Tweet épinglé

dragob

333 posts

dragob

@Dragobbbb

niches get riches $NUAI / $IREN / $EQRLF

New York, NY Inscrit le Haziran 2024

57 Abonnements195 Abonnés

$NUAI dilution was a lot larger than expected but this gives management a war chest for co-invest and general corporate purposes. After paying off sharonai they will be left with $52MM that can be contributed to TCDC economics. I am now modeling between 40 - 50% economics vs 20%

English

@AtlasShrug1 agreed. very accretive use of dilution if it goes towards co-invest and upping their stake in the project.

English

Hopefully should not have to issue any additional equity going forward, certainly not before they sign the hyperscaler tenant. I’m using 126.85M FD share count now, including the public warrants which if exercised T $11.50 will bring close to another $70M in cash into the til. With more of the economics but modestly more shares out than I previously had modeled, I am still coming up with similar $16-24 of equity value for the 1GW TCDC project. And, fingers crossed, that will only be the first deal of many!

English

@Dragobbbb Are we sure the equity offering is just to raise the 30 million though. Is there any added dilution too for working capital?

English

@ThePrudentWhale I don’t believe the Term Loan can be used for equity. It is specifically stated for project level use such as equipment etc.

English

Sharon AI note wasn't due until June 30. Paying it off in cash kills that overhang early.

$NUAI secures up to $290M in debt financing.

$270M is ring-fenced to physically build the data center (adding co-invest to the Steam JV and boosting $NUAI equity ownership).

Bullish.

English

$NUAI owes Sharon AI $50M.

How they are paying it:

-$20M from the new Macquarie loan (the absolute max allowed)

-$30M from the new public stock offering

The loan legally forced the $30M offering.

The debt and equity raise are directly related.

The dilution HAD to happen.

English

$NUAI this equity offering drop off is a blessing to buy more shares after this amazing Macquarie Term Loan news. I upped my position sizing by 20%. The exact playbook that happened in $APLD is happening out here. Same exact lenders and bookrunners of Macquarie and Northland.

English

@Thebullwhisper I feel like calling the BDE crew in the AI/HPC space is a bit of a stretch. These are former bitcoin guys trying to pivot from what I see. Does BDE have any ai hpc customers?

English

Nothing is a given, lot's of steps on the way.

Replacing a failing board with a hungry board of directors already in the AI/HPC business was the most important one imo. I find it very hard to believe Endeavor, big digital energy LLC took over just to sell it at 250k/MW.

Imo more likely they JV with Mawson and get to fair value.

Here's a possible route to $700M mkt cap, should they fully win the vertua case (not likely though, it'll be a settlement at best). My base case is $300M anyways, just accounting for Mawsons 153MWs on the grid, rest is optional:

x.com/i/status/20372…

English

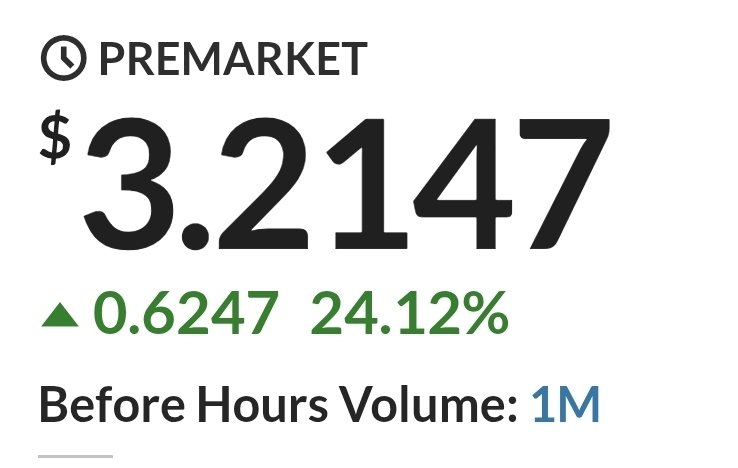

$MIGI could be the most violent play of 2026.

Getting $NUAI vibes from October when I sat comfy at $0.50 in the rocket taking of.

Vooooolume 1M premarket, 👀

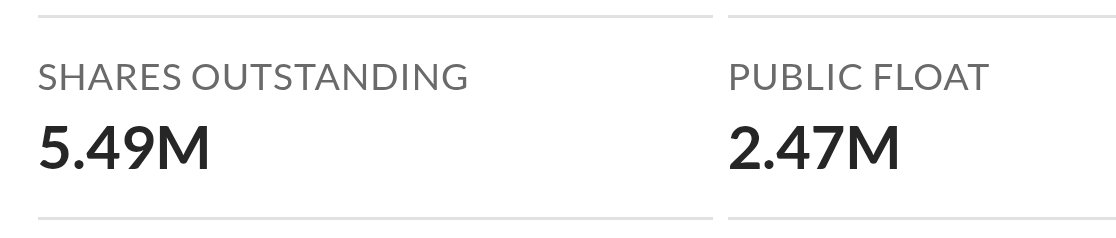

5M outstanding, 2.47M public float.

English

@Dragobbbb I am modelling a fundamental rerate to fair value at $500M mkt cap.

If they sell $7.50, bit boring, but so be it then.

English

@Thebullwhisper most likely path is being acquired by another miner in its current form unless proven otherwise. Im modeling a sale of the combined BDE+MIGI entity at 250K/MW for a share price of $7.5 at 5.5mm shares outstanding

English

@Thebullwhisper Great news overall and definitely derisked going forward with new board and management. Curious as to Big Digitals infra and what they own. Where are their sites? Do they own land and power or leased? None of the installed leadership is in the AI or datacenter space

English

@ConvexityStocks Are you sure nuai will be receiving development fees or management fees though? In press release there is no language of fees and stream will be main developer in this new jv

English

QHT

1/ A ~6% move in $NUAI after the Stream announcement tells me the market still does not understand what was disclosed.

PAY ATTENTION

English

@KashRamki thoughts on if they will still be retaining developer fees or is that all going to stream?

English

This is huge!! $NUAI now we’re cookin!

New Era Energy & Digital Partners with Stream Data Centers for Flagship TCDC Campus - businesswire.com/news/home/2026…

English

@samelifeenjoyer agreed. hopefully they get a good promote interest for bringing together all parties on top of prime real estate that they have

English

Wouldn’t be worse case depending on the equity stake size. An equity position in a $10B project with 80% debt financing and backed by Apollo could still be extremely valuable. They could lose development and management fees but we won’t know till $NUAI release their percentage equity.

English

I am sensing a lot of confusion around the $NUAI Stream Data Centers announcement today. Here is the plain language and questions I asked:

First who is Stream Data Centers?

Stream is not a random company. They are a Tier-1 U.S. data center operator with 25 years of operating history. Over 90% of their inventory is leased to Fortune 100 customers. They know how to build, operate, and lease data centers to the largest companies on earth.

They’re backed by Apollo Global Management. One of the largest alternative asset managers in the world with over $600 billion in AUM.

Apollo just chose to put their ecosystem partner into a deal with a $300M micro cap….. you can think on that.

Second what does this JV actually do?

$NUAI has the land, the power strategy, and the vision.

What they needed was:

A credible operator that hyperscalers trust. Institutional capital to fund construction 80% debt financing at competitive rates so please feel free to continue on with the dilution FUD 😂. This announcement delivered all three.

Stream operates the campus. An unnamed institutional investor funds the equity and leads the debt financing. $NUAI contributes the land and co-invests alongside them as an ongoing equity stakeholder. This is the GP/LP model Will Gray described on the March 17th call. It just all got confirmed.

Third, why does the 80% debt financing matter?

The press release explicitly confirmed approximately 80% debt financing on competitive market terms.

That means for every $1B of construction cost $NUAI only needs to fund $200M through equity. The other $800M comes from project level debt backed by the tenant’s creditworthiness. Again, miss me with any of your dilution FUD. They will have access to other financial vehicles as well.

This is how you build a multi-billion dollar campus without destroying your share count. The structure works and it just got confirmed.

Fourth, what about the hyperscaler?

Stream has direct relationships with leading cloud and technology companies and a track record of leasing to Fortune 100 customers. They weren’t brought in to find a tenant from scratch.

They were brought in because they already know how to execute with the exact type of customer $NUAI has been in deep talks with.

The JV is the vehicle through which the hyperscaler deal gets done. The operator and the capital are now in place. The tenant announcement is the next domino.

The bottom line

Most people looked at this announcement and saw a company they didn’t recognize partnering with $NUAI.

What actually happened is that one of the most credible data center operators in the country backed by one of the largest asset managers in the world just validated NUAI’s asset, their strategy, and their GP/LP model publicly.

That’s not a small thing. That’s the institutional stamp of approval the thesis needed.

The hyperscaler announcement is coming. Now you know the machine is in place to execute when it does. The Ted Warner hire was the only signal you needed. Anything bearish in here? No not really, other than this is an LOI agreement execution is still key but things are falling into place ⏱️

English