Nikolaj

1.8K posts

My take on dilution from someone who has raised millions from VCs: Dilution is not scary. It is just a tool. On X, people treat every raise like theft. Sometimes it is. Sometimes it is exactly what lets a company scale into the opportunity in front of it. In my world, VC money was basically a bridge loan of credibility until the business could prove itself. Public companies are not that different. If management raises capital at the right time, puts good dollars to work, and increases the value of the company by more than the dilution, shareholders win. If they raise badly, spend badly, or dilute to survive instead of scale, shareholders lose. So the question is not “is dilution bad?” The question is: do you trust management to turn that capital into something more valuable than the shares issued to do it. If not, you probably should not own the stock anyway.

Klingelnberg $KLIN.SW - a ticker you never heard before, but should be aware of. Especially if you’re bullish on physical AI, but find it hard to identify the future winners. The numbers reflect a legacy automotive supplier. I see the undervalued backbone of the robotics future: - 120m market cap - P/S: 0.36x - Trading below book value (P/B 0.8x) - 200+ active patents Every humanoid robot requires C3-precision gears in its joints. This finishing step is only possible through high-precision grinding. Only five companies globally can deliver this quality. Klingelnberg is a Swiss small-cap, part of this elite oligopoly Capacity is the constraint. Machines cost millions and have 24-month lead times . When robotics demand spikes, this oligopoly might become a global bottleneck. Klingelnberg integrates grinding and measuring into one automated cell. Perfect for robot OEMs who want to build actuators in-house without decades of gear-making DNA.

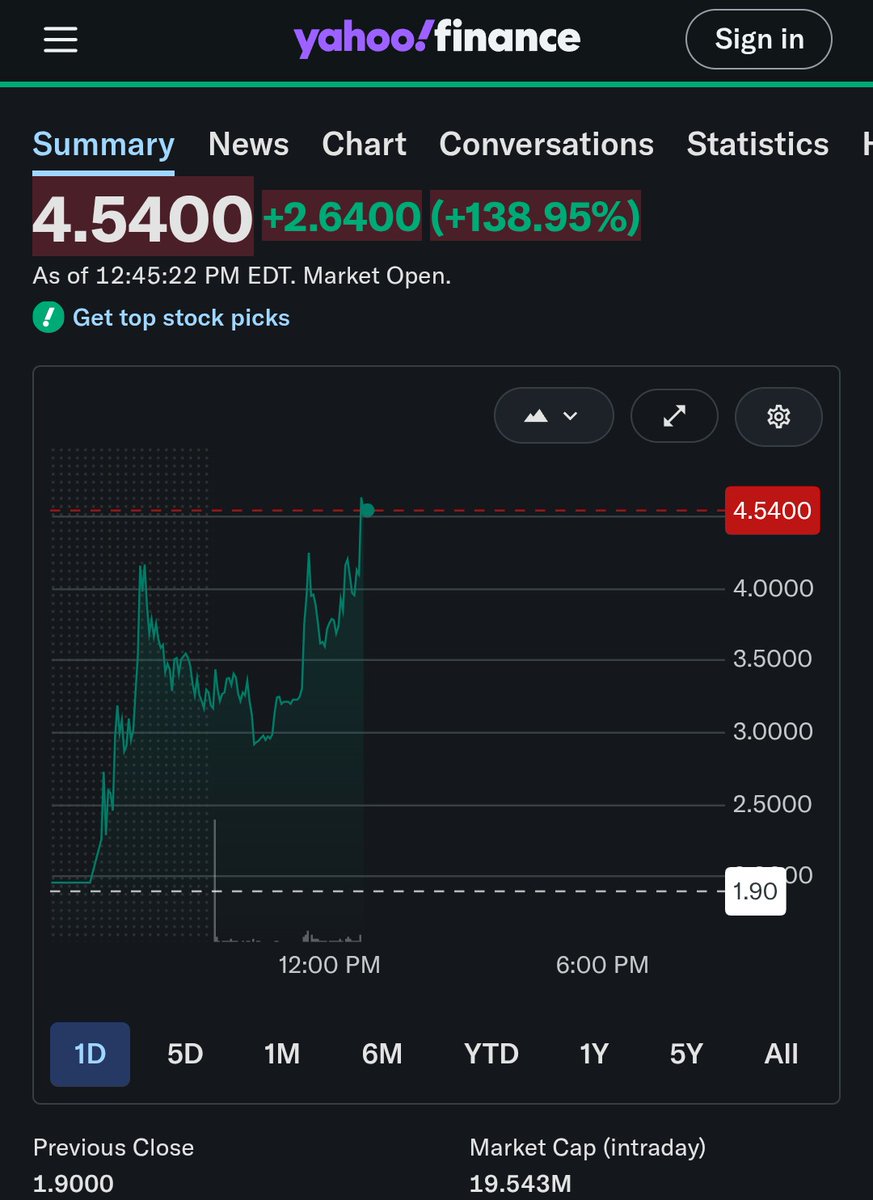

I took a position in another hidden ai data center infra play. Contract of 260mill. Payment received of 43mill, marketcap of 22mill. Heavy re rating incoming. I also added more $keel $aib $hive $shaz and $dgxx