more challenging, with inflation rising to ~3.7% and the cedi posting its sharpest monthly depreciation.

Despite this, external debt stayed resilient. Overall, May was marked by rising pressures alongside resilience across selected asset classes.

The market closed lower as four decliners outweighed gains in KASA and CAL, with KASA leading the gainers after rising ~9.7% to GHS 1.59.

Despite the decline, strong demand for KASA, IIL and ETI kept the market in net bid territory at the close.

The market closed higher today, supported by gains in KASA, FAB and ETI while RBGH posted the steepest decline of the session.

Intense buying interest in KASA , AADS and CAL ultimately led the market to close in a net bid position.

🚨 New Stock Alert 🚨

SpaceX is now available on the Black Star App!

With the click of a button, you can own a piece of the company pushing the boundaries of technology, space exploration and the future of humanity.

Download the Black Star App today!

#BlackStar#SpaceX@elonmusk

As T-bill yields compress, Ghana's private sector credit growth has rebounded from -7.5% to 28.7% since late 2023 as banks are increasingly willing to lend.

For investors, the acceleration signals improving business confidence and a more supportive outlook for economic activity

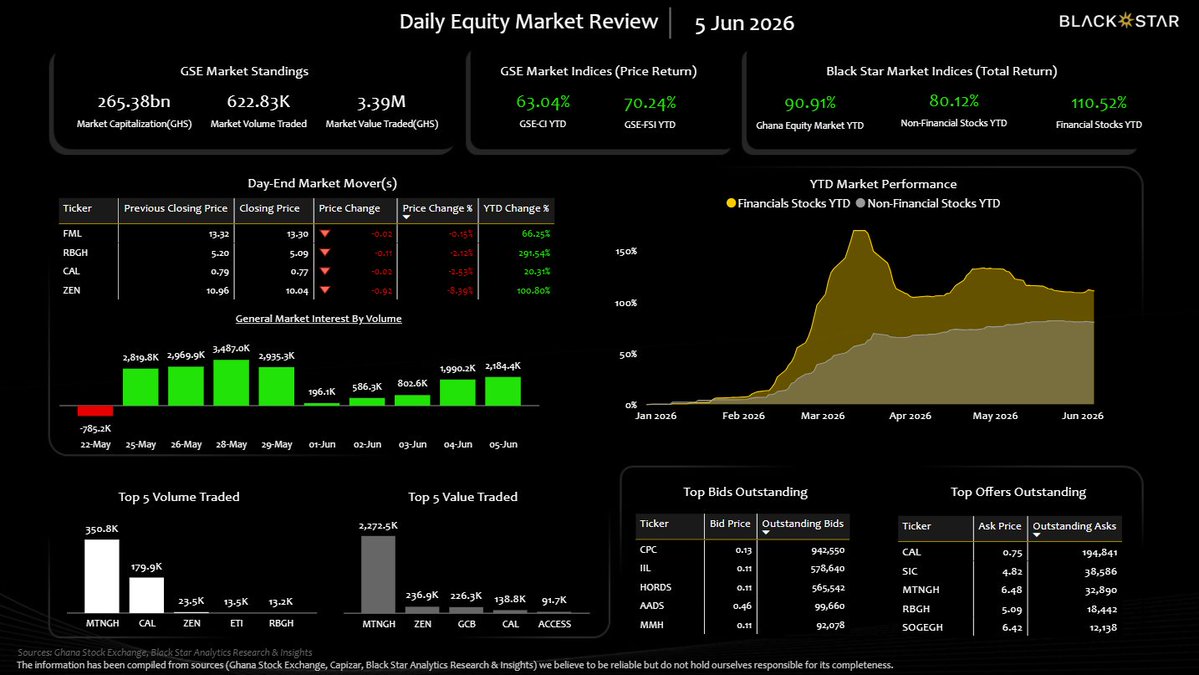

The GSE-CI recorded a second straight gain as six gainers led by TOTAL, CLYD and ETI outweighed four laggards.

Strong demand for CPC, DIGICUT and HORDS led the market to close net bid. Trading activity strengthened further, with volume and value both rising from the previous day

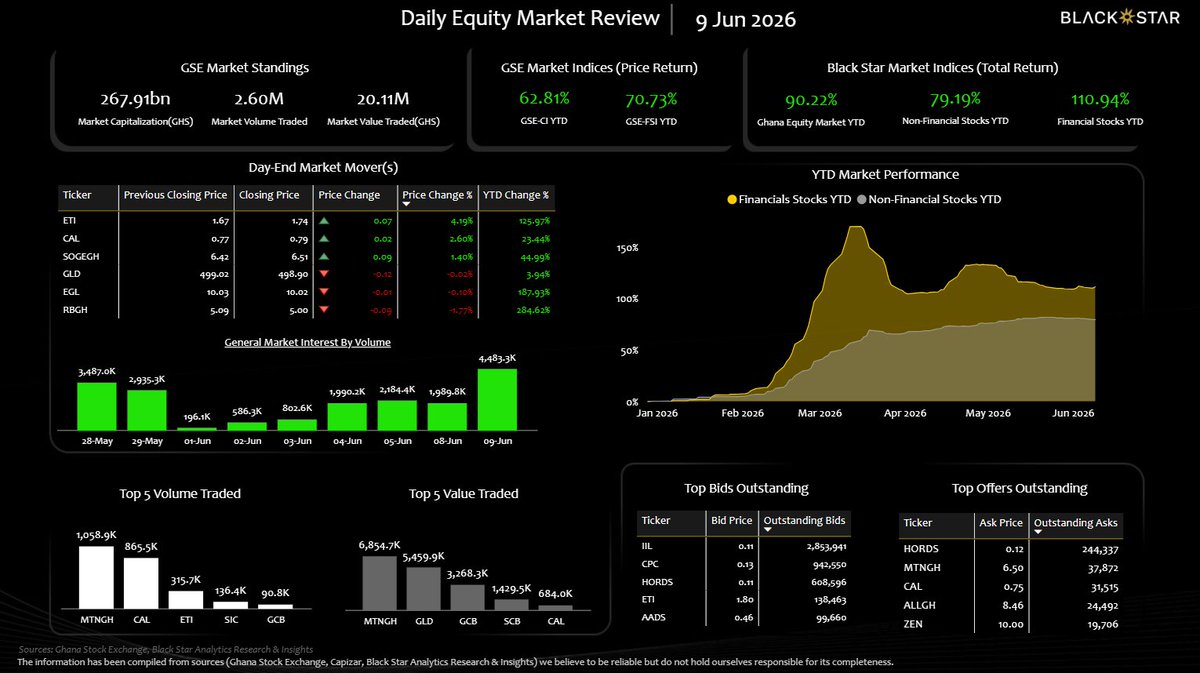

The GSE-CI edged higher from the previous session at today's close, supported by gains in ETI, CAL and SOGEGH despite three laggards.

Trading ended net bid, with ILL leading bid interest. Volume and value also improved.

The market remained under pressure as six decliners outweighed ETI's ~6.4% gain pulling the GSE-CI down by 0.46%.

Despite the continued weakness, sizeable bids in CPC, DIGICUT kept the market in a net bid position at the close.

The market closed lower as all price movers posted losses, marking the second consecutive Friday in which all movers ended in negative territory.

Nevertheless, persistent bidding interest in CPC and ILL kept the market in a net bid position at the close.

The market closed lower today as eight stocks declined, led by ZEN and EGH, outweighing gains in ETI and ALLGH.

Despite the downturn, sustained buying interest in CPC and DIGICUT kept the market in a net bid position at the close.

Market closed with ZEN falling ~2.8% as investors took profits following its strong year-to-date performance.

Despite the pullback, gains in ETI, CAL and GCB supported the market, while demand for CPC and CLYD kept it net bid.

Ghana's headline inflation edged higher to ~3.7% in May, marking a second consecutive monthly increase as price pressures became more broad-based.

The MPC’s decision to hold the Policy Rate at ~14.0% is likely to be tested by May’s inflation outcome.