CompoundingAI

2.8K posts

CompoundingAI

@compoundingaiin

Institutional Grade AI Market Research Assistant Substack : https://t.co/cyPsc6BDHB Connect: https://t.co/3sGFd13wee

Beigetreten Eylül 2024

42 Folgt4.1K Follower

Despite positive FCF and near-zero debt, Titan Biotech shows early signs of stress:

-Operating cash flow is declining (~5%)

-Net margins have compressed ~300 bps

-ROCE has dropped sharply: 25.18% → 23.91% → 17.01%

-Costs (employee + depreciation) are rising much faster than revenue

Note : No Buy/Sell Reco. Content for educational purposes.

CA Manish Goel@StockGoel

Cash Flow Quality: Why Titan Biotech’s Operating Cash Flow Validates Every Rupee of Profit — How Indian Investors Can Use Cash Flow Analysis to Separate Real Earnings from Accounting Illusions

English

Nazara Technologies is pivoting from a local gaming firm to a global consolidator. Key takeaways from MD Nitish Mittersain latest interview with ET Now :

1. The Cleanup

Nazara has written off its ₹900Cr+ investment in PokerBaazi. The Real Money Gaming (RMG) sector in India is dead for them due to regulatory hurdles. They are now 100% focused on social gaming and esports.

2. Doubling Scale

The Spain acquisition (Best Play & Blue Tile Games) adds ₹1,400Cr in revenue and ₹250Cr in EBITDA. This effectively doubles Nazara’s proforma financials for FY27.

3. Financial Firepower

Cash Position: ₹700Cr currently on hand.

New Capital: Raising ₹500Cr via warrants.

Target: Zero debt and 20-25% margins.

4. Global Footprint

90% of revenue now comes from outside India, with 60% from North America. They are operating as a global holding company using Indian centers of excellence for backend tech and UA.

5. The 2030 Goal

Mittersain is targeting ₹10,000Cr in revenue by 2030. Success depends on their ability to integrate international acquisitions and maintain organic growth in social gaming.

Note : No Buy/Sell Reco

English

Likhitha Infrastructure stock has gone up by ~40% since this post.

Read this thread to look at the risks before you press that buy button.

The upside is factored in but risks aren't.

You would't want to end up being a forced long term investor.

Note : No Buy/Sell Reco.

CompoundingAI@compoundingaiin

THE CATALYST LPG supply will be CUT OFF if you don't switch to PNG where available. This is a government-forced catalyst for Likhitha Infrastructure, India's pure-play gas pipeline EPC company. Stock down 48% YTD from highs. The question: Can they capitalize?

English

Daily Market Digest - 6 April 2026 by CompoundingAI

Markets closed red. Sensex -241 pts. Nifty -84 pts. Pharma, Defence, Infra all weaker. Brent above $120, rupee near ₹95. RBI MPC in session - rate decision Friday.

Order wins from BSE filings:

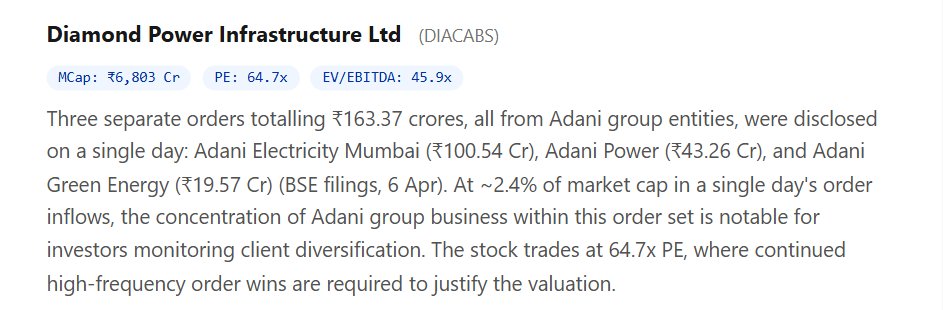

→ Diamond Power Infra: ₹163 Cr in a single day - all three orders from Adani group entities. Client concentration worth watching at 64.7x PE.

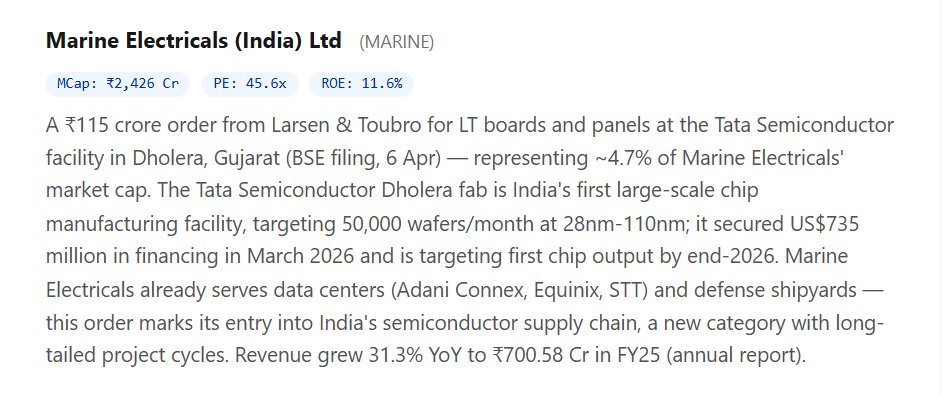

→ Marine Electricals: ₹115 Cr from L&T for the Tata Semiconductor Dholera fab. First semiconductor supply chain order. New category, long-tailed cycles.

→ Avantel: ₹11.59 Cr from NSIL. Fourth consecutive ISRO-ecosystem win. ₹459 Cr + ₹122 Cr preceded it. 221x PE — execution now has to catch up.

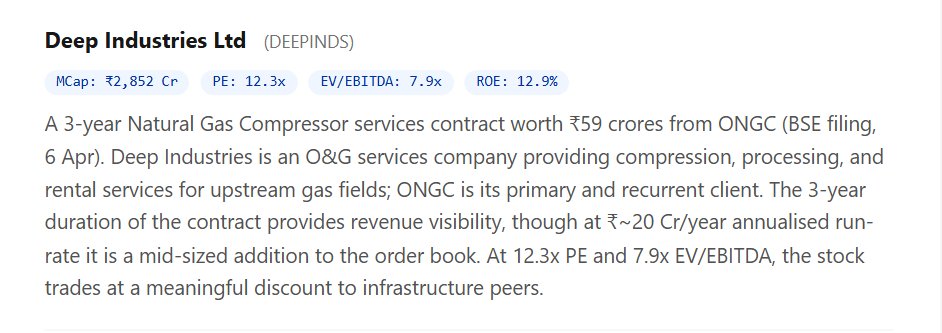

→ Deep Industries: ₹59 Cr / 3-year compressor services contract from ONGC. ~₹20 Cr/year run-rate. 12.3x PE, 7.9x EV/EBITDA.

→ Texmaco Rail: ₹39 Cr from Southern Railway for OHE systems. Order book down from ₹8,194 Cr to ₹5,661 Cr — awaiting fresh tenders.

Other:

→ YES Bank: Vinay Tonse (ex-SBI) takes charge as MD & CEO. ROE at 5.46%, P/BV at 1.13x. Recovery story - now needs a returns story.

→ Blue Cloud Softech: ₹372 Cr acquisition of US entity Global Impx + simultaneous MD change. Structural shift for a ₹1,462 Cr MCap company.

→ POCL: 6.91% promoter stake transmitted via inheritance. Not a market transaction but free float tightens.

Powered by CompoundingAI

Note : No Buy/Sell Reco

English

Diamond Power Infrastructure (DIACABS)

₹163.37 Cr in orders - all from Adani group entities — disclosed on a single day. BSE filing, 6 Apr.

Adani Electricity Mumbai: ₹100.54 Cr

Adani Power: ₹43.26 Cr

Adani Green Energy: ₹19.57 Cr

That's ~2.4% of market cap in one-day inflows. The order wins are frequent. The client concentration, however, is now a material monitoring point for any serious investor.

At these multiples, the assumption is that order cadence stays high. Whether that happens without client diversification is the structural question.

Note : No Buy/Sell Reco

English

Marine Electricals (MARINE)

₹115 Cr order from L&T for LT boards and panels at the Tata Semiconductor Dholera fab. BSE filing, 6 Apr.

That's ~4.7% of Marine Electricals' market cap in a single order.

The Dholera fab is India's first large-scale chip manufacturing facility - targeting 50,000 wafers/month at 28nm-110nm, first chip output by end-2026. Marine already serves Adani Connex, Equinix, STT (data centers) and defense shipyards.

This is a new category entry: India's semiconductor supply chain. Long-tailed project cycles, not a one-time win.

FY25 revenue: ₹700.58 Cr (+31.3% YoY). At 45.6x PE, execution in this new vertical will be watched closely.

Note : No Buy/Sell Reco

English

Deep Industries (DEEPINDS)

₹59 Cr, 3-year Natural Gas Compressor services contract from ONGC. BSE filing, 6 Apr.

Annualised: ~₹20 Cr/year. Mid-sized addition, not a needle-mover in isolation but ONGC is a recurrent client, and the 3-year duration adds revenue visibility to the book.

For an O&G services company with steady ONGC flow, the valuation doesn't demand much. The compression business is capital-light and recurring.

Note : No Buy/Sell Reco

English

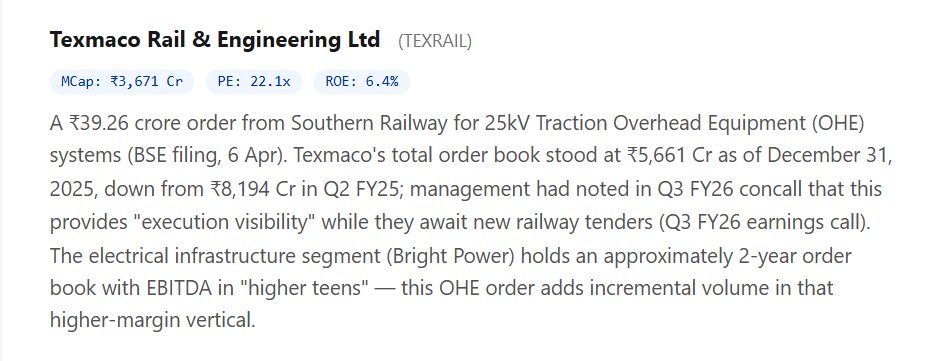

Texmaco Rail & Engineering (TEXRAIL)

₹39.26 Cr order from Southern Railway for 25kV Traction OHE systems. BSE filing, 6 Apr.

Total order book: ₹5,661 Cr as of Dec 31, 2025 - down from ₹8,194 Cr in Q2 FY25. Management acknowledged the decline on the Q3 FY26 call and is awaiting fresh railway tenders.

The OHE order lands in Bright Power (electrical infra), which runs EBITDA in "higher teens" - the higher-margin segment within the business.

22x PE, 6.4% ROE. Execution-dependent story while the order book rebuilds.

English

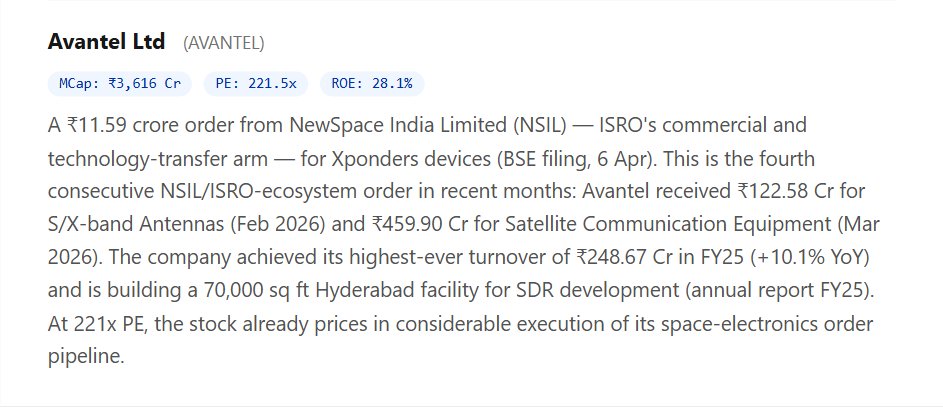

Avantel Ltd (AVANTEL)

₹11.59 Cr order from NSIL for Xponders devices. Fourth consecutive NSIL/ISRO-ecosystem win in recent months.

For context: ₹122.58 Cr (S/X-band Antennas, Feb 2026) → ₹459.90 Cr (Satellite Comms Equipment, Mar 2026) → now ₹11.59 Cr.

FY25 turnover: ₹248.67 Cr (+10.1% YoY).

New 70,000 sq ft SDR facility underway in Hyderabad.

Stock at 221x PE. The order pipeline is visible. Whether execution catches up to the valuation - that's the real question.

BSE filing, 6 Apr.

English

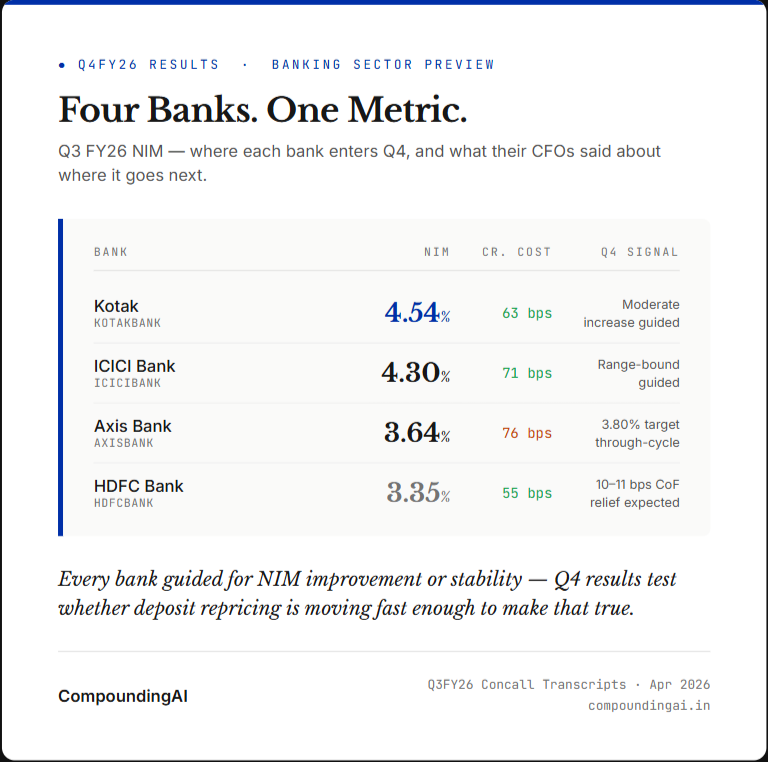

Banking results start this week. Four CFOs made specific commitments in Q3. Here is what they said and what Q4 must show.

The NIM leaderboard entering Q4: Kotak at 4.54%. ICICI at 4.30%. Axis at 3.64%. HDFC at 3.35%.

What each CFO committed to:

Devang Gheewalla, CFO, Kotak Mahindra Bank: "We will see a moderate increase in Q4 NIM." Starting from 4.54% - the highest in the peer set, a moderate increase means Kotak exits FY26 at or above 4.6%.

Sandeep Batra, Executive Director, ICICI Bank: "NIM should be range-bound going forward." Range-bound at 4.30% is a defence, not an improvement. Q4 confirms whether ICICI holds that level or whether unsecured retail stress bleeds into the spread.

Amitabh Chaudhry, MD & CEO, Axis Bank: "We maintain our through-cycle NIM guidance of 3.80%." Q3 NIM was 3.64% - 16 bps below the stated target. Through-cycle is a long horizon, but Q4 direction matters. Flat or declining from 3.64% makes the 3.80% target a question, not a commitment.

Srinivasan Vaidyanathan, CFO, HDFC Bank: "Two-thirds of the 125 bps policy rate change has flowed through. We expect 10–11 bps change in cost of funds this quarter." HDFC at 3.35% NIM has the most structural ground to recover. The 10-11 bps CoF relief is the mechanism. Q4 shows whether that relief actually reached the NIM line or was absorbed elsewhere.

The spread between the best and worst is 119 bps. That gap does not exist because of loan mix alone - it reflects years of divergent deposit franchise quality. Q4 will not close it. But it will show whether each bank is moving in the direction their CFO promised.

One number that does not get enough attention:

Ashok Vaswani, MD & CEO, Kotak: credit costs at 93 bps in Q1, 79 bps in Q2, 63 bps in Q3. Thirty basis points of sequential improvement across three quarters. His words: "normalization to continue, though at a more moderated pace." The easy compression is done. Q4 shows the floor.

Credit costs across all four banks are converging downward - Kotak 0.63%, HDFC 0.55%, ICICI 0.71%, Axis 0.76%. The direction is consistent. The pace of further improvement is what separates the Q4 reads.

CompoundingAI provides contextual analysis on every banking result within 5 mins of announcement.

English

@InvestInMicro We wrote about this today, do give it a read.

open.substack.com/pub/compoundin…

English

Canvas from Europe

Paint from Italy

Artist from India

History on a wall…😎

Indian Tech & Infra@IndianTechGuide

🚨 Serum Institute's Cyrus Poonawalla buys Raja Ravi Varma painting for record Rs 167 crore.

English

@dhanesh500 This is not how it works in India.

We wrote about this today, do give it a read.

open.substack.com/pub/compoundin…

English

Paintings are one of the most powerful financial instruments in the world used by the ultra rich.

Here’s why:

> They buy a painting for ₹150 crore

> An appraiser values it at ₹500 crore a few years later

> They donate it to a museum/charity

They don’t get deduction on ₹150 crore,

They get deduction on ₹500 crore !!

Now add the main layer to this :

Many UHNIs don’t even keep the art at home,

They store it in “Freeports” in places like Geneva, Singapore or Luxembourg

Freeports are tax free warehouses where art can be stored for years without import duty or immediate capital gains tax

The artwork can even be sold multiple times while sitting in the same warehouse because technically it never entered the country

So the painting doesn’t move,

but ownership changes and money moves tax free

The elites truly work differently…

Indian Tech & Infra@IndianTechGuide

🚨 Serum Institute's Cyrus Poonawalla buys Raja Ravi Varma painting for record Rs 167 crore.

English

@raghavwadhwa We wrote about this today, do give it a real. We would appreciate your opinion on this.

open.substack.com/pub/compoundin…

English

Art is the richest man's tax loophole and nobody talks about it.

Until 2007, painting gains in India were completely tax free. Zero. Paintings were "personal effects" under the Income Tax Act. Buy for ₹10 lakh, sell for ₹10 crore, owe nothing.

Even today, art is the most opaque asset class in the country. No centralized registry. No mandatory registration of ownership transfers. No stamp duty. No exchange recording the trade. Two collectors can transact ₹100 crore in a living room and no government entity will ever know.

Globally, billionaires store art in "freeports" (Geneva, Singapore, Delaware). Paintings sit legally "in transit" for decades. No import duty. No capital gains. No wealth tax. The Geneva freeport alone holds ~1.2 million artworks. The European Parliament literally called them spaces where "trade can be conducted untaxed and ownership concealed."

The Poonawallas already own Rembrandt, Van Gogh, Picasso, Renoir, Damien Hirst.

This ₹167 crore Raja Ravi Varma is not a painting purchase. It's a wealth strategy disguised as culture.

Indian Tech & Infra@IndianTechGuide

🚨 Serum Institute's Cyrus Poonawalla buys Raja Ravi Varma painting for record Rs 167 crore.

English

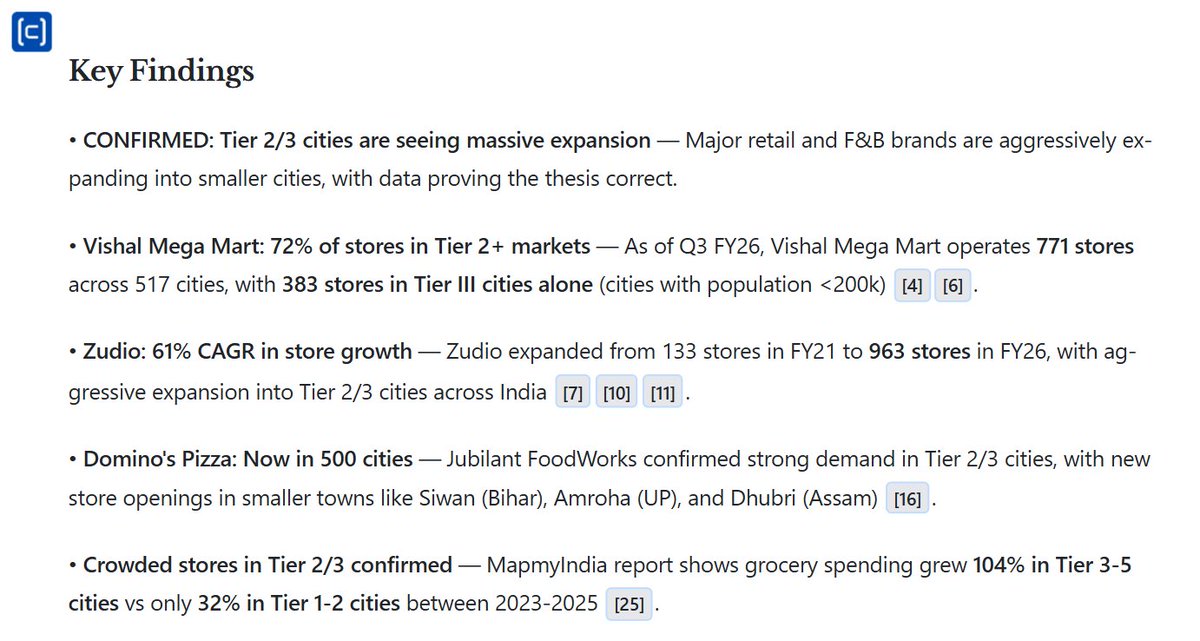

Tier 2 and Tier 3 cities are seeing massive expansion.

Brands like Vishal Mega Mart, Zudio, Domino's Pizza, and other café and food chains are going deeper into these markets, opening large-format stores.

They’re setting up big showrooms in smaller cities, driving high footfall, operating on low margins, and relying on fast inventory turnover.

It’s a scale game.

And it’s crazy how these stores are often more crowded than those in Tier 1 cities.

English

Saudi Arabia needs 4,000 km of new gas pipeline. The only Indian company inside the gate is Welspun Corp. Read on to understand the thesis!

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WELSPUN CORP LIMITED

NSE: WELCORP | BSE: 532144

CMP: ₹846.85 | April 5, 2026

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The most mispriced infrastructure

franchise on the NSE right now.

Three countries. Three once-in-a-decade

buildouts. One company. Trading at 9.3x

FY28 earnings.

In May 2026, every screener in India will

show a Welspun Corp PAT decline.

The algorithms will sell.

The Twitter crowd will call it a red flag.

Here is what they will all get wrong:

FY25 reported PAT of ₹1,900 Cr included

a ₹470 Cr one-time gain from a partial

EPIC stake sale. That gain will not repeat.

Strip it out. Adjusted FY25 operating PAT

was ₹1,430 Cr.

My FY26 estimate: ₹1,600 Cr adj PAT.

That is +11.9% real operating growth.

The coming "decline" is a manufactured

optical illusion from one non-recurring

line item that screeners cannot strip out.

That illusion is precisely why this entry

window exists at ₹846 today.

📊 Verified Sources:

→ WCL NSE/BSE Quarterly Filings ✅

→ Q3 FY26 Earnings Call Transcript ✅

→ CARE Ratings AA+ Reaffirmation Dec 2025 ✅

→ CRISIL AA+ Upgrade July 2, 2025 ✅

→ Screener.in | Smart-Investing.in ✅

→ All forward estimates are personal and

independent. Not SEBI registered.

Label applies to every number below.

⚠️ NOT SEBI REGISTERED. NOT INVESTMENT

ADVICE. DYOR. PURELY EDUCATIONAL.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧱 CHAPTER 1: WHAT THIS COMPANY IS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Picture three workshops across the planet.

One in Anjar, Gujarat. One in Little Rock,

Arkansas. One in Dammam, Saudi Arabia.

Each workshop takes massive steel coils,

bends and welds them into large-diameter

pipes, then ships them to oil majors,

water utilities, LNG terminal builders,

and gas grid operators who have no

alternative qualified supplier at that

precise specification.

That is Welspun Corp.

The moat is deceptively simple:

API-certified large-diameter pipe

manufacturing takes 3 to 5 years and

hundreds of crores to build. The new US

LSAW mill (end-FY27) will produce pipes

from 6 to 56 inches. It will be the ONLY

facility in the United States with 56-inch

capability. Zero competitors replicate

that by FY28.

REVENUE SEGMENTS (WCL Filing ✅):

→ 🇮🇳 India Line Pipes: Oil, LNG, gas

transmission. Largest volume segment.

→ 🇮🇳 Ductile Iron (DI) Pipes: Jal Jeevan

Mission water. ~20% EBITDA margin.

→ 🇺🇸 US Line Pipes: LNG export + AI data

centre gas pipelines. Fully booked FY27.

→ 🇮🇳 TMT Bars: Construction rebar.

→ 🇮🇳 Stainless Steel Pipes: Defense,

BHEL, industrial. Turning profitable FY26.

→ 🇮🇳 Sintex OPVC: Premium plastic pipes.

The consensus calls this a "commodity

cyclical." The consensus is wrong.

Here is the proof:

EBITDA per tonne (CARE Ratings ✅):

→ FY23 trough: ₹6,577/t

→ FY24: ₹11,031/t

→ FY25: ₹11,922/t

+81% unit margin expansion in two years

while HRC steel prices were FALLING.

A commodity business cannot do that.

This is a permanent product-mix shift.

Every DI tonne adds 700-800 bps of margin

over a line pipe tonne. Permanently.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 CHAPTER 2: THE THREE-ACT STORY

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎬 ACT 1 THE STRESS TEST (FY21-FY23):

Net debt peaked at ₹3,316 Cr (FY23 ✅).

Interest coverage fell to 2.06x (FY23 ✅).

Margins at trough: 5.1% EBITDA (CARE ✅).

US underutilised. DI not yet at scale.

This fear moment permanently discounted

the stock into a value trap narrative.

🎬 ACT 2 THE SILENT REBUILD (FY23-FY25):

While the market stared at falling revenue,

management executed a clear blueprint:

→ DI capacity India: scaling to 400 KTPA.

→ EPIC JV: 26.5% Saudi stake established.

→ US LSAW: new mill planning commenced.

→ DRI Plant: ₹659 Cr investment launched.

→ Debt crushed from ₹3,316 Cr to NET CASH.

→ CRISIL upgraded to AA+ (July 2025 ✅).

→ ₹1,722 Cr capex deployed in 9M FY26

while staying net cash. Rare discipline.

🎬 ACT 3 THE COMPOUNDING BEGINS (FY26+):

Three geographies firing simultaneously.

Record order book ₹23,600 Cr in Q3 FY26.

ROCE annualised: 24.4% (Earnings Call ✅).

US fully booked FY27. Saudi DI commissioning.

India LNG + CGD + JJM all running. FCF

inflects massively in FY28. The buildout

cost is nearly fully deployed. From here,

every incremental rupee of capex is

maintenance, not construction.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🌍 CHAPTER 3: THREE-GEOGRAPHY ENGINE

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🇮🇳 INDIA: FOUR DEMAND WALLS, ALL RISING

→ Jal Jeevan Mission:

₹70,000 Cr budget, extended to FY28.

DI demand: ~220 KT (FY25) to 400+ KT

estimated by FY28. EBITDA ~20% (CARE ✅).

→ City Gas Distribution:

₹40,000 Cr investment by 2034.

(MD, Q3 FY26 Earnings Call ✅)

→ LNG Terminals:

India growing from 52 MTPA to 86 MTPA.

Five new terminals by 2030. Every terminal

needs high-spec transmission pipe.

(MD, Q3 FY26 Earnings Call ✅)

→ DRI Plant, Anjar Gujarat:

255 KTPA sponge iron. Capex ₹659 Cr.

FY27 commissioning. Replaces 15-20% of

HRC market purchases permanently.

Annual RM savings: ₹150-220 Cr from FY27.

🇺🇸 US: THE AI PIPELINE TRADE

MD direct quote, Q3 FY26 Call (verbatim ✅):

"We are seeing a significant demand,

continuing demand for the pipelines and

they are all driven by basically movement

for gas pipelines either for LNG export

or primarily for data centers. We are

seeing a surge of data centers coming up

in US and with each data center they have

to have their own power plant and all

those power plants requires uninterrupted

gas for which pipelines are required.

So we are into the part of the value

chain of the AI data center."

→ US order book: Fully booked FY27.

Partial bookings into FY28.

8 to 9 pipeline projects under active

discussion beyond what is already awarded.

→ New US LSAW Mill, Little Rock (end-FY27):

6 to 56 inch diameter range.

ONLY such facility in the United States.

No competitor replicates in under 3 years.

US premium ASP: USD 800-900/tonne.

🇸🇦 SAUDI: THE LARGEST OPTIONALITY

MD direct quote, Q3 FY26 Call (verbatim ✅):

"They are contemplating to put almost 4,000

kilometres of new pipeline. Master Gas

Phase 4 is about to go to 11.8 bcf per day.

From 11.8 bcf to 16.6 bcf per day."

→ Saudi DI Plant: Commissioning H1 FY26.

First local DI manufacturer in Middle East.

2/3 of Saudi DI currently imported.

Anti-dumping on DI imports "likely

beneficial." (Management, Q3 FY26 ✅)

Revenue potential: ₹800-1,200 Cr/yr.

→ Dammam LSAW MoU (January 2026):

350 KTPA with Saudi Aramco.

Converts to contract by Q3 FY27: adds

₹3,500-5,000 Cr revenue from FY28-29.

→ EPIC JV: 26.5% stake, Tadawul-listed.

Recurring JV income + strategic moat.

Jaffura gas network + anti-dumping

both lift EPIC's forward earnings.

→ April 2026 geopolitics:

Saudi east-west crude bypass expansion

post Hormuz tensions = unmodelled

incremental pipeline cycle.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 CHAPTER 3B: UNIT ECONOMICS MATTER MOST

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The most important number in this thesis

is not revenue. Not P/E. Not market cap.

It is EBITDA per tonne. Because it tells

you whether this is a real business or a

volume game dressed up in growth clothes.

EBITDA/TONNE TREND (CARE Ratings ✅):

→ FY23: ₹6,577/t (this was trough fear)

→ FY24: ₹11,031/t (+67.7%)

→ FY25: ₹11,922/t (+8.1%)

→ Q3 FY26: ~₹16,963/t (calc from

₹616 Cr EBITDA / ~363 KT volume)

That is +158% unit margin growth in

three years, in a so-called commodity.

THE MECHANISM:

→ One India DI pipe tonne earns ~20%

EBITDA (CARE ✅) vs ~12-13% for a

line pipe tonne. That is +700-800 bps

per DI tonne added to the mix.

→ One US LSAW tonne: USD 800-900/t ASP.

At ₹86/USD that is ₹68,800-77,400/t.

The margin delta vs India is structural.

→ DRI from FY27 saves ₹500-800/t on RM

cost permanently vs market HRC buyers.

These three forces compound together.

That is not a cyclical recovery.

That is a permanent architecture shift.

SENSITIVITY CHECK:

→ Every ₹1,000/t RM (HRC) change at

1,638 KT FY26 volume:

EBITDA impact: ~₹100-120 Cr

PAT impact: ~₹70-90 Cr

→ Forward cover: 2 quarters always held.

(Management, Q3 FY26 ✅)

P&L lag: 2-3 quarters post spot change.

ROIC ON DEPLOYED CAPITAL:

→ Cumulative capex FY24-FY28: ~₹6,600 Cr

→ Incremental EBIT by FY28 vs FY24:

~₹1,630 Cr additional EBIT

→ ROIC = 24.7% vs WACC ~11%

(AA+ rated, 0.12x D/E, low risk)

→ Every rupee invested creates ₹2.25 of

enterprise value. Textbook value-creation.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💬 CHAPTER 3C: MANAGEMENT QUALITY SCORE

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

→ Acknowledged misses honestly?

YES. JJM sluggishness stated directly.

No corporate speak. ✅

→ Specific numbered guidance?

YES. ₹2,200 Cr EBITDA target.

4,000 km Saudi pipeline quoted.

8-9 active US pipeline discussions. ✅

→ Consistent with last quarter guidance?

YES. 8 straight quarters of delivery. ✅

→ Capital allocation under pressure:

₹1,722 Cr capex in 9M FY26 while

staying NET CASH. ✅

→ Debt discipline:

D/E from 0.70x (FY22) to 0.12x (FY25)

during three simultaneous buildouts. ✅

→ Credit recognition:

Two agencies upgraded to AA+ same year.

CRISIL July 2025. CARE December 2025.

That does not happen by accident. ✅

→ Auditor: Deloitte + MSKA. No change

in 3 years. Clean books. ✅

MANAGEMENT CONCALL SCORE: 5/5 ✅

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 CHAPTER 4: THE VERIFIED NUMBERS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Q3 FY26 ACTUALS (NSE Filing ✅):

→ Revenue: ₹4,532 Cr (+25.4% YoY)

→ EBITDA: ₹616 Cr (+41.7% YoY)

→ EBITDA Margin: 13.6% vs 12.1% year ago

→ Adj PAT: ₹365 Cr (+60.3% YoY)

8 STRAIGHT QUARTERS OF EBITDA GROWTH:

→ Q3 FY25: EBITDA ₹434 Cr | PAT ₹228 Cr

→ Q4 FY25: EBITDA ₹460 Cr | PAT ₹172 Cr

→ Q1 FY26: EBITDA ₹525 Cr | PAT ₹300 Cr

→ Q2 FY26: EBITDA ₹591 Cr | PAT ₹348 Cr

→ Q3 FY26: EBITDA ₹616 Cr | PAT ₹365 Cr

PAT grew ₹228 Cr to ₹365 Cr in 12 months.

That is +60%. Compound this forward.

OCF QUALITY (Screener.in ✅):

→ FY24: OCF/PAT = 96% | FY25: 109%

→ 2-year avg: 102.5%. No earnings tricks.

BALANCE SHEET TRANSFORMATION:

→ Net debt FY23: ₹3,316 Cr

→ Net debt FY24: ₹820 Cr

→ Net CASH FY25: ₹340 Cr

→ Net CASH Q3 FY26: ₹132 Cr ✅

→ D/E ratio FY25: 0.12x ✅

→ Interest Coverage ~12x annualised ✅

→ CRISIL AA+/Stable (Jul 2025 upgrade ✅)

→ CARE AA+/Stable (Dec 2025 reaffirm ✅)

SHAREHOLDING (NSE Dec 2025 ✅):

→ Promoter: 49.7% | Pledge: 0.0%

→ FII: 11.5% | DII: 20.6%

→ Zero pledge for 3 consecutive quarters.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔮 CHAPTER 5: PROJECTIONS

All numbers below are personal

independent estimates unless labeled ✅

Macro: HRC ₹48K-56K/t, INR/USD ₹86-96,

Brent $70-85, 25% tax, JJM extended FY28

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

9M FY26 base (WCL Filing ✅):

→ Revenue ₹12,457 Cr | EBITDA ₹1,732 Cr

→ Adj PAT ₹1,013 Cr

FY26E:

→ Revenue: ₹17,550 Cr (+25.6% YoY)

→ EBITDA: ₹2,365 Cr | Margin: 13.5%

→ D&A ₹420 Cr | Interest ₹220 Cr

→ Other Income (JV+treasury): ₹400 Cr

→ Adj PAT: ₹1,600 Cr | EPS: ₹60.5

→ FCF: ~₹580 Cr | Net Debt: ~₹100 Cr

→ BV/share: ~₹335

⚠️ Screener will show PAT "decline" vs

FY25 ₹1,900 Cr because FY25 had ₹470 Cr

one-time EPIC gain. Adj growth: +11.9%.

Screeners lie. This is the entry window.

FY27E: (Saudi DI full yr, DRI online H1,

US LSAW partial Q4)

→ Revenue: ₹20,875 Cr (+19.0% YoY)

→ EBITDA: ₹2,643 Cr | Margin: 12.7%

→ D&A ₹540 Cr | Interest ₹165 Cr

→ Other Income: ₹460 Cr

→ Adj PAT: ₹1,895 Cr | EPS: ₹71.8

→ FCF: ~₹790 Cr | Net Debt: ~₹3,000 Cr

(US LSAW project finance drawn down)

→ BV/share: ~₹390

Net Debt/EBITDA: below 1.2x ✅

FY28E: THE INFLECTION YEAR

(US LSAW full year 424 KT, capex drops

from ₹2,100 Cr to ₹600 Cr, FCF explodes)

→ Revenue: ₹28,000 Cr (+34.1% YoY)

→ EBITDA: ₹3,500 Cr | Margin: 12.5%

Note: Two independent models (top-down

and bottom-up) BOTH arrive at ₹3,500 Cr.

That convergence is not coincidence.

→ D&A ₹615 Cr | Interest ₹195 Cr

→ Other Income: ₹510 Cr

→ Adj PAT: ₹2,400 Cr | EPS: ₹90.9

→ FCF: ₹2,400 Cr | FCF/share: ₹90.9

→ FCF Yield at CMP ₹846.85: 10.7%

→ Net Cash: ~₹8,500 Cr

→ BV/share: ~₹479

₹100 invested today earns ₹10.7 pure free

cash annually from FY28. Best AA+ FD pays

₹6.5. WCL grows revenue at 27% CAGR.

FY29E: (US LSAW 85%+ util, Saudi LSAW P1,

India CGD full swing, DRI full savings)

→ Revenue: ₹34,000 Cr (+21.4% YoY)

→ EBITDA: ₹4,420 Cr | Margin: 13.0%

→ Adj PAT: ₹3,100 Cr | EPS: ₹117.4

→ FCF: ~₹3,500 Cr | Net Cash: ~₹13,000 Cr

→ BV/share: ~₹579

FY30E: (H2/CCUS specs emerging, Saudi P2,

India CGD near complete, US wave 2)

→ Revenue: ₹40,500 Cr (+19.1% YoY)

→ EBITDA: ₹5,470 Cr | Margin: 13.5%

→ Adj PAT: ₹3,850 Cr | EPS: ₹145.8

→ FCF: ~₹4,500 Cr | Net Cash: ~₹18,500 Cr

→ BV/share: ~₹690

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 CHAPTER 6: UPSIDE CALCULATOR

CMP ₹846.85 | 26.4 Cr shares

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PEER CONTEXT:

→ APL Apollo: ~47x P/E (branded ERW)

→ Jindal SAW: ~14x P/E (no US/Saudi)

→ Maharashtra Seamless: ~9.3x P/E

→ Sector avg P/E: ~22.7x (NSE Apr 2026)

→ WCL at 11.4x TTM = 50% sector discount

P/E formula: Multiple × EPS

EV/EBITDA: [(Multiple × EBITDA) ± Net Debt]

divided by 26.4 Cr shares

P/B: Multiple × BV/share

FCF Yield: FCF/share divided by yield %

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📅 FY26E (EPS ₹60.5 | BV ₹335)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

P/E:

🐂 17x: ₹1,029 (+22%) | Q4 beats guidance

⚖️ 14x: ₹847 (+0%) | In-line delivery

🐻 10x: ₹605 (-29%) | Screener panic

EV/EBITDA (Net Debt ₹100 Cr):

🐂 12x: ₹1,071 (+26%)

⚖️ 10x: ₹892 (+5%)

🐻 8x: ₹713 (-16%)

P/B:

🐂 3.5x: ₹1,173 (+39%)

⚖️ 3.0x: ₹1,005 (+19%)

🐻 2.0x: ₹670 (-21%)

✅ BASE TP: ₹847-1,005 | BULL: ₹1,029-1,173

Screener dip in May 2026 = entry window.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📅 FY27E (EPS ₹71.8 | BV ₹390)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

P/E:

🐂 18x: ₹1,292 (+53%) | Saudi DI + DRI live

⚖️ 15x: ₹1,077 (+27%) | In-line execution

🐻 11x: ₹790 (-7%) | JJM + HRC spike

EV/EBITDA (Net Debt ₹3,000 Cr):

🐂 11x: ₹986 (+16%)

⚖️ 9x: ₹786 (-7%)

🐻 7x: ₹586 (-31%)

P/B:

🐂 3.5x: ₹1,365 (+61%)

⚖️ 3.0x: ₹1,170 (+38%)

🐻 2.0x: ₹780 (-8%)

✅ PRIMARY ANCHOR: P/E 15x + P/B 3.0x

Base TP: ₹1,077-1,170 (+27-38%)

EV/EBITDA lower as FY27 is peak capex year.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📅 FY28E (EPS ₹90.9 | BV ₹479)

FCF ₹90.9/sh | FCF Yield 10.7%

4 METHODS. ALL CONVERGE.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

P/E:

🐂 20x: ₹1,818 (+115%) | US LSAW full util

⚖️ 16x: ₹1,454 (+72%) | FCF confirmed

🐻 12x: ₹1,091 (+29%) | 1 geo underdelivers

EV/EBITDA (Net CASH ₹8,500 Cr):

🐂 11x: ₹1,784 (+111%)

⚖️ 9x: ₹1,515 (+79%)

🐻 7x: ₹1,249 (+47%)

P/B:

🐂 4.0x: ₹1,916 (+126%)

⚖️ 3.2x: ₹1,533 (+81%)

🐻 2.2x: ₹1,054 (+24%)

FCF YIELD:

🐂 5%: ₹1,818 (+115%)

⚖️ 7%: ₹1,299 (+53%)

🐻 10%: ₹909 (+7%)

SoTP (FY28E):

→ India LP: ₹940 Cr × 7.5x = ₹7,050 Cr

→ DI Pipes: ₹910 Cr × 7.5x = ₹6,825 Cr

→ US LP: ₹1,070 Cr × 8.0x = ₹8,560 Cr

→ Saudi LP: ₹120 Cr × 7.0x = ₹840 Cr

→ SS Pipes: ₹190 Cr × 12.0x = ₹2,280 Cr

→ TMT Bars: ₹160 Cr × 5.0x = ₹800 Cr

→ Sintex: ₹90 Cr × 27.5x = ₹2,475 Cr

→ EPIC JV (26.5%): 12x PAT = ₹2,035 Cr

→ Total EV: ₹30,865 Cr

→ + Net Cash: ₹8,500 Cr

→ Equity: ₹39,365 Cr / 26.4 Cr = ₹1,491/sh

🐂 Bull (Saudi LSAW converts): ₹1,700+

⚖️ Base: ₹1,491

🐻 Bear (Saudi stays MoU): ₹1,180

✅ FY28 VERDICT: VERY HIGH CONVICTION

All 4 methods converge above ₹1,054.

BEAR CASE MINIMUM: +24% to +47%.

Net cash ₹8,500 Cr creates a hard floor.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📅 FY29E (EPS ₹117.4 | BV ₹579)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

P/E:

🐂 22x: ₹2,583 (+205%)

⚖️ 18x: ₹2,113 (+150%)

🐻 13x: ₹1,526 (+80%)

EV/EBITDA (Net Cash ₹13,000 Cr):

🐂 11x: ₹2,338 (+176%)

⚖️ 9x: ₹2,003 (+137%)

🐻 7x: ₹1,667 (+97%)

FCF Yield (FCF ₹132.6/sh):

🐂 5%: ₹2,652 (+213%)

⚖️ 7%: ₹1,894 (+124%)

🐻 10%: ₹1,326 (+57%)

✅ BEAR CASE ALONE: +57-97% from CMP.

That is what asymmetric opportunity

actually looks like on paper.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📅 FY30E (EPS ₹145.8 | BV ₹690)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

P/E:

🐂 25x: ₹3,645 (+330%)

⚖️ 20x: ₹2,916 (+244%)

🐻 14x: ₹2,041 (+141%)

EV/EBITDA (Net Cash ₹18,500 Cr):

🐂 12x: ₹3,187 (+276%)

⚖️ 9.5x: ₹2,669 (+215%)

🐻 7x: ₹2,151 (+154%)

FCF Yield (FCF ₹170.5/sh):

🐂 4%: ₹4,263 (+403%)

⚖️ 6%: ₹2,842 (+235%)

🐻 9%: ₹1,894 (+124%)

✅ BEAR CASE: +124-154%. Not a typo.

A 4-year compounding franchise thesis.

Not a trade.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🕐 WHY RIGHT NOW IS THE ENTRY WINDOW

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Three converging forces create the entry:

→ FORCE 1: Screener Confusion Incoming

May 2026 Q4 results will show PAT "down"

vs FY25 because of the ₹470 Cr one-time

item last year. Most retail investors

will see a red screener and sell.

Institutions who can read a cash flow

statement will buy. Be on the right side.

→ FORCE 2: Capex Peak Is Done

FY26 capex: ₹2,290 Cr. FY27: ₹2,100 Cr.

FY28: ~₹600 Cr. Peak spending is over.

FCF goes from ₹580 Cr to ₹2,400 Cr in

just 24 months. The FCF machine turns on

exactly when the market least expects it.

→ FORCE 3: Geopolitical Tailwind Unmodelled

April 2026: Hormuz tensions accelerate

Saudi bypass pipeline construction.

Zero sell-side models have this.

Zero screeners can model it.

You have the MD's own words from Jan 2026.

4,000 km of new pipeline in Saudi Arabia.

WCL is inside the gate with a JV and

a manufacturing MoU already signed.

When the screener crowd sells in May,

the geopolitical crowd will be buying.

That asymmetry is where you want to be.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ CHAPTER 7: THE HONEST RISK REGISTER

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔴 RISK 1: HRC STEEL SPIKE >15%

→ Trigger: India HRC > ₹60,000/t for 2+ Qs

→ PAT impact: -₹150-200 Cr/year

→ Probability: 30%

→ Monitor: JSW/Tata Steel monthly pricing.

Forward cover below 6 weeks = red flag.

🔴 RISK 2: JJM FUNDING SLOWDOWN

→ Trigger: Fund utilisation <40% for 2+ Qs

→ PAT impact: -₹200-280 Cr (DI -15-20%)

→ Probability: 25%

→ Monitor: jalshakti.gov.in disbursements.

🔴 RISK 3: SAUDI MoU DOES NOT CONVERT

→ Trigger: Dammam LSAW no formal LOI by

Q3 FY27

→ PAT impact: -₹120-180 Cr (FY28-29)

→ Probability: 20%

→ Monitor: WCL BSE/NSE contract filing.

🔴 RISK 4: MAY 2026 SCREENER PANIC

→ PAT optic looks like decline = -10-15%

→ Probability: 75% (near certain)

→ THIS IS AN ENTRY WINDOW, NOT AN EXIT.

→ Watch: Q4 EBITDA > ₹560 Cr = thesis on.

🔴 RISK 5: US LSAW YEAR-1 QUALITY FAIL

→ Trigger: 56-inch batch fails API spec

→ PAT impact: -₹100-150 Cr (FY28 delay)

→ Probability: 15%

→ Monitor: Any NSE warranty/rejection note.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚡ CHAPTER 8: CATALYST CALENDAR

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

→ MAY 2026 [CRITICAL]:

Q4 FY26 results. FY27 guidance issued.

Screener panic = buy zone.

EBITDA > ₹2,365 Cr FY26 = thesis intact.

→ APR-JUN 2026 [HIGH]:

Saudi DI first production announced.

First DI pipe made in Middle East.

Anti-dumping ruling outcome.

Impact: +₹30-50 on stock price.

→ JUN-SEP 2026 [HIGH]:

Dammam LSAW formal Aramco contract.

MoU converts to order = re-rating event.

Impact: +₹50-100 on stock price.

→ Q1-Q2 FY27 [MEDIUM]:

DRI plant Anjar first production.

First RM cost savings hit the P&L.

50-80 bps margin expansion visible.

→ Q4 FY27 [VERY HIGH]:

US LSAW Little Rock commissioning.

Only 6-56 inch mill in United States.

Institutional upgrades begin.

Impact: +₹100-200 over 2 quarters.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CHAPTER 9: FINAL VERDICT

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Three things the market has missed:

1️⃣ THE MISPRICING IS MANUFACTURED:

FY25 had ₹470 Cr one-time EPIC gain.

FY26 "decline" is optical, not operational.

Adjusted operating PAT grows +11.9%.

Screeners lie. Verified cash flows don't.

2️⃣ THE DATA SEALS THE THESIS:

EBITDA/tonne: ₹6,577 (FY23) to ₹11,922

(FY25) while HRC prices fell. (CARE ✅)

+81% unit margin in a "commodity" business.

This is permanent product-mix compounding.

3️⃣ THE NUMBERS MAKE THE CASE:

At CMP ₹846.85, my FY28 FCF yield = 10.7%.

Better than AA+ fixed deposits in India

on a company growing at 27% revenue CAGR.

Bear case FY28: +24-47%. Base: +72-81%.

THE SINGLE CORE INSIGHT:

At 9.3x FY28 earnings, Welspun Corp is

priced as a commodity cyclical while

quietly building the most strategically

positioned large-diameter pipeline

franchise across three continents.

That gap between price and value is

exactly where multi-baggers are born.

📊 RATING: BUY / ACCUMULATE ON DIPS

📊 CONVICTION: HIGH (9/10)

📊 12M TP: ₹1,005-1,170 (+19-38%)

📊 24M TP: ₹1,291-1,454 (+52-72%)

📊 36M TP: ₹1,491-1,818 (+76-115%)

📊 STOP LOSS: ₹680 weekly close

ENTRY PLAN:

→ Tranche 1 (40%): ₹840-870 (now)

→ Tranche 2 (40%): ₹750-800 (May panic)

→ Tranche 3 (20%): Breakout above ₹950

→ Avg entry: ₹820-855

RISK:REWARD at ₹850 entry:

→ Downside to SL: -20%

→ Base 24M upside: +65%

→ R:R = 3.25:1

RAISES CONVICTION TO 10/10:

→ Saudi Dammam formal contract filed

→ FY28 FCF confirmed at ₹2,000 Cr+ actuals

→ FII ownership crosses 13%

FORCES EXIT:

→ Promoter pledge goes non-zero any quarter

→ FY27 OCF/PAT drops below 0.5x for 2+ Qs

→ Saudi LSAW + DI anti-dumping both fail

THIS IS NOT A 3-MONTH TRADE.

This is a 4-year compounding franchise bet.

Three countries. Three once-in-a-decade

buildouts. One pipe maker. One price: ₹846.

The market will eventually price what this

business has become. The question is only

whether you are early enough to matter.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ NOT SEBI REGISTERED. NOT INVESTMENT

ADVICE. ALL FORWARD ESTIMATES ARE

INDEPENDENT PERSONAL PROJECTIONS.

VERIFIED DATA LABELED ✅ THROUGHOUT.

DYOR BEFORE ANY INVESTMENT DECISION.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

#WelspunCorp

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

English

Every number in this thread came from primary source concall transcripts.

30+ banks and NBFCs. Every claim is cited to the source document and page - not a news article, not a screener export.

That's what CompoundingAI does for every result season.

English

Four things the divergence is telling you that analyst reports aren't:

The quality gap is repricing.

Kotak vs. IndusInd at 226 bps wasn't this wide a year ago. The market is starting to pay for clean books.

NRI risk has no model. A 26% deposit outflow scenario doesn't exist in any sell-side note. It will.

Within NBFCs, Bajaj at 0.27% and Shriram at 4.54% are not in the same story. Stop reading them as one.

Headline GNPA is now actively misleading. IDFC First's 1.69% is doing real work hiding a 5.00% MFI book.

SBI Chairman said it directly: strip out rupee depreciation from the 15% growth number before you read Q4. The underlying is 8.7%.

English

One banking system. Two completely different credit cycles running inside it.

226 bps separates the best GNPA from the worst and that gap is still widening.

Q4 results start April 9. This thread is your cheat sheet.🧵

English