Angehefteter Tweet

Venkatram

7.5K posts

Venkatram

@srir54

Product Leader¦ Deep India - Africa connect¦ SaaS +Avid SME and nano cap investor. Information freak and passionate about India

Kenya Beigetreten Temmuz 2009

68 Folgt1.3K Follower

Venkatram retweetet

Akshay Tritiya: The Day of Eternal Beginnings!

👉🏽Parshurama was born.

👉🏽Ganga descended.

👉🏽Sudama met Krishna.

👉🏽Ganesha began writing the Mahabharata.

👉🏽Construction of Jagannath’s Rath Yatra chariot starts today.

What begins on Akshaya Tritiya carries success forever.

Gold may shine in your locker,

but donation shines in Lakshmi’s eyes. 🥰

English

Venkatram retweetet

It's time...

SRIRANGAN E K@sriranganek

#PowerEPC #Transmission #HVDC #GRIDCONNECTIVITY #TRANSFORMERS Transmission EPC has order longevity, long execution cycles, and annuity like cash flows. Terminal phase is impossible with structural peak load rising gradually Either be TBCB transmission or say substation upgrades or BESS connected infra,... it's in the NON TERMINAL recurring phase Folks!! Don't simply get carried away by some useless narratives They are in the mid cycle. Clear order visibility for 132/220/400 and 765kv for the next 2-3 years. PGCIL or Discoms are agreeing for the hike in the prices and it's simply a joke for people to compare this with a pure solar epc players EHV will have durable tailwinds here 120 Gw peak demand estimated by 2030 is no joke right!! We are talking about 8 to 9 lacs crores here. Stop kidding 50+ ISTS projects and 15+ green corridors. Come on Folks, don't get carried away Good order visibility for lower ratings to mid(400kv) to higher ratings 765kv PGCIL and Discomms are agreeing for the price hikes and so pricing power is intact and so the margins Don't forget that re rating is driven by the scarcity premium and let's count how many serious transformers OEMS that deliver EHV/HVDC grade.. 12, 15?? Let's go back to the basic. Terminal valuarion require DEMAND STAGNATION + CAPEX SATURATION. Read somewhere that Quality Power is working on 9x capex and so major players like Shilchar, Atlanta, Danish,... Tell the story tellers that a xyxle becomes cyclical only when TAM is almost saturated and pricing power is substantially lost + capex revival is next to impossible and last but not the least... disruptions destroys underlying demand Now u tell me.. Does power EPC and transmission profit pool have any of fhe above?? Solar EpC is a different story altogether. Pure EPC players will hear the music. But they are transitioning towards RTC + hybrid, solar + BESS, C&I.... Will discuss this some other day To re emphasize the demand to get revised further up anytime soon to cater to AI/DC, semicon push, EV loads, grid modernization, bess integration,.... 765kv + hvdc backlogs are surmounting and people should stop joking by passing some pathetic opinions Temporary slowdown in bidding isn't structural death 🤣🤣 Lastly, Valuation follows fundas and nowhere they are near the terminal phase near peaking out

English

@drjimmy2407 And many more - Sugslloyd, Rajesh power, Oriana Power, Afcom. All I suspect will post their best H2 in their reporting periods.

English

SMEs in momentum and good result expectations yet to reach ATH:

🟠 TaurianMPS

🟠 LTElevator

🟠 Airfloa

🟠 Maxvolt

🟠 Osel

🟠 SystematicInd

🟠 Safe Enterprise

Can be looked on pullbacks...

Any others names?

English

Venkatram retweetet

Mainboard Leaders & Their SME Counterparts - Hidden Opportunities You Can’t Ignore 🔥👇

Waaree Energy →Alpex Solar

Syrma SGS → Aimtron Electronics

Garden Reach Shipbuilders → Krishna Defence (recently migrated)

Transrail Lighting → Rajesh Power / Viviana Power

Yatharth Hospital → UniHealth Hospitals

Cupid → Anondita Medicare

Polycab → JD Cables / Prime Cables

Shilchar Technologies → Danish Power

Amara Raja Energy → Maxvolt Energy

Interarch Building → Sathlokhar Synergys

Acme Solar → Oriana Power

Gravita India → Baheti Recycling

Aditya Infotech → Prizor Viztech

Let’s continue building this list further - you can also add more mainboard players and their SME counterparts to make this list even more comprehensive and insightful.

Disclaimer:

This is for educational purposes only and not investment advice. Please do your own research before investing.

English

Venkatram retweetet

#accretionpharma #accpl why the stock as been forever below IPO price of 101 Here are some reasons why - All new product registrations in new geographies are expensed first hitting financials before they contribute, QIB UHNI are almost nil. If H2 delivers and exports work then 🚀

Venkatram@srir54

#accretionpharma #accpl is shaping up as an export-led SME CDMO with owned manufacturing, multi-country approvals and improving scale. The key monitor now is execution: product registrations converting into direct exports, better mix, margin recovery and tighter working capital.

English

Venkatram retweetet

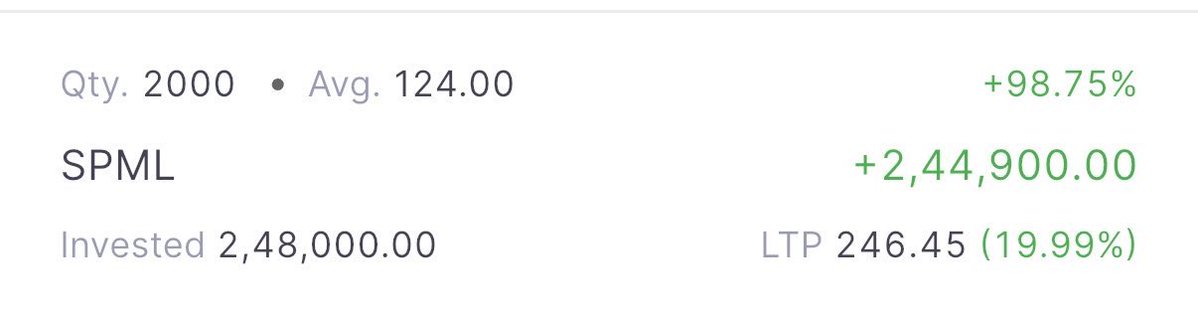

#SPML man what a crazy ride Stock up 60%+ since this post has reached FY26 Fair Value. Future now depends on PE market decides and results. I know some of my friends added this based on my analysis I hope this made a good start to FY27 for them 🙏

Venkatram@srir54

#SPML interesting story to watch. Investment note for the interested.

English

Venkatram retweetet

Energetics — Explosives and Propellant chemicals

The biggest bottleneck in any hot conflict is not the missile systems themselves but the upstream energetic materials (TNT, RDX, nitrocellulose) that feed both conventional and precision munitions. Energetics — explosives and propellant chemicals — are explicitly identified as the binding constraint on shell output, with analysts calling for prioritization of nitric acid, TNT, and nitrocellulose production lines as the core strategic bottleneck.

The demand for military-grade energetics has shifted from "steady state" to "urgent replenishment" as of early 2026. The market for RDX and HMX alone is projected to reach approximately $18.69 billion in 2026, growing at a CAGR of over 5.2%. The primary driver is the massive consumption of artillery and precision munitions in active conflict zones (Ukraine and the Middle East), coupled with a global push for strategic stockpiling.

Prices for military energetics have seen a "double-digit" percentage increase between 2024 and 2026, driven by raw material scarcity and energy costs.

In the West, strict REACH and EPA regulations make opening new TNT/RDX "wet" chemical plants a 5-10 year process.

Many global RDX plants are decades old; downtime for maintenance in these plants is currently causing immediate spikes in global spot pricing.

India has moved from being a net importer of high-energy materials to an exporter.

In India, there are currently about 5 to 10 major private companies with the specific technical capability and industrial licenses (DPIIT/PESO) to manufacture military-grade high explosives (Class 1-3). Globally, there are just 200 companies which are able to make military grade explosives.

Globally, over 1.5 million metric tons of military explosives are manufactured yearly.

💣TNT: Remains the "workhorse," accounting for roughly 55% of the total volume. Over 24 countries maintain active TNT production lines.

💣RDX/HMX: Global production of these high-performance materials exceeded 45,000 metric tons recently, driven by the demand for precision-guided munitions and long-range artillery.

💣Artillery shells: By far the largest explosive-consuming segment by weight and unit count. A standard 155mm M107 projectile contains approximately 6.8 kg of TNT. During active conflict, tens of thousands are fired per day. Russian factories produced approximately 7 million artillery, mortar, tank, and rocket rounds in 2025 — roughly 19,000 rounds per day.

Rajesh Singla@VTGCapital

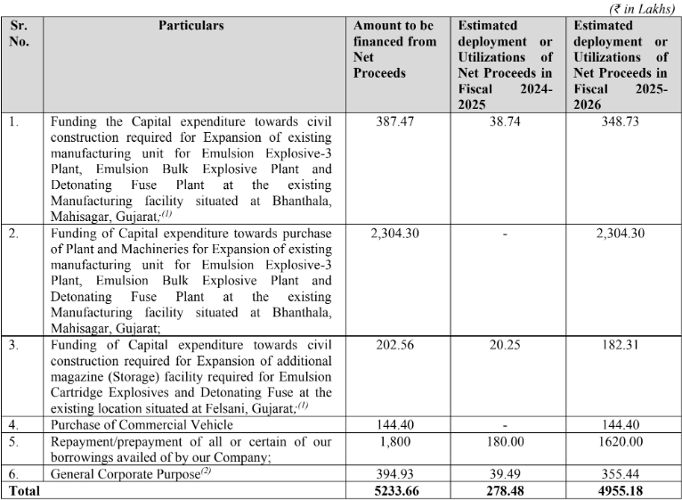

Beezaasan : Scuttlebutt analysis : Quietly building defence capabilities As per one of its peer, Beezaasan is also in the race to get defence licence for RDX, HMX, TNT, Propellent etc. They seem to have already applied for all these licences. The peer also mentioned that it takes 18-24 months from the grant of licence to start production. Last year as per IPO discussions by the management of Beezaasan, their sister company Asawara Earthtech Ltd. had all the defence licenses for production of RDX, HMX, TNT and other products. Recently, Beezaasan acquired 35% stake in this company from promoters. Considering, this company already had defence licences more than a year ago, we expect this company to start the production of defence explosives at the end of FY27 (18-24 months from the grant of licence). Beezaasan's own defence explosive licences might take another two years. Most of the money raised via Beezaasan's IPO would have already been deployed as per the schedule of capex as per DRHP. This expanded capacity should also come on-line during FY27. What all this mean for earnings expectations? 1. Considering new expansion is going to be complete in FY27, FY26 could remain largely muted vs FY25. 2. FY27 : Would see completion of expansion at Beezaasan, may be start of production of defence explosives at 35% owned Asawara Tech. As per Asawara company's valuation report (at the time of preferential issue), Asawara could have a PAT of 58cr in FY27 and 120cr in FY28. Beezaasan's share i.e. 35% of this would be Rs. 20cr and 42cr, respectively. Conservatively, Beezaasan can have a PAT of Rs. 16-25cr, conservatively, assuming delay in start of production at Asawara and may be Beezaasan's expanded capacity as well. If executed well, Beezaasan consolidated PAT could be Rs. 30-40cr in FY27, itself. Better to remain conservative. 3. FY28 : Could see a substantial jump in earnings due to full year of operations at Beezaasan and Asawara new capacity. The PAT could grow to Rs. 40-60cr in FY28 for Beezaasan. 4. FY29 : Could be a big year as the expanded capacity gets scaled up and Beezaasan own defence capacities comes into operation. Conservatively, Beezaasan could have Rs. 100cr PAT. All depends upon execution. FY30 can surprise considering all the defence explosive capacities at Beezaasan and Aswara could be fully operational. Current market cap is Rs. 300cr. Defence explosives is a highly regulated industry and trades at higher valuation multiples. Only for long-term investors with patience. Do your own due-diligence.

English

Venkatram retweetet

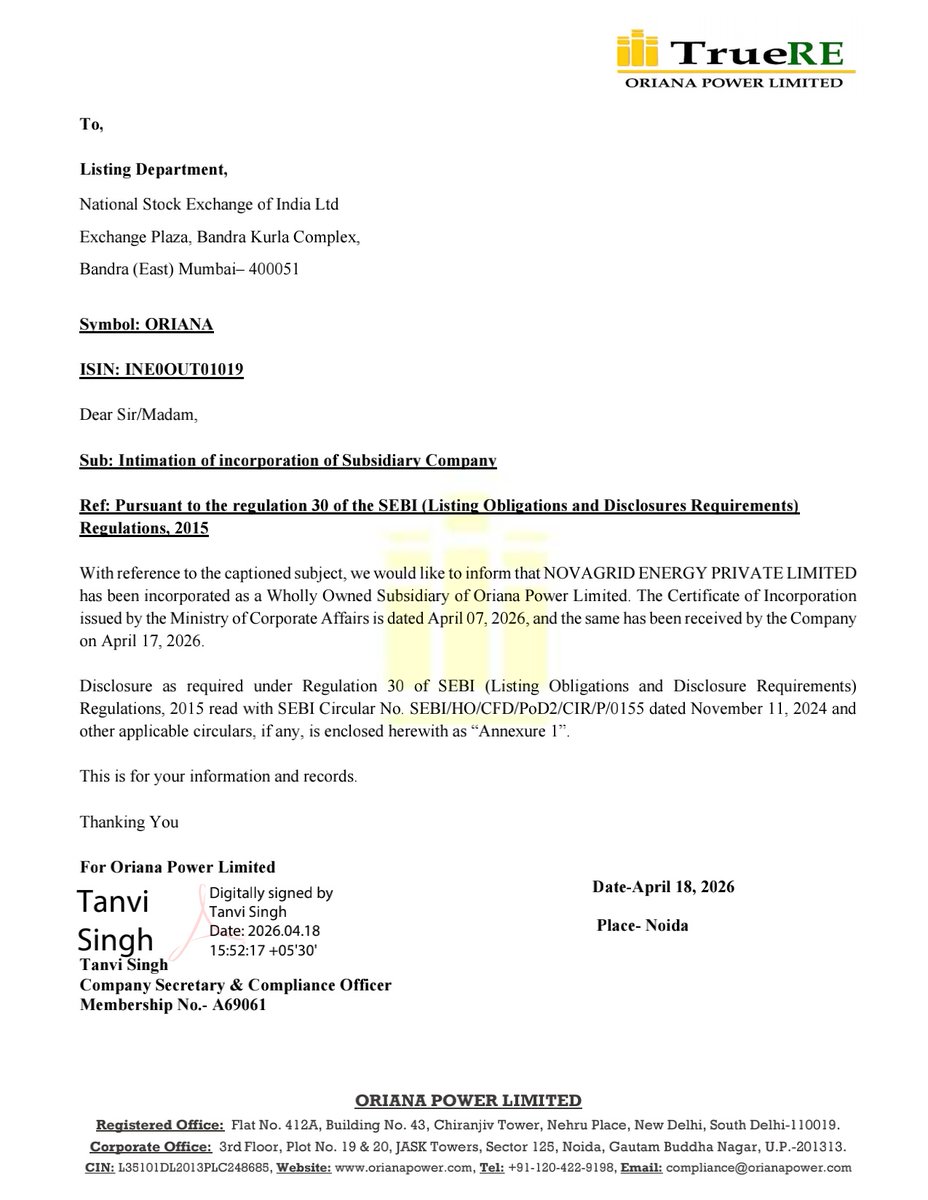

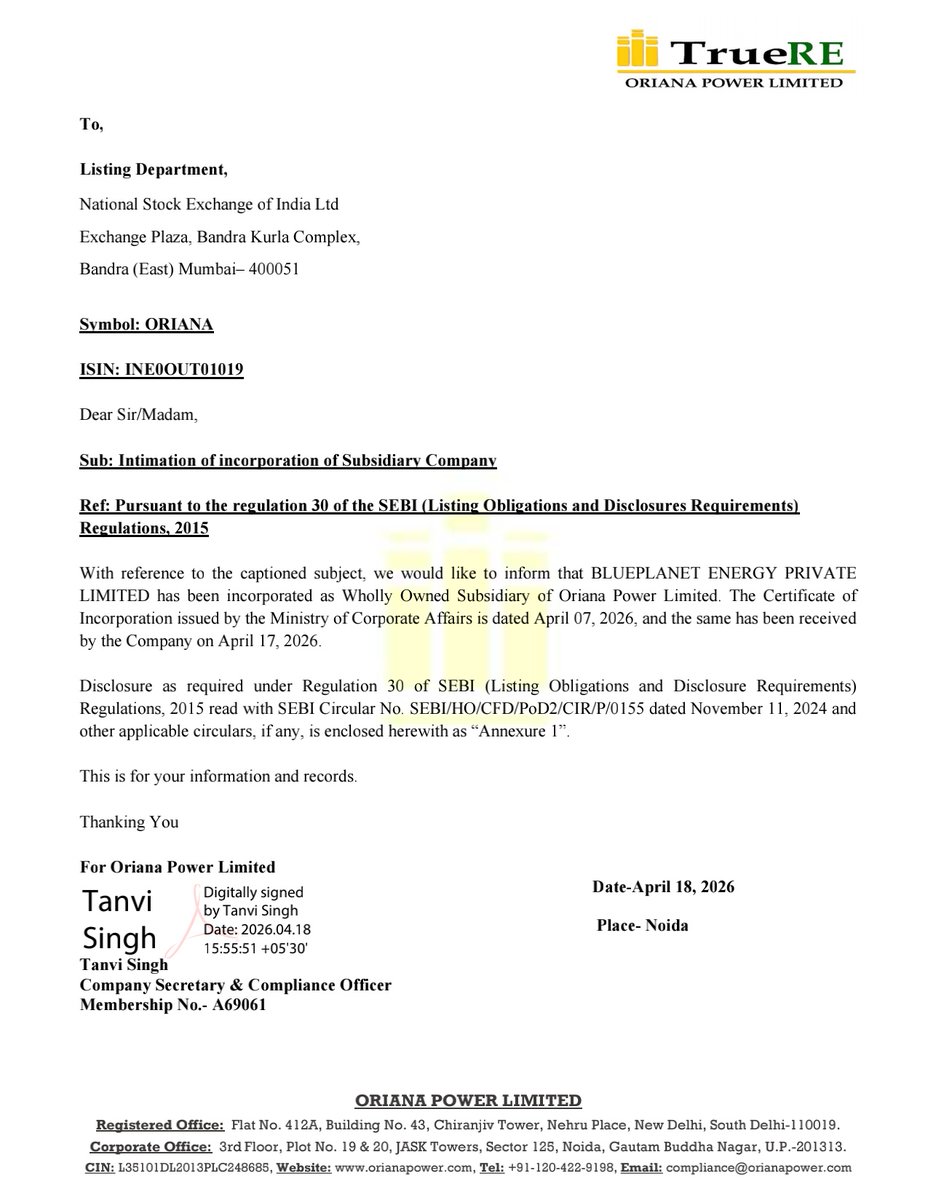

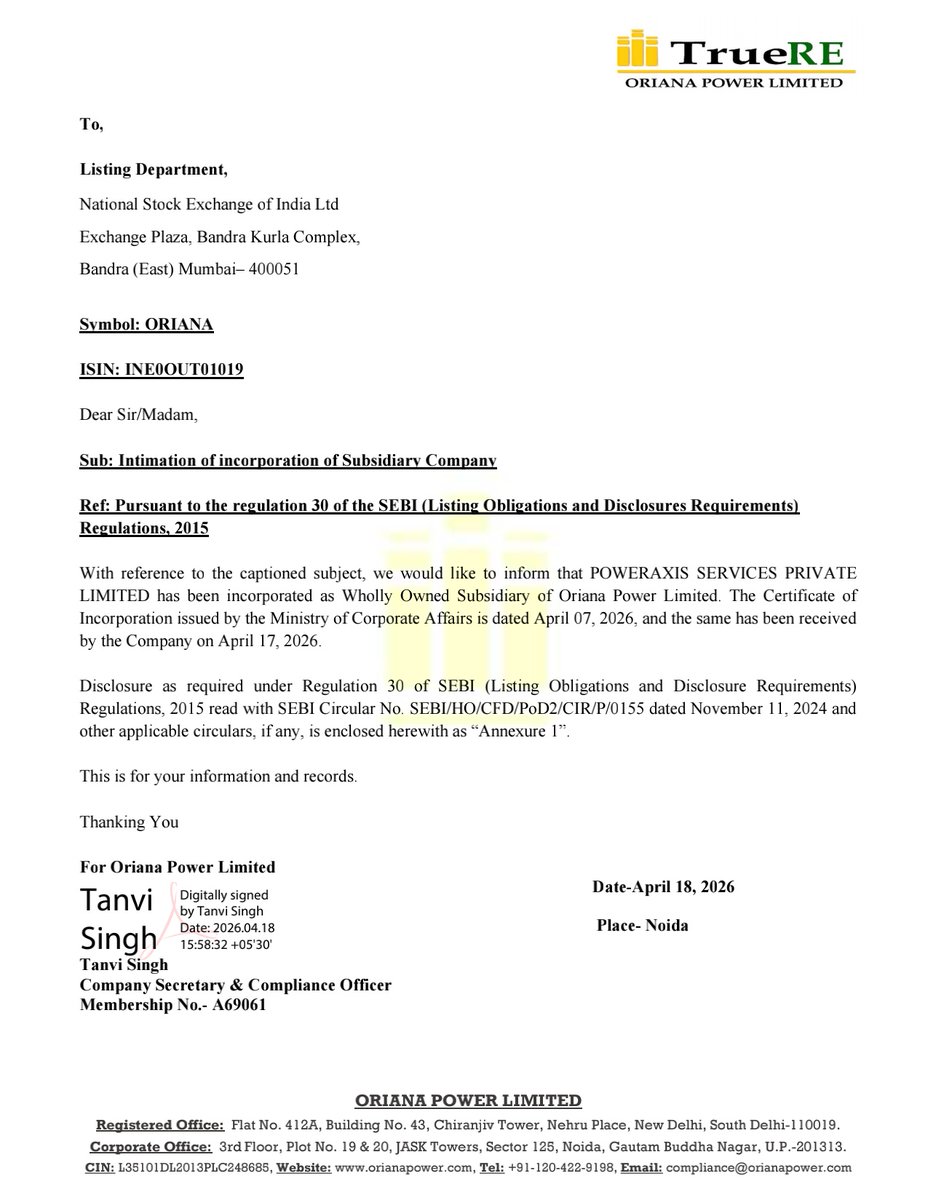

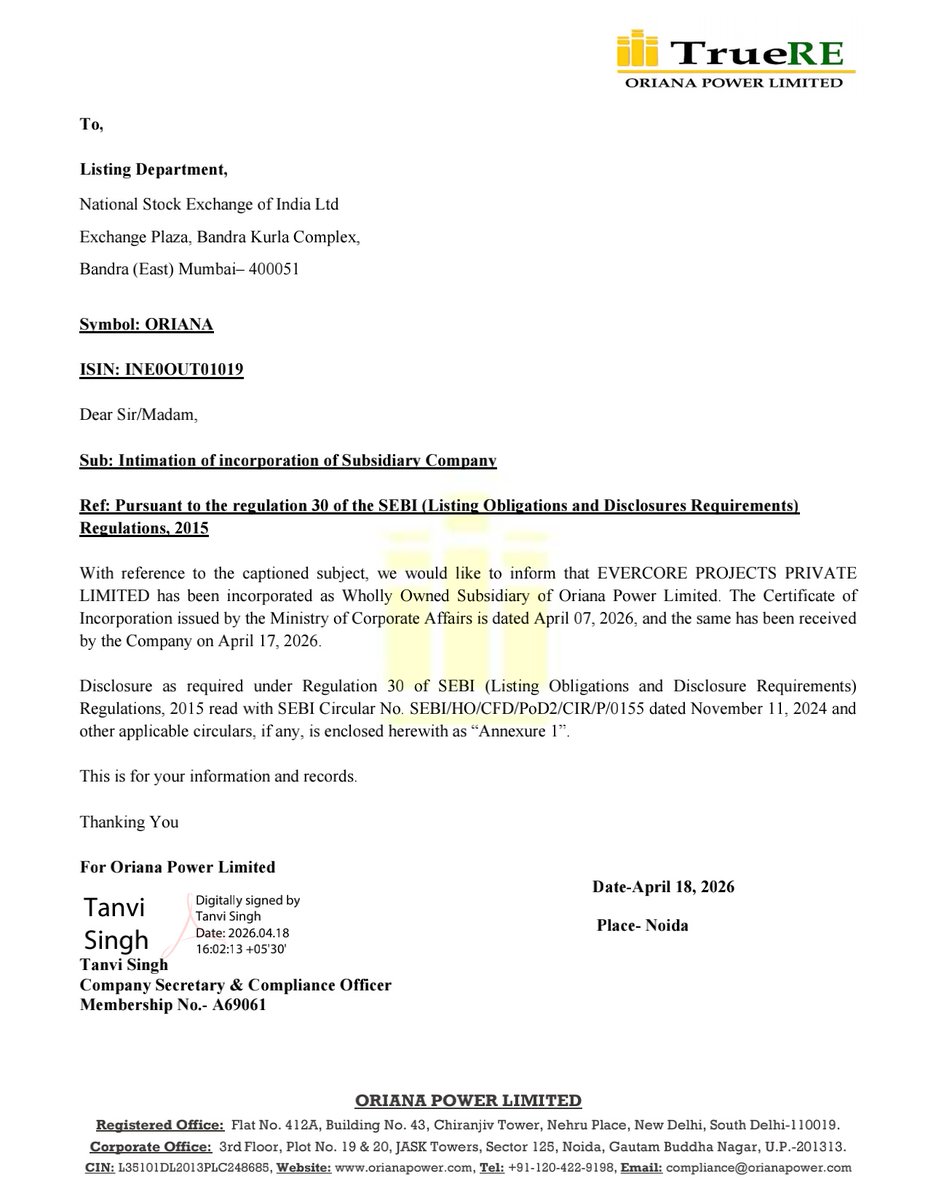

📌 Oriana Power Limited informed the exchange that COREGRID PROJECTS PRIVATE LIMITED, EVERCORE PROJECTS PRIVATE LIMITED, POWERAXIS SERVICES PRIVATE LIMITED, BLUEPLANET ENERGY PRIVATE LIMITED and NOVAGRID ENERGY PRIVATE LIMITED have been incorporated as Wholly Owned Subsidiary of Oriana Power Limited. The Certificate of Incorporation issued by the Ministry of Corporate Affairs is dated April 07, 2026, and the same has been received by the Company on April 17, 2026. #SME #ORIANA ⚡🏭

English

Venkatram retweetet

Venkatram retweetet

The @mps_taurian Mobistack TC 2090 continues to support efficient stockpile formation with controlled material flow—enabling smoother operations, reduced handling, and sustained productivity on site.

#TaurianMPS #Mobistack #MaterialHandling #Stockpiling #Mining #Aggregates #Site

English

Venkatram retweetet

Beezaasan : Scuttlebutt analysis : Quietly building defence capabilities

As per one of its peer, Beezaasan is also in the race to get defence licence for RDX, HMX, TNT, Propellent etc. They seem to have already applied for all these licences. The peer also mentioned that it takes 18-24 months from the grant of licence to start production.

Last year as per IPO discussions by the management of Beezaasan, their sister company Asawara Earthtech Ltd. had all the defence licenses for production of RDX, HMX, TNT and other products. Recently, Beezaasan acquired 35% stake in this company from promoters. Considering, this company already had defence licences more than a year ago, we expect this company to start the production of defence explosives at the end of FY27 (18-24 months from the grant of licence). Beezaasan's own defence explosive licences might take another two years.

Most of the money raised via Beezaasan's IPO would have already been deployed as per the schedule of capex as per DRHP. This expanded capacity should also come on-line during FY27.

What all this mean for earnings expectations?

1. Considering new expansion is going to be complete in FY27, FY26 could remain largely muted vs FY25.

2. FY27 : Would see completion of expansion at Beezaasan, may be start of production of defence explosives at 35% owned Asawara Tech. As per Asawara company's valuation report (at the time of preferential issue), Asawara could have a PAT of 58cr in FY27 and 120cr in FY28. Beezaasan's share i.e. 35% of this would be Rs. 20cr and 42cr, respectively.

Conservatively, Beezaasan can have a PAT of Rs. 16-25cr, conservatively, assuming delay in start of production at Asawara and may be Beezaasan's expanded capacity as well. If executed well, Beezaasan consolidated PAT could be Rs. 30-40cr in FY27, itself. Better to remain conservative.

3. FY28 : Could see a substantial jump in earnings due to full year of operations at Beezaasan and Asawara new capacity. The PAT could grow to Rs. 40-60cr in FY28 for Beezaasan.

4. FY29 : Could be a big year as the expanded capacity gets scaled up and Beezaasan own defence capacities comes into operation. Conservatively, Beezaasan could have Rs. 100cr PAT. All depends upon execution. FY30 can surprise considering all the defence explosive capacities at Beezaasan and Aswara could be fully operational.

Current market cap is Rs. 300cr.

Defence explosives is a highly regulated industry and trades at higher valuation multiples.

Only for long-term investors with patience.

Do your own due-diligence.

English

Venkatram retweetet

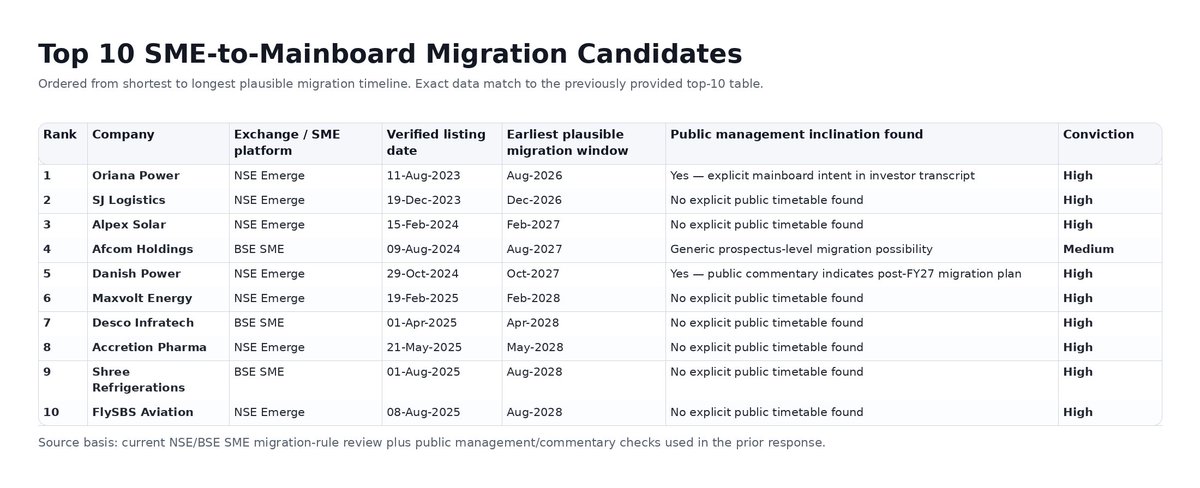

Multiple popular and well performing SME listed companies going into mainboard in next 6-18 months.

Most of these companies trading upto 50% discount to their mainboard peers due to lack of liquidity in this mini world.

Migration might help them get fairer valuation and that will give both companies and investors in SME much needed incentives and motivation.

Rahul Kumar Das@Rahul_Invest

Look out for SME companies migrating to the mainboard within the next 6-8 months. There is potential for massive value unlocking..

English

Venkatram retweetet

@Sanace1010 Yes this I have heard on the street. I just track close to 2% which means there will atleast be a dozen or so set for this yr which i am not tracking.

English

@AnirbanManna10 Was tentative but the war and png push might do the trick. We might get a good suprise here. Management is coming quickly with the audited results which usually is a good sign.

English

@srir54 Is 100% CAGR guidance possible for Desco infra?

Seems street does not have trust on the Management

Giving my unbiased view

English

Venkatram retweetet

#accretionpharma #accpl Latest cap table for the interested.

Venkatram@srir54

#accretionpharma #accpl is shaping up as an export-led SME CDMO with owned manufacturing, multi-country approvals and improving scale. The key monitor now is execution: product registrations converting into direct exports, better mix, margin recovery and tighter working capital.

English

Venkatram retweetet

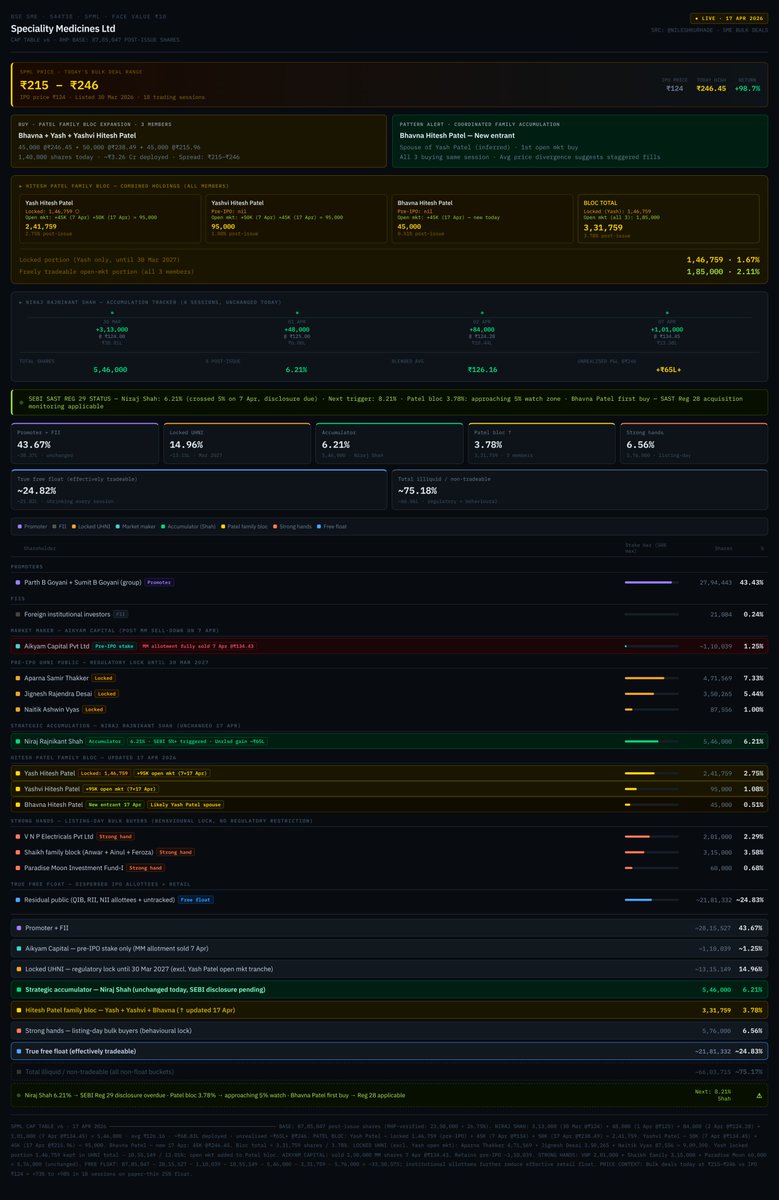

#spml hitesh patel family in full on buy mode the conviction is heartening for us investors. #scml more support offered to prevent stock from going below 80

Nilesh Kurhade@nileshkurhade

SME BULK DEALS on 17/04/2026 🇳 • ACCORD • Accord Synergy Limited 🟩 • AFZAL AIYUB PATEL • BUY • 20,000 SHARES • ₹38.15 🟥 • AGAM RAHUL SHAH • SELL • 24,000 SHARES • ₹38.15 🟩 • PRAGNYESHBHAI BHARATBHAI PATEL • BUY • 20,000 SHARES • ₹38.15 🟥 • RAHUL SHAH • SELL • 20,000 SHARES • ₹38.15 🟩 • SARFARAZ YAKUB PATEL • BUY • 20,000 SHARES • ₹38.15 🇳 • KRMAYURVED • KRM Ayurveda Limited 🟩 • AFFLUENCE GEMS PRIVATELIMITED • BUY • 2,00,000 SHARES • ₹236.00 🟥 • MANSI SHARE AND STOCK BROKING PRIVATE LIMITED • SELL • 2,02,000 SHARES • ₹235.97 🇳 • KANDARP • Kandarp Dg Smart Bpo Ltd 🟩 • ALTIZEN VENTURES LLP • BUY • 1,01,000 SHARES • ₹141.21 🇧 • 543540 • PGCRL • Pearl Green Clubs and Resorts Ltd 🟩 • GULRAJ LAKSHMANDAS CHANDARAM RAHEJA • BUY • 16,200 SHARES • ₹129.68 🇧 • 543285 • RCAN • Rajeshwari Cans Ltd 🟩 • PHOOLWATI JAIN • BUY • 69,600 SHARES • ₹17.07 🇧 • 544746 • SCDL • Safety Controls & Devices Ltd 🟩 • DEALMONEY COMMODITIES PRIVATE LIMITED • BUY • 115,200 SHARES • ₹81.22 🇳 • SAIFL • Sameera Agro And Infra L 🟥 • SATYA MURTHY SIVALENKA • SELL • 2,60,000 SHARES • ₹10.98 🇳 • SPEB • Speb Adhesives Limited 🟥 • COMPACT STRUCTURE FUND • SELL • 1,78,000 SHARES • ₹55.70 🟩 • POOJA SHALIN JHAVERI • BUY • 1,78,000 SHARES • ₹55.70 🇧 • 544738 • SPML • Speciality Medicines Ltd 🟩 • BHAVNA HITESH PATEL • BUY • 45,000 SHARES • ₹246.45 🟩 • YASH HITESH PATEL • BUY • 50,000 SHARES • ₹238.49 🟩 • YASHVI HITESH PATEL • BUY • 45,000 SHARES • ₹215.96

English

Venkatram retweetet

@DrBhavin6 He can be, that is not an issue as long as the company delivers on the numbers and quality of earnings things look good. Each promoter has his personality. It might benefit at some point. Dhirubhai was called so which I remember from rel petro ipo times.

English

@srir54 Well, time will tell . Only one problem is the Promoter looks self obsessed. The day he came on the business news channel at stock price around 700, the downfall started. The brand should be above the man. Reminder me of Mr. A appeared on India TV and the rest is the history

English