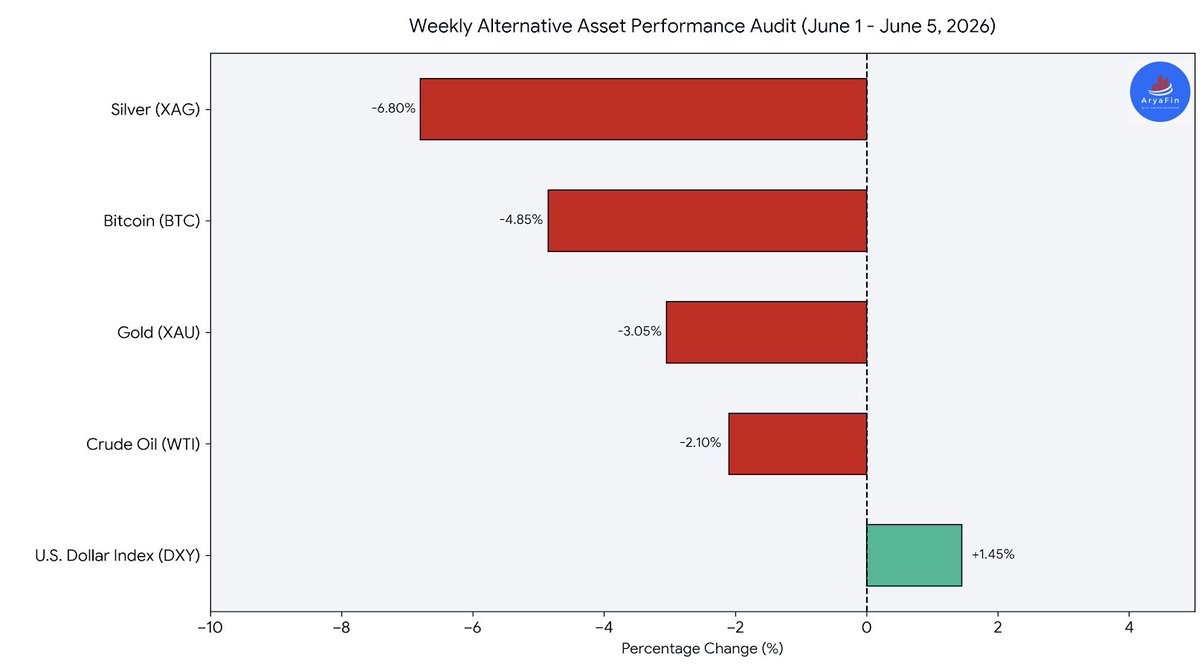

📊 Scion Asset Management Portfolio Update

Michael Burry, the contrarian manager of Scion Asset Management, disclosed that he has increased his long positions in a highly specific cluster of large, well-established businesses. Burry highlighted his investment thesis on his Substack, explaining that the broader market is heavily punishing dominant franchises with significant owner's earnings, minimal debt, and aggressive, accretive share buybacks.

According to Burry, these companies are experiencing deep valuation compression due to a massive concentration of capital into AI-adjacent names, creating distortions reminiscent of the 1999 dot-com bubble where non-internet stocks were left completely abandoned.

🔍 Deep Value Breakdown: The Four Key Additions

1. Adobe Inc. ($ADBE) 🏠The Valuation Dislocation: Down roughly 30% year-to-date, Adobe has been heavily targeted by short sellers due to extrapolated fears that generative AI competitors will disrupt its creative software monopoly.

Burry’s Core Thesis: He identifies $ADBE as a clear deep-value opportunity, explicitly pointing out that the company's gross margin rate is resting near all-time highs. The market is pricing in maximum-AI disruption scenarios that do not align with Adobe's fundamental software dominance or its actual free cash flow generation.

2. Alibaba Group ($BABA) 🇨🇳The Valuation Dislocation: Trading well off its historical highs due to Chinese regulatory adjustments, geopolitical trade pressures, and massive domestic e-commerce competition.

Burry’s Core Thesis: Burry heavily reframes the narrative, calling Alibaba "the most advanced company in China as far as AI strategy goes". He underlines that because management is aggressively buying back common stock, true intrinsic value continues to accrete to shareholders regardless of whether the short-term tape rewards it. He noted that "when the time comes, the stock will launch fast and fly high."

3. PayPal Holdings ($PYPL) 💳The Valuation Dislocation: Punished heavily over a multi-year window, down nearly 24% year-to-date due to a management turnover drag and intense payment processing headwinds from Apple Pay, Block, Stripe, and Adyen.

Burry’s Core Thesis: Burry describes the market as having "been attending PayPal’s wake for years now, though the body has yet to show". Trading at a highly compressed 7x to 8x earnings multiple, he notes that the asset is buying back stock "hand over fist" and represents a highly lucrative target for both private equity (PE) firms and strategic enterprise acquirers.

4. Veeva Systems ($VEEV) 🧪The Valuation Dislocation: Dropped nearly 29% year-to-date, hitting relative multi-year lows as localized biotech and pharmaceutical spending slowed into the credit reset.

Burry’s Core Thesis: He states that Veeva's core vertical SaaS architecture has returned to unjustifiably depressed price-to-earnings and price-to-sales ratios. He dismissed the looming competitive threat from Salesforce ($CRM) as only being relevant to a very small, isolated slice of Veeva's wider life-sciences software infrastructure.

The Strategy View: Burry is looking for structurally sound, high-cash-flow monopolies that have been completely orphaned because they aren't explicit AI hype plays. The broader the spectacle around mega-cap AI momentum swells, the wider the value discount gap grows for these compounding giants.

English