azoroso retweetet

🎯 An agentic AI that writes its own factor signals -> and backtests them?

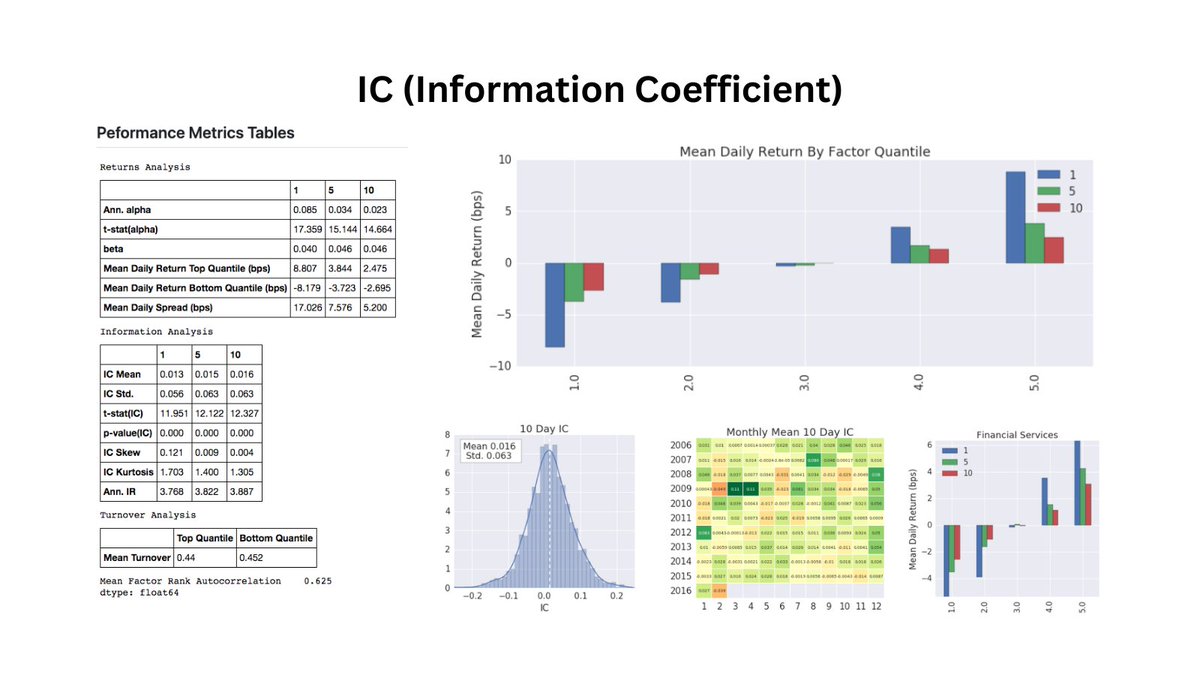

A paper that came across my radar at Noax this week: Huang and Fan build a fully autonomous framework for systematic factor investing using agentic AI. No manual prompting at each step: the system formulates signals, validates them out-of-sample, and applies economic-rationality filters on its own.

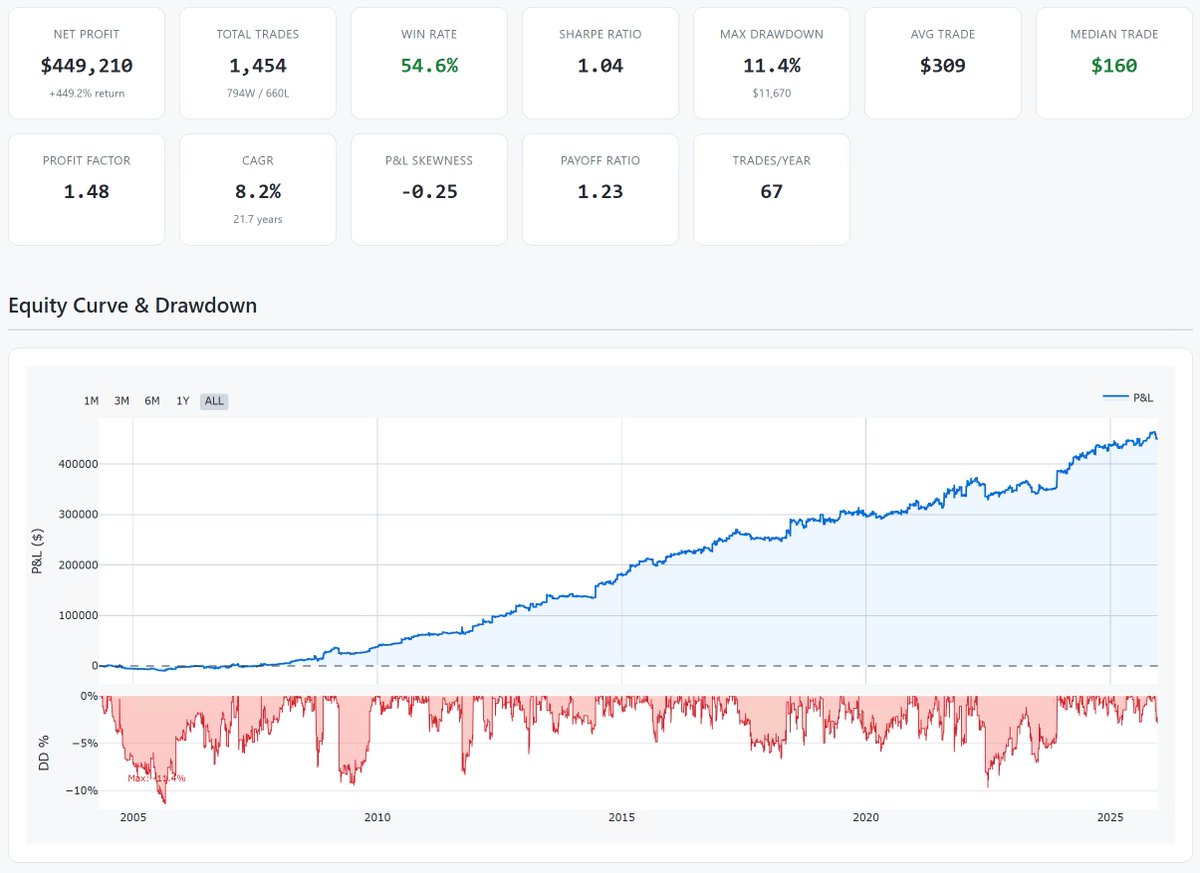

The results it reports: annualized Sharpe of 3.11 and returns of 59.53% on US equities.

My read: those numbers are almost certainly not replicable in a live setting. The gap between backtest Sharpe and real-world Sharpe is especially wide when the system itself is generating the signals. The risk of overfitting is enormous.

But the architecture is what's interesting. The idea of closing the loop, signal generation, validation, and refinement in a single autonomous pipeline, is where systematic investing is likely heading.

Worth reading as a directional piece, not as a performance claim.

📄 Paper: arxiv.org/abs/2603.14288

---

→ Join the newsletter: ivanblanco.ai/newsletter

---

English