The United States government is $36 trillion in debt and the currency hasn't collapsed. Every economics textbook says that's impossible.

The reason it hasn't happened is a deal cut in 1974 that most Americans have never heard of.

The USA promised Saudi Arabia unlimited military protection. In exchange, the Saudis agreed to sell every barrel of oil on earth in US dollars ONLY.

Overnight, every country on the planet became a forced buyer of American currency...

That artificial demand has subsidized your mortgage rate, inflated your stock portfolio, and funded two decades of American wars. All without a single vote from any citizen in any country.

For the first time since 1974, the system is cracking. And the investors who understand what's happening are positioning right now while everyone else doesn't even know what the petrodollar is.

And right now it's creating one of the best asymmetric investment setups of the decade.

I've talked to institutional allocators who build their entire macro thesis around petrodollar flows. Meanwhile most retail investors couldn't define the term if you asked them. That mismatch between who understands the system and who's blindly riding it is where the real asymmetry lives.

Every oil-importing country on earth is forced to accumulate US dollars before they can buy energy. Those excess dollars get parked in US Treasury bonds. Trillions per year, flowing into American government debt, not because it's the best investment, but because the system requires it. That forced demand is what lets the US borrow at rates no other nation gets. Cheap government borrowing pushes capital into stocks, real estate, risk assets. The entire post-1970s US bull market has petrodollar fingerprints on it.

If you've ever wondered why US equities have outperformed every other market for fifty straight years, this is a massive part of the answer. And if you've never factored it into your portfolio thesis, you've been investing on top of a system you don't understand.

That matters now because the system is fracturing for the first time.

Saudi Arabia, the country that started the whole system, is openly discussing pricing oil in other currencies. China and Russia are settling trades in yuan and rubles. India is paying for Russian crude in rupees. The dollar's share of global reserves dropped from 72% to 57%, the lowest since 1994. Central banks are dumping dollars for physical gold at the fastest pace since the 1960s.

When central bankers swap their own paper for metal, they're showing you exactly where they think this ends.

Understanding this actually gives you an edge over the vast majority of market participants, and the reason is simple: timing.

Most people will read about dedollarization in a headline three years from now and panic sell. The institutional money is already repositioning. The difference between those two groups, the ones who see it coming and the ones who react after the fact, is the difference between compounding wealth through a transition and giving it back.

Every major currency regime shift in the last century created a massive wealth transfer. When the gold standard ended in 1971, investors holding gold went from $35 to $850 per ounce over the next decade. When the Asian currency crisis hit in 1997, investors positioned in dollars beforehand captured 40-60% discounts on Asian assets. The investors who understood the system change BEFORE it showed up in prices made fortunes. The ones who read about it in the newspaper lost them.

The same playbook applies now.

Gold and miners. Central banks are front-running this trade right now. Gold went from $1,800 to over $5,100 in three years. The miners (GDX) are still trading at one of the widest discounts to spot gold in two decades. When that discount has compressed historically, GDX doubled within 18 months. The gold price reflects the macro fear. The miner discount reflects the fact that retail hasn't connected the dots yet. That gap is the opportunity.

Commodities. Oil, copper, uranium, agriculture. All priced in dollars. A weaker dollar pushes commodity prices higher in dollar terms even without a supply change. Freeport-McMoRan (FCX) mines the copper that every AI data center and electrical grid expansion requires. Cameco (CCJ) produces the uranium that 34 countries just pledged to triple capacity for. These aren't speculative. They're structural demand stories priced in a weakening currency.

Short-duration over long-duration bonds. BIL pays 4.5% with zero duration risk. Buffett is parking $344 billion here. If fewer foreign governments buy Treasuries and the $28 trillion refinancing wall forces higher yields, long bonds get destroyed. Anyone still holding TLT is on the wrong side of this trade. Stay short on the curve and you earn yield while keeping dry powder for the dislocations ahead.

Energy independence plays. Countries breaking free from the petrodollar need domestic energy before they can stop accumulating dollars. Nuclear, LNG infrastructure, battery storage. Every nation trying to ditch the dollar has to solve its own power supply first, and they're all scrambling to do it at the same time. The companies building that infrastructure are sitting at the intersection of the two biggest macro trends of the next twenty years: dedollarization and the energy transition.

The investors I respect most are the ones who understand which macro forces are driving capital flows across entire sectors, and position themselves in the path of that money before it arrives. That's the difference between trading and investing.

Most retail investors will read this, find it interesting, and go right back to picking stocks off a newsletter. The ones who actually build wealth through macro shifts like this have a framework for translating what they understand into positions.

That's what I teach in my free weekly session. Signup in bio

Margin is key 💎

High net profit margins are not just numbers, they are a signal of a dominant business model

Here are 20 Margin Kings every investor needs to know

🇺🇸💻 Applovin $APP 65.5%

🇺🇸💹 CME $CME 59.7%

🇺🇸🏭 NVidia $NVDA 54.3%

🇺🇸💳 Visa $V 54.3%

🇺🇸💰 Blackstone $BX 51.3%

🇺🇸🛡️ Verisign $VRSN 49.7%

🇸🇪🎰 Evolution $EVO 48.7%

🇺🇸💳 Mastercard $MA 48.6%

🇳🇱💰 Adyen $ADYEN 43.1%

🇺🇸🛡️ Palantir $PLTR 40.6%

🇺🇸💰 MSCI $MSCI 39.9%

🇺🇸💻 Microsoft $MSFT 39.0%

🇺🇸🏭 Broadcom $AVGO 38.6%

🇺🇸💉 Eli Lilly $LLY 37.0%

🇺🇸💰 Fair Isaac $FICO 34.6%

🇺🇸💹 Intercontinental Ex. $ICE 33.9%

🇺🇸💰 Moody's $MCO 32.9%

🇩🇰💉 Novo Nordisk $NVO 32.8%

🇺🇸💰 Blackrock $BLK 30.8%

🇳🇱🏭 ASML $ASML 30.1%

Foreign Capital May Not Return Soon: Protect Your Downside

1. 85% of India's capital outflows going to: Korea, Taiwan, China

2. Their 2026 Forward Earnings: 2X/3X of India

3. Their AI/Semicon Growth Supercycle vs. India’s IT Slump

4. Rupee fall erodes FII/FDI capital

DATA:

Where Is the Money Going?

a. Over ₹1 lakh crore FII capital exited India in 2026 (YTD).

b. 60% to Korea & Taiwan: AI/Semiconductor supply chain stocks

c. 25% to China: Bottom-fishing in undervalued tech stocks

d. 15% to “Safe Havens”: U.S. Treasuries and Gold

2025 Actual Earnings Growth

India (Nifty 50): 8.1%

Korea (Kospi): 76%

Taiwan (TWSE): 27%

China (CSI 300): 12%

2026 Earnings Growth (Est.)

India (Nifty 50): 9%

Korea (Kospi): 130%

Taiwan (TWSE): 22%

China (CSI 300): 13%

NOTE: Estimates are from Goldman Sachs, JP Morgan, Morgan Stanley, Bernstein reports.

2026 Forward P/E Comparison

India (Nifty 50): 18.1x

Korea (Kospi): 8.8x

Taiwan (TWSE): 19.7x

China (CSI 300): 13.9x

NOTES:

a. Even after the recent sell-off, India still remains one of the most expensive markets in Asia.

b. Korea has seen an earnings explosion in memory chips, but that market still offers deep value to investors at 8.8x forward P/E.

c. Taiwan is getting expensive, but AI/Semiconductor dominance of Taiwanese companies and TSMC’s pricing power is still a great attraction. Estimated earnings growth of Taiwan in 2026 is 2.5x of India.

d. China is no longer at “distressed” price levels of 2024, but it is still fundamentally 25% cheaper than India.

P/B Ratios March 2026

India (Nifty 50): 3.14x

Korea (Kospi): 0.90x

Taiwan (TWSE): 2.2x

China (CSI 300): 1.45x

NOTE: India is the world’s most expensive major market on P/B ratio basis. India’s price-to-book is 1.5x of Taiwan, 2.5x of China, and 3.5x of Korea. In other words, it is 3.5 times more expensive than Korea for every unit of net asset value as of March 2026.

KOREA

a. Landmark domestic corporate governance reforms combined with a global semiconductor growth supercycle have created a rare “double-alpha” opportunity for investors.

b. A stunning 130% earnings growth projected for KOSPI in 2026, led by Samsung and SK Hynix.

c. Korea’s forward P/E of 8.8x is half the valuation of Indian large caps as of today.

TAIWAN

a. Investors are moving away from AI software/LLM builders to AI hardware (semiconductors and server infrastructure) where Taiwan dominates.

b. TSMC alone controls 70% of the market share, with gross margins of 62%.

c. Taiwan 50 Index with an estimated earnings growth of 22% at a PEG ratio of just 0.9x makes it twice as attractive as Indian large caps on a growth-adjusted basis.

CHINA

a. China’s industrial output in Jan-Feb, 2026 jumped by 6.3%, beating estimates by far.

b. High-tech FDI increased by 20.4% following the government’s massive consumption stimulus package in late 2025.

c. As of March 2026, MSCI China trades at a forward P/E 11.9x, representing 48% discount compared to MSCI India’s 23x. This 48% valuation gap is at a decade-high, leading to an FII pivot towards China. (Foreign investors use MSCI benchmarks.)

INDIA

a. With 85% dependency on oil imports, current account deficit (CAD) widening, rupee getting weaker, and no tech exports hedge, India presents an asymmetric risk (from the viewpoint of foreign investors.)

b. China is energy-secure, while Korea & Taiwan’s high-margin tech exports effectively subsidize their increased oil import bills.

c. IT service exports, which is India’s solitary global competitive edge, is getting threatened by AI. Legacy coding tasks are getting automated.

ENDPIECE: Don’t Fight Mean Reversion

Don’t believe vested interests whose careers are built on the thesis of “Stocks Only Go Up.”

The world has shifted from the era of “Growth at Any Price” (GAP) to “Growth at a Reasonable Price” (GRP). That’s what has hit India.

Now either India delivers exceptional earnings growth in 2026 to justify its P/E multiples, OR the AI growth bubble bursts worldwide.

Until then, play defensive, avoid FOMO, and wait for the loose ball. Your time will come.

@arabicatrader

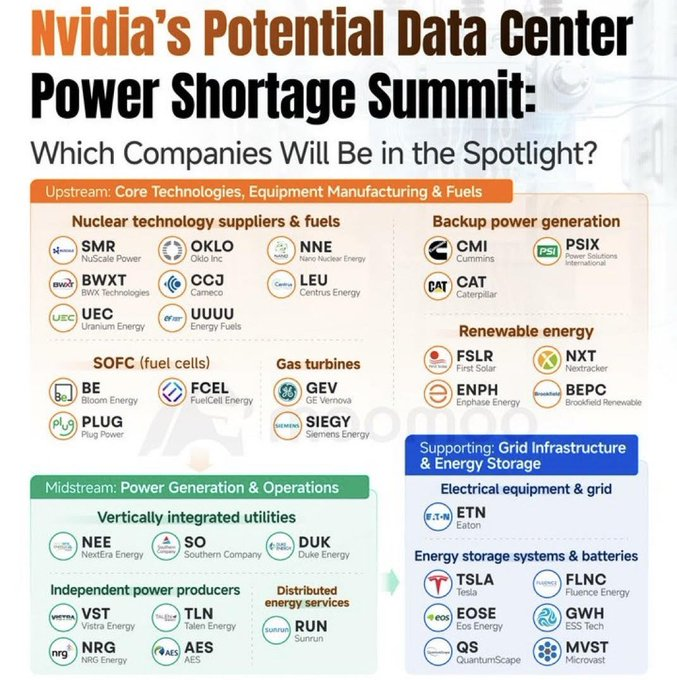

$NVDA has been clear that energy is the real bottleneck for AI with Morgan Stanley estimating a 44 GW U.S. power shortfall by 2028 so here’s how the power stack breaks down.

NUCLEAR

• $SMR industrializing small modular nuclear reactors

• $UUUU integrating uranium mining with fuel processing

• $OKLO building on-site nuclear power for AI data centers

• $CCJ anchoring uranium supply for the nuclear build cycle

• $LEU enabling advanced reactors through fuel enrichment

• $UEC scaling uranium production for long-duration demand

• $BWXT supplying critical nuclear components & fuel systems

• $NNE developing microreactors for distributed baseload power

GRID & STORAGE

• $TSLA scaling grid-scale battery storage

• $QS developing next-gen battery chemistry

• $EOSE commercializing long-duration storage

• $FLNC deploying utility energy storage for grid stability

• $MVST supplying batteries for storage & electrification

FUEL CELLS

• $BE deploying always-on solid-oxide fuel cells

• $FCEL providing distributed fuel-cell generation

• $GEV supplying flexible gas turbines to fill grid gaps

• $PLUG building hydrogen infrastructure for future power systems

RENEWABLES

• $ENPH enabling distributed solar & storage at the edge

• $FSLR manufacturing utility-scale solar for grid reliability

• $NXT improving utility solar economics through tracking systems

POWER OPERATORS

• $DUK upgrading grids to meet rising demand

• $SO expanding regulated baseload power infrastructure

• $NEE operating large-scale generation for AI-driven load growth

POWER PRODUCERS

• $AES scaling renewables & storage globally

• $NRG balancing generation and retail power exposure

• $VST monetizing flexible generation in tight power markets

• $TLN operating merchant power positioned for AI load spikes

Bitcoin miner turned AI bubble stock $IREN is up 22% pre-market on announcing a $9.7 billion GPU contract with $MSFT.

As always, the devil is in the details.

Before it can provide any service, IREN first needs to spend $5.8 billion buying the GPUs and ancillaries.

MSFT will provide $1.94 billion upfront, but IREN needs to come up with a further $3.86 billion to fund this capex.

Assuming this is debt financed at 10%, the 5-year contract achieves breakeven in year 4.

Here's the math:

Annual revenue: $1.94 billion

Initial capex: $5.8 billion

Total interest on loan: $0.77 billion

Gross profit: $3.13 billion

Annualized gross profit: $626 million

IREN currently spends $136 mn on SG&A to capture $500 mn in revenue. That amounts to 27 cents out of every dollar in revenue, down from 38 cents the previous year.

Assuming the same run rate and zero depreciation on the new data center facility, the company will spend $528 mn on SG&A to capture the incremental $1.94 bn in annual MSFT revenue.

Annualized operating profit = $98 million

Let's be charitable and assume the company manages to cut down SG&A to 20% of revenue.

Optimistic annualized operating profit = $238 million

While "$9.7 billion contract" makes for a great headline, the numbers throw cold water on this fairy tale.

Making $238 million on a $5.8 billion investment amounts to a mere 4.1% pre-tax return.

The hard truth is data centers are a low-margin business. Microsoft is smart, which is why they have signed this deal rather than build this capability in-house.

IREN investors have nothing to cheer for. This deal is inferior to simply buying 10-year US treasuries and calling it a day.

Everyone's burning $200/month on AI tools:

$20 – ChatGPT

$20 – Claude

$30 – Midjourney

$20 – ElevenLabs

$20 – Kling

$30 – Stable Diffusion

$50 – Minimax

But here’s the twist…

I found a way to use all of them for the price of a coffee

Here's how to use it↓