nanocapper

423 posts

nanocapper

@nanocapper

flipping rocks in nano-caps.

Denver, CO Se unió Aralık 2020

155 Siguiendo556 Seguidores

We’re pleased to share our investment memo, which outlines our thesis and what we believe makes this business uniquely positioned for sustained growth. $CSU, $CSU.TO. Please DM for the full version.

English

Glow Lifetech $GLOW.C cleaned up its capital structure:

41M+ warrants reduced in Q1 2026

5M options (Expired unexercised)

10.9M warrants exercised

89% by insiders & long term holders

Cuts dilution 16.6% over the trailing twelve months.

“This significant reduction in our warrant and option overhang marks an important milestone for Glow… we are well-positioned to advance into our next phase of growth.” - CEO Rob Carducci

glowlifetech.com/news/glow-life…

English

@whiteoutcapital In your opinion, what is the main reason that Calnano isn't converting more R&D customers to larger manufacturing contracts?

English

California Nanotechnologies $CNO.V $CANOF - closed their private placement with ~3.12m shares issued. They offered 2.5m shares plus a 1m share over-allotment. My interpretation is that they possibly had buyers lined up for the 2.5m and left the other 1m open to shop.

There's good and bad news here. The good news is they were able to raise almost $1m when sentiment is generally poor and they've been on a losing streak operationally.

The bad news isn't too bad or surprising, but they were only able to fill 612k shares of the 1m over-allotment. So there was some interest, but not like the raise in 2023 where it was over-subscribed and many people only got 1/3 of the allocation they requested (such as myself).

This cash will hopefully help them bridge the gap to their next commercial customer(s) after abruptly losing their green steel customer about a year ago. I still don't love the raise here in a position of weakness, but at least they were able to raise at the market price and enough to sustain them for a while.

calnanocorp.com/california-nan…

English

@nanocapper hey man dm’d you to discuss a name. Not sure if you saw but hoping to connect!

English

@nitinkinvest @DMetropolitan They hired a back end developer for RaceControl and QA person. I'm pretty sure the CEO and CFO are going to earn $400k salary each.

English

@nanocapper @DMetropolitan Announced the earnings date right after the post. Also agree with the earnings sentiment! However , Don’t think SG&A is a concern but you never know with nanocaps.

English

I know most people didn’t read the SS post, so I wanted to share my thoughts on the $MSGM setup, which I believe is extremely compelling heading into 2026. Thanks to @DMetropolitan for bringing this to my attention.

I believe the set up is massively misunderstood and offers asymmetric upside. Currently trading at a market cap of roughly $20 million and essentially 1x forward sales, the market is mispricing the equity as a distressed, capital-destructive legacy gaming publisher.

The company has executed a structural turnaroundand is now completely debt-free with $4.5 million in cash reserves. Driven by the shift from physical retail sales to the high-margin RaceControl SaaS platform, gross margins have expanded to an exceptional 80.7%. Over the coming quarters, I believe, the underlying intrinsic value of this recurring revenue ecosystem will become the narrative which will drive the stock higher.

Social Arbitrage & Capturing the Competitor Vacuum

LMU is aggressively cannibalizing market share in a landscape currently defined by lackluster competition. The historical king of GT3 racing, Assetto Corsa Competizione (ACC), has been effectively abandoned by its developers in favor of Assetto Corsa Evo, a title currently facing heavy community criticism and OVERWHELMINGLY NEGATIVE rating on Steam.

Simultaneously, the reigning multiplayer titan, iRacing, continues to alienate newer players with sunk-cost fatigue, requiring hundreds of dollars just to participate. LMU is exploiting this friction well.

The games' momentum is being accelerated by major YouTube KOLs like Jimmy Broadbent and Danny Lee, who are actively redirecting their massive audiences into the MSGM ecosystem due to its superior, highly communicative tire physics and accessible pricing. The brand loyalty can also be seen from the positive comments on YouTube videos released by LMU. The development team and CEO Stephen Hood are receiving overwhelming praise for their transparency and community driven updates, proving they are actively listening to their player base.

Unprecedented Engagement & De-Risked Infrastructure

In their December 2025 press release, the company mentioned that players drove a staggering 12.5 million laps on RaceControl (608% YoY increase). That growth compounded into the new year, with Steam concurrent player peaks hitting all-time highs of 8,740 in January and 8,660 in February 2026. What makes these metrics truly explosive is that the real-world 24 Hours of Le Mans doesn't even take place until June, these numbers are strictly organic.

As MSGM continues to roll out new tracks, cars, and highly requested features like a single-player career mode, the adoption of their high-margin RaceControl Pro ($48/yr) and Pro+ ($84/yr) subscriptions will continue to scale rapidly.

This past weekend, LMU hosted stable 12-hour endurance races with complex driver swaps, the developers proved they have resolved the scaling bottlenecks that plagued the platform in the past. This was the Achilles heel of the company in 2023 and resulted in Max Verstappen getting disconnected during the 2023 virtual event which caused a lot of negative press.

Upcoming Catalysts & The Console Lottery Ticket

We are entering a compressed window of highly lucrative catalysts. The Q4 2025 earnings report will benefit from a massive deferred revenue tailwind, as the December launch of ELMS Pack 2 legally unlocked significant cash parked on the balance sheet under ASC 606 accounting standards. Q1 2026 is structurally positioned to be even stronger, leveraging all-time high player counts and aggressively optimized SaaS monetization.

Looking ahead to the summer, the June Le Mans Virtual event will most likely completely shatter existing records, driving an immense top of funnel lift for the RaceControl platform. If MSGM successfully secures commitments from massive real-world drivers to join the simulation, a strategy currently in motion according to the management, the mainstream cultural exposure could trigger a viral explosion for the game.

The sticky PC player base could also give MSGM immense leverage in their late-stage negotiations with third-party partners to fully fund the console port. Porting an already-optimized PC architecture to PlayStation and Xbox is a manageable transition that instantly unlocks a TAM multiple times larger than their current footprint. If management can smooth out the remaining minor VR bugs and penalty system friction, 2026 is destined to be a watershed year for the company.

Nitin Gupta@nitininvests

Not my idea, but one I'm really liking for earnings is $MSGM. Working on an SS post and hoping to share it this weekend, link in the bio (no paywall). Medium-risk play but could be a potential multibagger. The current quarter is shaping up to be a material turning point, as significant revenue tailwinds from the Q4 "Track and Pack" release suggest a potential blowout performance. The December 2025 update, which introduced the Paul Ricard circuit and the innovative "Team Online" feature, has acted as a massive catalyst for both high-margin DLC sales and recurring "RaceControl Pro" subscriptions. Alternative data and web traffic metrics support this narrative, showing a 126% spike in traffic between community hubs and the storefront, while traffic to the "Pro" subscription paywall has soared by 60%. This momentum has carried directly into January 2026, which saw the game hit an all-time peak of 8,740 concurrent players, a 4x increase over the previous year an This suggests to me that the market is missing a surge in deferred revenue and ARPU (Average Revenue Per User) that could make the next earnings report a landmark event for the company's valuation. The company could post revenue numbers close to $3.5M which would represent a significant QoQ growth and a material lift in the bottom line owing to the 80% margins from DLC and RaceControl Pro subscription. Motorsport Games $MSGM is a possible turnaround story with great social traction, where a company has successfully pruned its distractions and is now focusing on its high margin business. Historically, MSGM was a bloated license collector and burdened by expensive, underperforming contracts for NASCAR and IndyCar that drained cash at a rate of $2 million per month. Under the leadership of returning CEO Stephen Hood, the company has cleaned up its act materially and is divesting the NASCAR license and refocusing entirely on its crown jewel: Studio 397 and the Le Mans Ultimate (LMU) platform. The company has shrunk its footprint to a boutique team of 41 people who develop the industry-leading rFactor 2 physics engine, one $FWONK & $DBO.TO $DBOXF use for their F1 Arcades. MSGM has reduced its monthly cash burn to less than $100,000 and I believe will be cash flow positive in Q4 creating a lean foundation for a possible multi-bagger opportunity. The story today is about their pivot towards a technology centric SaaS model via the RaceControl platform. The broader market is incorrectly focused on a perceived slowdown, alternative data and social sentiment analysis from community hubs like Reddit and Discord reveal a thriving, highly engaged ecosystem. MSGM has teased a potential new game, as noted they provide the physics engine for the F1 Arcade, MSGM has established a strategic moat that could realistically lead to a full-scale F1 simulation title in the future. This is currently ignored by Wall Street, yet it provides a free lottery ticket on future high-profile developments. In the near term, the return of the Le Mans Virtual championship serves as a material catalyst, likely driving peak user numbers and lucrative sponsorships that will lift ARPU. Finally, the most significant catalyst is the impending console port for PS5 and Xbox. Management is in late-stage negotiations with a funding partner to foot the entire bill for development, effectively eliminating MSGM’s financial risk while opening the door to a user base 4X larger than the current PC market. With growing deferred revenue and material catalysts in the current quarter, the market’s pessimistic view of MSGM is a textbook mispricing. MSGM offers the rare combination of a "boring" niche business, a proven tech moat, and massive multi-platform growth potential that is currently underfollowed by the institutional crowd.

English

@TrentBlair19 Are they just the middlemen in shipping server parts?

English

$RCHN $14 million market cap company trading at 7x cash flow shipped 8.3 tons of computing components to an AI company. Really big news.

Liger Cub@realLigerCub

FWIW, $RCHN shipped ~8.3 tons of computing components to Tenstorrent AI in Nov-Dec 2025.

English

@nitinkinvest Sounds good. A lot of filings today with Mike Zoi's plan of selling all his class A shares and the $3 million revolving loan announced today.

English

@nanocapper Thanks for mentioning that. I'll send you a DM if I have any further questions, since you seem well versed with the story. 😀

English

@whiteoutcapital What do you think about calnano raising $$$? More dilution + warrants.

English

Valuing Cal Nano is challenging right now.

Backward-looking valuations are murky. Forward-looking valuations are speculative.

From a qualitative perspective, I think their network and reputation are under-valued and under-monetized. Some of the most cutting edge technology companies are hiring Cal Nano to R&D their most critical components.

Their relationship with top material science researchers at universities and national labs is not something that could be easily replicated.

The current financials don’t provide much support for valuation today (which I’d speculate is part of why the share price has struggled), but given these qualitative factors, the current $10.4m market cap feels low to me. I’ve been actively purchasing shares for the first time since 2023.

How is everyone else thinking about the current setup?

$CNO.V $CANOF

I own shares. Not investment advice. See full legal disclaimer on website.

English

@hughieforbes @TrentBlair19 Any way to get access to the expert markets for non high worth investors?

English

I find many very illiquid liquidations on the OTC. If you can get a fill, then you can make some nice low risk returns. The paradox is you often need expert market access.

Dirtcheapstocks@dirtcheapstocks

If I had $100,000 I'd do this: - Read every filing. - Arb odd lot tenders, new releases, liquidations, etc. - Own 2-3 tiny companies trading at ~3x earnings and less than net cash. I bet a smart person could do ~50% CAGR. Issue is it takes all your time. Not investment advice.

English

Somehow I missed that Cal Nano got their first analyst last Oct.

They have a price target of $1 for $CANOF (translates to C$1.39 for $CNO.V). Target was maintained after last quarter’s miss.

Analyst is Tate Sullivan if you’d like the report: tsullivan@maximgrp.com

English

@whiteoutcapital Did not expect that much revenue drop and net loss. It's been painful holding canof.

English

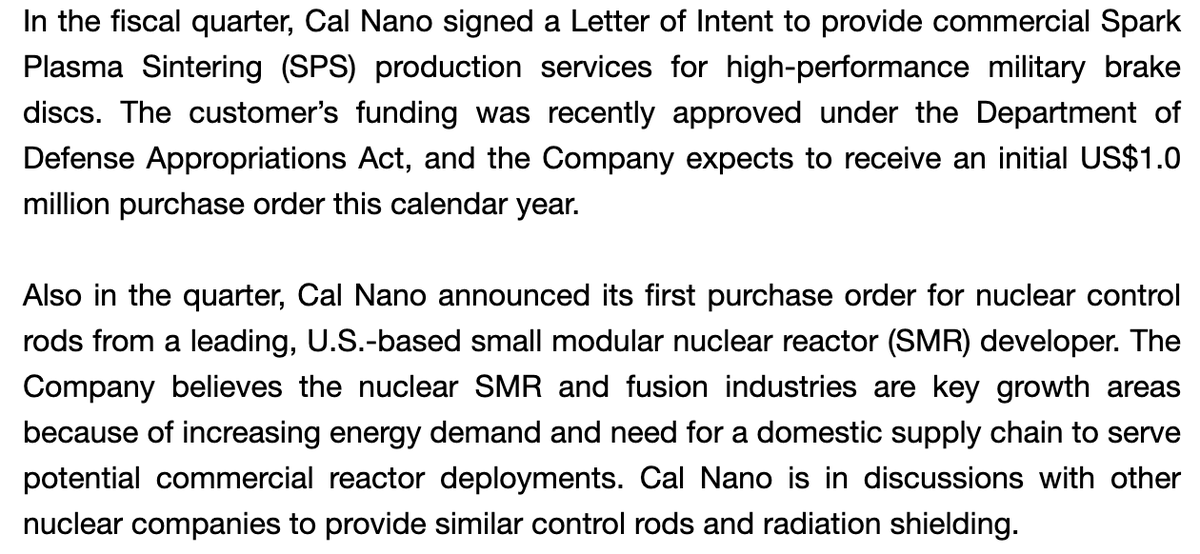

$CNO.V - $1m military brakes order expected in 2026. In reference to their first nuclear control rod order, "Cal Nano is in discussions with other nuclear companies to provide similar control rods and radiation shielding."

English

$GLOW.C enters Canada’s medical cannabis channel 🌿

Glow Lifetech launches its MOD™ & .decimal™ portfolio on Mendo Medical, its first formal entry into the medical channel, expanding access for registered patients nationwide (including veterans) 🇨🇦

✅ Full portfolio: 14 SKUs

✅ Focus on consistency + dose-control + personalization

✅ Adds a new channel alongside provincial retail distribution

A meaningful commercial milestone heading into 2026 📈

GLOW.CN

Source: Newsfile “Glow Lifetech Expands into Medical Cannabis Channel with National Launch on Mendo Medical” (Jan 7, 2026)

English

My goal with these interviews is to dive deeper into the industry, science, competition, etc. rather than focus on specific developments at Cal Nano.

English

Yesterday I published my first interview in what I plan to be a series of industry expert interviews for California Nanotechnologies $CNO.V.

What are people you'd be interested in hearing from or questions you'd like answers to?

The goal is to interview people other than Eric.

Whiteout Capital (Zack)@whiteoutcapital

Most people have never heard of spark plasma sintering (SPS), but it’s quietly enabling breakthroughs in aerospace, defense, semiconductors, energy, and beyond. I just published an interview with someone who’s been on the front lines of its evolution.

English

@ragingbullcap @TrentBlair19 Love me some share buybacks at these prices.

English

@whiteoutcapital Maybe it was just me, but the narrative from Eric sounded like the goal was to get them from r&d to a production contract. Thanks for the reply, hope they can start growing their revenue soon.

English

My understanding is that the green steel company was never going to do a commercial contract. They communicated from the start that they wanted to use Cal Nano as an R&D partner and move the process in-house once they met performance requirements.

With that said, the green steel industry is in flux right now. The Trump administration, DOGE, tariffs, etc. have upended a lot of what they were working on and my read is that they are taking a conservative approach until they understand the new rules of the game. Last I talked with Eric, they are still a customer, just at a lower volume. Could return any day to previous R&D levels, or leave for good, really hard to say.

I think Cal Nano has a lot of opportunities beyond just the green steel company.

English

Most people have never heard of spark plasma sintering (SPS), but it’s quietly enabling breakthroughs in aerospace, defense, semiconductors, energy, and beyond.

I just published an interview with someone who’s been on the front lines of its evolution.

English

@whiteoutcapital Any progress on getting the green steel customer on a production contract?

English

This is the first in a series of expert interviews I’m publishing on FAST/SPS and Cal Nano’s role in the broader materials science landscape.

I don't post full articles here, but you can read the interview and other $CNO.V content here:

whiteout.substack.com/p/update-23-ex…

English

@2t_investing Mgmt is busy using the extra space at their new facility for a ping pong table and game room (for real)

English

Is $Calnano going BK? Maybe a business update / communcation to inform investors about current state of affairs and stop the relentless bleeding? Your current MC is shameful tbh... $CNO.V $CANOF

English

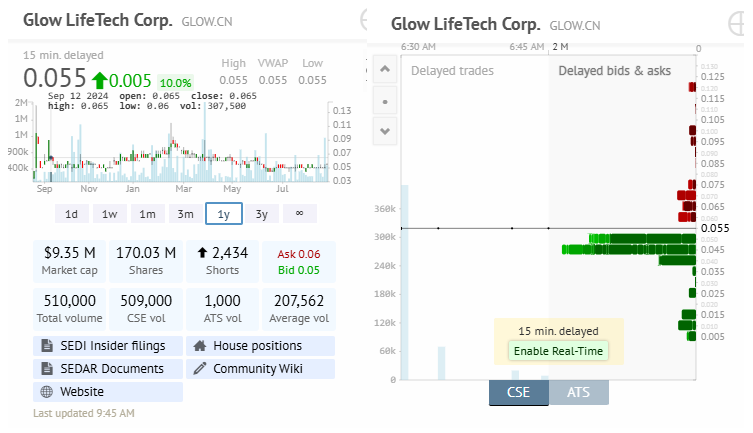

Glow Lifetech $GLOW.CN news seems to have cleared the ask at $0.055.

I wonder if the anon seller done, or will they hit $0.06?

$GLOW.C $GLWLF

JGGCDN@JGGCDN

Glow Lifetech Expands Ontario Distribution with MOD Launch in 100+ FIKA Company Stores, One of Canada's Largest Cannabis Retailers $GLOW.C $GLWLF $GLOW.CN stockhouse.com/news/press-rel…

English