Angehefteter Tweet

写了一篇关于美债,赤字,稳定币和DeFi的文章

未来3-5年将会是美债继续泡沫化的一段时期,区块链技术使美债的购买群体从机构间接转为个人。

全世界都会成为美债的承销商,能帮美政府承销美债的生意都是好生意!

> 属于美债承销商的4年:timzz.substack.com/p/401

中文

timzz

1.3K posts

@timzz_sleep

Record & feedback | contributing to ⚡️@sparkdotfi | writings at https://t.co/MqdOaznih7

A milestone for @Ethereum in Asia. Sharplink is honored to partner with @VitalikButerin, @ethereumfndn, and @SNZHoldings in the launch of the Ethereum Community Hub in Hong Kong, the first in the region. Hong Kong's digital asset ecosystem is maturing rapidly, and Ethereum is at the center of what comes next.

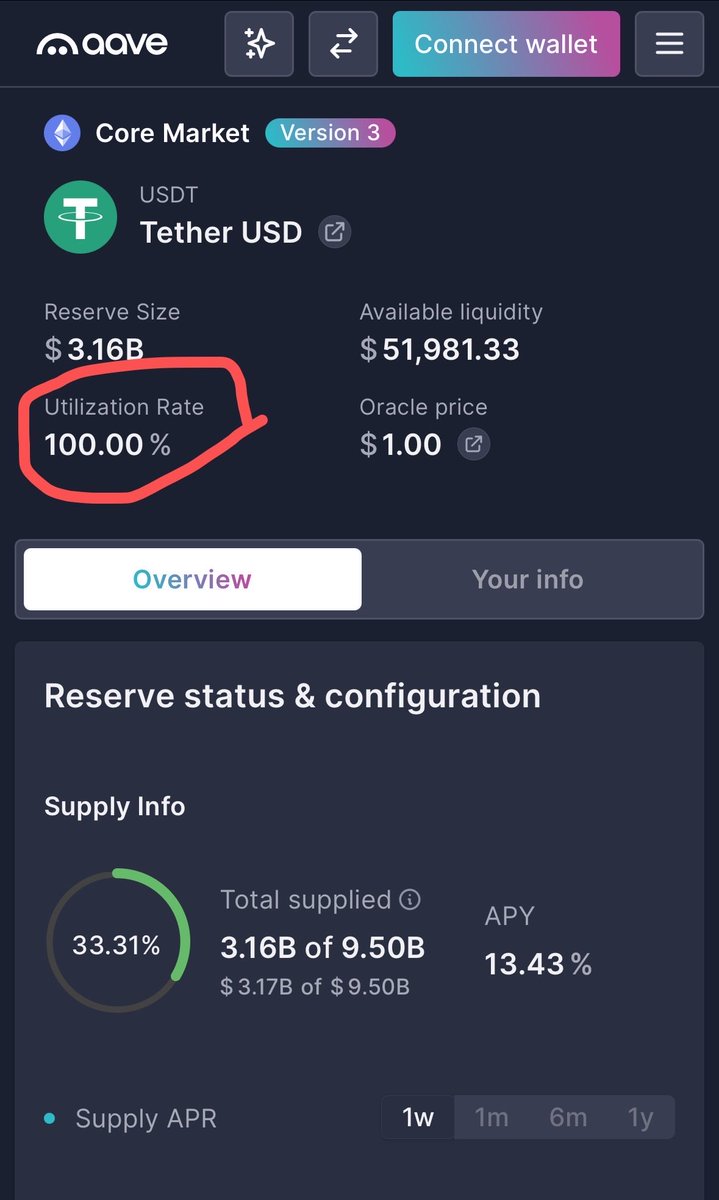

Aave 上的资金还在持续流出,3 天半的时间已经流出了 $151 亿:总存款量从出事前的 $485 亿到现在的 $307 亿,差不多是跑了三分之一的资金。 另两家主流借贷平台的情况 ◎Morpho:总存款量从 rsETH 事件前的 $117 亿到现在的 $102 亿,跑了 $15 亿资金。 ◎Spark:SparkLend 业务 TVL 从 rsETH 事件前的 $19 亿到现在的 $32 亿,进来了 $13 亿资金。 Spark 吸纳了部分巨鲸/机构 (例如孙哥还有 2 月份 $5 亿资金抄底的那个巨鲸等) 从 Aave 撤出的资金。 ---------------------------------------------------- #Bitget VIP 费率更低,福利更狠!买美股秒级入场

截至目前为止,AAVE已经撤资达到66亿美元,不止主网,多个L2和EVM网络上部署的AAVE借贷池的USDT和USDC均被挤兑一空,存借利率均飙升15%以上。 水友们都在纳闷这样下去AAVE不是自己砸自己招牌呢?应该马上解决啊,又不是赔不起。 主任揣测Aave 尴尬在于不能喊兜底,喊了跟另外两家L0和KelpDAO 就没法谈判如何分摊用户损失了。要是AAVE自家问题, Stani早都喊兜底安抚用户劝阻用户疯狂提现的恶性循环了。 但迟迟不喊兜底又持续被用户挤兑,Defi生态进一步瓦解。要主任说,这时候就应该看V神居中协调了,平常以太神教大旗挥舞,这时候不能再做缩头乌龟了,要肩负起领袖的责任来!

KelperDAO因为在L0的DVN验证人只有1/1被攻破,导致以太坊主网L0桥上被盗出约2.8亿美金的rseth,在没有流动性跑路的情况下,黑客将rseth存入aave, compound等借贷协议,借走真金白银weth,导致这些协议出现资金窟窿。 目前AAVE预估窟窿在1亿美金以上,安全基金(Umbrella)只有5600万美金不足以100%覆盖。目前AAVE ETH和Arbitrum的ETH利用率都达到了100%,无法提出任何ETH资产。 目前USDT USDC等主流资产仍然有流动性能够提出,但考虑到协议有资金窟窿,如果用户都提出资金挤兑的话,最后总会有一部分钱出不来。 如果事情得不到官方处理,ETH存款用户通过借出其它主流资产先提走一部分资产。在这个博弈下,有其它资产存款的用户能跑先跑,目前估计很多亚洲用户还没反应过来,随后就会参与到对aave的挤兑行动中。 官方通过增发AAVE拍卖卖币解决资金窟窿也许是一个比较实际的解决方案参考当年MakerDAO的例子。 这次黑客事件对Defi协议安全性信心的打击是非常严重的,直接触及了整个领域最核心的基础设施,主任非常痛心,不知道又要多久才能恢复…

Spark Savings spUSDT is the ONLY liquid defi deposit for USDT Aave Core: illiquid for past 2 days (and potential bad debt for rsETH hack) Morpho: currently all major vaults/markets are at 100% utilization @sparkdotfi Savings: >$400 million in instantly available liquidity

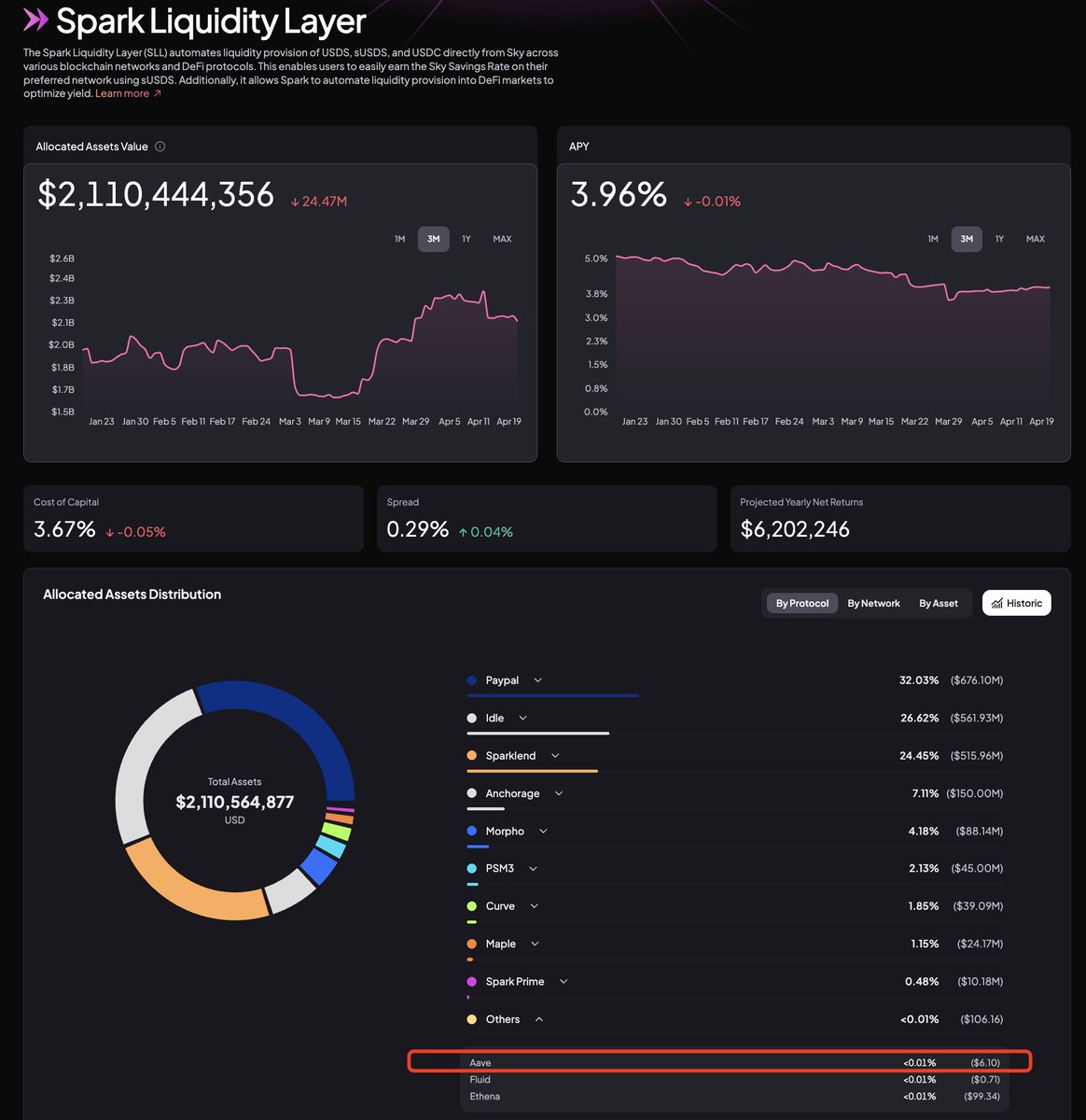

重大更新: 根据借贷市场的需求和资产风控模型,Sparklend 将逐步移除移除对 [Gnosis Market] 市场的支持,以及对 [$ezETH],[$rsETH],[$tBTC] 作为抵押物的支持, 阶段1设置具体如下: 1)[Gnosis Market] - 不再支持新借贷仓位的建立 - Reserve factor 设置成为50% 2)[$ezETH] - 不再支持 $ezETH 作为抵押物借贷仓位的建立 3)[$rsETH] - 不再支持 $rsETH 作为抵押物借贷仓位的建立 4)[$tBTC] - 不再支持 $tBTC 作为抵押物借贷仓位的建立 - Reserve factor 设置成为99% 以上资产的相关情况,以及目前在Sparklend的利用率如下图1,详细数据可以参考:spark.blockanalitica.com/v1/ethereum/ma… 调整之后,Sparklend支持的合格抵押物为:[$ETH],[$wstETH],[$weETH], [$rETH],[$cbBTC],[$LBTC],详情请参考图2. 未来 @sparkdotfi 将会继续积极支持蓝筹资产,并根据风险模型和需求进行相应调整。

some great risk discourse from @LucaProsperi and @adcv_ Luca reaches the conclusion that defi lenders are significantly underpricing risk vs SOFR, while Adrian counters that defi prime repo markets have very little default risk in practice generally find myself aligned with Adrian, but with a few caveats: (1) risk for prime repo is mostly driven by fundamental rather than market risk, and (2) prime repo provides idiosyncratic advantages that can explain divergence from SOFR/risk free rate benchmarks --- first- the bulk of the risk of onchain prime repo is not from market price jump risk, but rather from technical and counterparty risks embedded in the underlying collateral assets and oracle mechanisms most blue-chip collateral in ethereum defi is either tokenized bitcoin (WBTC, cbBTC) or liquid staking tokens (wstETH, weETH). these collateral issuers have long successful track records, but they are still subject to various fundamental risks including custody/key management, smart contract integrity, business continuity/uptime, etc. additionally, repo markets depend on data integrity, smart contract security, and key management of oracle providers. probability of default/incidents across these dependencies is expected to be very low, but the potential losses incurred in a failure case can be significant (up to 100% of the exposure) looking at the most recent loss events in defi (resolv and drift), we see that they were driven by fundamental risk factors rather than market risk. as a defi lender, the primary driver of risk is these fundamental factors rather than jump risk. --- second- onchain lending has additional benefits that can explain low or even negative spreads vs risk free rates like SOFR fundamentally, i think it makes sense to assume that (most, large scale/sophisticated) market participants are prima facie rational; if they are accepting defi lending risk with yields at or below SOFR, there is probably a reasonable explanation my mental models for this are liquidity premia or convenience yield liquidity premium is the excess return that investors demand to hold assets that cannot be quickly converted to cash at low cost. for tradfi investors, prime MMFs, tbills, and other SOFR benchmarked cash equivalent assets are this asset class and we wouldnt expect them to accept a yield below this in any circumstance. but for cryptonative investors or cryptoasset service providers (think whales, hedgefunds, exchanges), the key measure of liquidity is not the speed+cost to receive cash in a bank account, but rather the speed/cost/slippage to meet their business liquidity needs, which are typically onchain/within the crypto ecosystem. taking a directional hedge-fund as an example, if they face even a 1 hour delay between the time they request redemption of a MMF and when they receive wire transfer into their exchange account, they could easily miss a 5-10% move in a volatile asset, wiping out years of "excess risk adjusted return" they might earn with tradfi SOFR linked instruments over onchain repo convenience yield, the implied return on holding inventories, is another way to look at the same benefit. if onchain actors can expect to derive meaningful benefits from having their assets closer at hand in onchain repo markets, even if the benefit is only realized infrequently, then it can be entirely rational for them to accept risk adjusted returns below SOFR on prime repo opportunities --- @sparkdotfi has placed significant effort into both elements above, mitigating fundamental risks and facilitating onchain repo's key liquidity advantages with respect to risk- in sparklend, we use redundant/aggregated price feeds across multiple providers to mitigate oracle risks, and are continuously introducing mechanism design solutions to alleviate corner cases (eg. automatically freezing borrowing when a pegged asset trades below peg). additionally, we put significant focus into fundamental research on collateral assets, with rate limits and automated cap management helping limit exposure to issuer failures with respect to liquidity/utility- Spark is laser focused on delivering high liquidity savings products that meet the needs of sophisticated crypto market participants taking the Spark Savings USDT vault as an example (app.spark.fi/savings/mainne…), we currently maintain over 700 million in available withdrawal capacity against a 885 million total vault size, or roughly 80% liquidity ratio. this far surpasses the typical liquidity available within other onchain lending markets, which already have a significant liquidity advantage for cryptonative entities vs offchain cash equivalents --- to summarize - market risk is an important consideration, but generally represents only a small factor within onchain prime repo - the larger impact on risk is from fundamental factors, which can be mitigated with a diligent approach to counterparty+collateral evaluation and technical/mechanism design solutions - the market is fundamentally (mostly) rational and delivering superior a superior onchain liquidity profile can justify residual risk exposures, even when the spread vs SOFR is low or negative