Francesco

818 posts

$AMD $3,000 is Inevitable Long Term 🧵

The roadmap to $5 Trillion Market Cap is much clearer today than just months ago due to sentiment shift, where I talked extensively for years since 2022/2023. Most subscribers and followers already know How lonely I was writing DDs on AMD in 2023. But the first time I heard Dr. Su "I love being able to bring the best product to the market; I really love to win" 11 years+ ago, I was in!

$3,000 is assuming no stock split. The timeline is accelerated much faster as CPU:GPU Ratio shifted from 1:4-8 to 3-5:1 in the near term and 10-20:1 as we get to Autonomous Agents by 2030 or sooner. Read more below. Put your seatbelt on, because it is going to be a long thread.

Slap the Like/Repost/Bookmark to please the X Algo.

If you want to support me to produce better quality threads, consider subscribe. And yes you will have access to more in-depth analysis.

Not Financial Advice! Just well-researched 🧵

I want to make this thread after $MSFT and $AMZN announced the important role for CPUs in this explosive Agentic AI Era. I will link both below and other threads to help you understand this topic. How Dr. Su is prepared for this AMD J-curve moment since 2020-2021 to have the full stack of AI Solutions from CPUs,GPUs, NPU, ROCm open Software, Networking & Interconnects, and Custom Chip. This is important to understand because:

~ $INTC has inferior CPUs than $AMD

~ $AMD Helios Racks are on track to outperform Rubin Racks with much lower TCO,TDP and $ per million tokens on training and inference.

~ $ARM makes inferior custom chips vs $AMD, precisely the AMD Custom chip HBv Series for $MSFT. Dr. Su is getting into Custom Chip for all large customers

~ AMD NPU is the best in the world atm with 0 competition for local/personal LLM on high-end laptops or workstations.

~10 of 10 major social media platforms now run EPYC including Meta, which was historically an Intel-only shop

~ 10 of 10 large SaaS organizations have converted to EPYC ~3× year-over-year public cloud adoption growth by large customers

~AMD's target of 50%+ server CPU market share is achievable by 2027 with Venice and Verano

~ 100% of AMD Helios AI racks (pairing Venice CPUs with Instinct MI455X GPUs) use EPYC as the host CPU, locking in CPU sales tied to AI GPU deployments

The two announcements from Amazon and Microsoft underscore a pivotal shift in AI infrastructure: Agentic AI (autonomous, always-on AI systems that reason, plan, execute multi-step tasks, and interact with tools/environments in real time) is dramatically elevating the role of CPUs alongside GPUs.

Amazon’s post (April 24, 2026) explicitly states that while GPUs/accelerators excel at parallel training/inference for LLMs, agentic workloads demand sustained, low-latency CPU-native tasks like sequential logic, file management, network calls, code execution, data retrieval, and orchestration across rapid execution cycles. AWS Graviton (ARM-based) is highlighted as purpose-built for this, with Meta deploying tens of millions of Graviton cores for global-scale agentic AI

Satya Nadella’s post (April 22, 2026) reinforces this: “Every agent will need its own computer” complete with dedicated enterprise-grade sandboxes, durable state, identity, and governance in Microsoft’s new Foundry hosted agents. This implies massive scaling of per-agent compute instances, far beyond batch inference.

This is not hype, it’s a fundamental rebalancing of data center spend. Training remains GPU-heavy, but inference + agentic execution (projected to become the majority of AI workloads) shifts toward CPUs for orchestration, low-latency reasoning, and sustained performance-per-watt at scale. Hyperscalers and enterprises are now optimizing entire stacks for “continuous intelligence,” not just bursty math.

The CPU:GPU Ratio is now shifting from 1:4-8 to 3-5:1, a complete change from 2023-2025. Now, that does not mean Training just gonna stop, NO. Training will continue to grow, but the pace of growth will be much slower than Inference. The Legend Larry Ellison $ORCL Chairman said this:

“Training AI models is a gigantic multi-trillion-dollar market. It’s hard to conceive of a technology market as large as that one. But if you look closely, you can find one that’s even larger: it’s the market for AI inferencing. Millions of customers are using those AI models to run businesses and governments. In fact, the AI inferencing market will be much, much larger than the AI training market. AI inferencing will be used to run robotic factories, robotic cars, robotic greenhouses, biomolecular simulations for drug design, interpreting medical diagnostic images and laboratory results, automating laboratories, placing bets in financial markets, automating legal processes, automating financial processes, and automating sales processes."

“In the end, all this money we’re spending on (AI model) training is going to have to be translated into products that are sold — which is all inferencing. And the inferencing market, again, is much larger than the training market.”

“People are running out of inferencing capacity.”

1. Why This Creates the Greatest J-Curve Growth Opportunity for AMD’s Full-Stack Solution

AMD is uniquely positioned to capture outsized upside here because it offers the industry’s strongest balanced, open full-stack AI infrastructure high-core x86 CPUs (EPYC), leading inference GPUs (Instinct MI series), ultra-low-latency networking (Pensando), and the open ROCm software stack. Unlike single-vendor or accelerator-only plays, AMD delivers end-to-end optimization for exactly the agentic workloads now exploding: CPU-orchestrated multi-agent systems running alongside GPUs for hybrid inference/MoE (Mixture of Experts) tasks

~CPUs become the control plane/orchestration engine: Agentic AI needs massive core concurrency for thousands of parallel agents, each with its own “computer” (sandboxed state, tools, reasoning loops). AMD EPYC already leads in core density, thread-per-watt, and x86 compatibility (critical for the vast Python/enterprise software ecosystem that ARM Graviton can’t always match without porting friction). AMD’s own analysis positions EPYC as ideal for agentic control planes, data preprocessing, and keeping GPUs fully utilized.

~Full-stack synergy drives TCO and performance leadership: AMD’s AI racks integrate EPYC host CPUs directly with Instinct GPUs + ROCm, enabling seamless orchestration, lower latency inter-core communication, and superior perf/system-watt. Partnerships like Nutanix further extend this into enterprise/hybrid clouds for agentic apps. This is exactly what hyperscalers and enterprises need as they move from GPU-only experiments to production agentic scale.

So what is your point Mike? When do we get to $5 Trillion?

The short answer is $50 B quarterly Revenue with 20-30% Cagr and Operating Margin in the 25%+. The market is only repricing @AMD for 10% of its long term potential. There are just so much room for hypergrowth. $50 B revenue sounds huge, but we may get there by 2027-2028 due to current explosive EPYC demand, projected to be 15-20m units.

2. EPYC Venice (H2 2026)is positioned as the World’s Best Server CPU for the Agentic Era

AMD’s 6th-gen EPYC “Venice” (Zen 6 architecture, TSMC 2nm) is sampling now and launches in 2026 alongside Instinct MI400 GPUs. Key specs and advantages:

~Up to 256 cores (33%+ increase over current Turin’s 192-core max) with radical package redesign for higher thread density (~1.3x) and bandwidth.

~Up to 70% overall performance uplift (and strong efficiency gains) vs. 5th-gen Turin, with massive memory bandwidth improvements (up to 1.6 TB/s via 16-channel DDR5/MRDIMM).

~Optimized for sustained, high-concurrency workloads, perfect for hosting “tens of millions” of agent sandboxes or orchestrating complex multi-step agent workflows with fast core-to-core communication.

Venice will power AMD’s next-gen Helios AI racks and deliver leadership TCO in exactly the always-on, reasoning-heavy environments Amazon and Microsoft are describing. It extends AMD’s current EPYC dominance (world-record benchmarks in enterprise, HPC, AI end-to-end) into the agentic wave, while remaining fully x86-compatible for drop-in deployment.

And most importantly, $TSM has the capacity to expand AMD EPYC supply to service a large % of this demand, per Dr. Su statement from Morgan Stanley Conference.

3. While everyone is struggling, $AMD is already working on the next beast EPYC, Verano 2027. A massive Step Forward for EPYC Dense Rack optimization

CPU for AMD’s 2027 AI rack-scale platforms (alongside Instinct MI500 GPUs). Highlights:

~First EPYC support for LPDDR5X SOCAMM2 memory ,delivering major perf/system-watt gains tailored for AI racks.

~Doubles rack density/scalability vs. prior generations, with 144+ MI500 GPUs per rack possible.

~Engineered for the exact agentic + MoE workloads: superior orchestration, energy efficiency at global scale, and tight GPU integration via ROCm.

This is the “big step forward” turning Venice’s raw power into rack-level, hyperscale efficiency for the always-on agentic internet. AMD’s roadmap (Venice 2026 → Verano 2027) aligns perfectly with the multi-year buildout of agentic infrastructure.

Conclusion:

Dr. Lisa Su’s long-term vision has been proven brilliantly correct. Years before the Agentic AI inflection, she repeatedly emphasized that the real scaling of AI would not be GPU-only; it would require powerful, high-core CPUs as the always-on control plane for orchestration, reasoning loops, tool use, and sustained low-latency execution the exact workloads now exploding in production. While the industry chased pure accelerator hype, Dr. Su doubled down on AMD’s full-stack advantage: EPYC as the world’s leading x86 server CPU, tightly integrated with Instinct GPUs and the open ROCm ecosystem.

Amazon’s April 24 announcement and Satya Nadella’s April 22 declaration (“Every agent will need its own computer”) are the ultimate market validation of that vision. Both hyperscalers are now publicly confirming what Dr. Su has been building toward: Agentic AI fundamentally shifts infrastructure spend toward CPU-native tasks at massive scale sequential logic, state management, multi-step orchestration, and real-time tool calling, precisely the strengths of high-core EPYC platforms.

The timing could not be more perfect. EPYC Venice (2026) arrives as the undisputed performance and efficiency leader for these workloads, while Verano (2027) delivers the rack-scale leap optimized for exactly the always-on, multi-agent systems Amazon and Microsoft are racing to deploy.

This is not incremental upside for AMD. It is the J-curve moment Dr. Su has engineered for years: the greatest multi-year growth acceleration in the company’s data-center history toward $5 Trillion Market Cap, driven by the very CPU-centric, full-stack architecture she insisted would define the next era of AI. The hyperscalers have now spoken. Dr. Su was right.

Not Financial Advice!

Mike@MikeLongTerm

$AMD at $600 is still cheap vs all others 🧵 Most should understand after you read the thread below, $AMD is so much cheaper than $ARM and $INTC. Now, $AMD is still the least owned Semi stock among all Funds because of bearish Analysts for years. Basically these institutions/Funds are reading these equity report on AMD and sold/trimmed AMD. So if we are talking about balancing back AMD to normal ownership level, it should be around $500-$600 approximately speaking. If you don't believe me, google those videos and equity papers on @AMD in 2022-2023-2024 and 2025. I was writing $AMD threads alone most of the time. $AMD is at ~$494B market cap or P/S 13x | Fwd P/S 6x-7x Fwd P/E 20-25x In what world this is expensive to you? PEG Ratio is 0.22. In what world is this expensive? $NVDA PEG Ratio is ~1; $AVGO PEG Ratio is 1.20 And AMD is the only company that has the full-stack AI solution CPUs,GPUs, NPU, ROCm open Software, Networking & Interconnects, and Custom Chip. And you think $494 B market cap is expensive? Think again!!!! IMO, AMD should be at 25x-28x or ~$600 a share. If we are using Forward P/S at 25x= $1,250 a share. For this kind of growth and potential, i'm already MAD Conservative. I'm not even pumping AMD here, just asking for a fair multiple. You have not seen FOMO at all, we are about to enter the most consequential J-curve Quarters or Q3 Q4 2026 toward the next 3-5 years. Now you know why I called analysts sexist for years. I will continue to do so as they kept rolling out 1GW Helios Rack revenue at $10 B. At $10 B, $AMD would lose money, and these idiots are getting paid $50-$200k a year on these equity reports. Mine is Free.99 or $10/month when subscribed. I will continue to call AMD Analysts sexist until they cover AMD fairly like other Semi companies. There is no need to judge base on male or female CEO, it should be judge purely on Financial Performance, Growth, and product leaderships. I spent years covering AMD, most followers and subscribers already know this. Analysts forecasted AMD to grow only 15-20% FY2026. Now they are rushing to change all PT and forecasts so they don't look like idiots. The whole Semi supply chain is complex and expensive to get Helios Racks to customers and AMD recognizes revenue when shipment gets to customers, not when customers decide to turn-on. 1GW of Helios Rack should generate ~$20-$25 B, because CPUs price is rising. The Industry is expecting 25-40% CPUs price increase for entire 2026, this is MASSIVE. Because the whole CPU:GPU ratio went from 1:4 to 3-5:1. $NVDA sold roughly 7m GPUs in 2025, so we are talking about 21m-35m Data Center CPUs shortage here, where $AMD EPYC Turin(Current Gen) is already dominating in all benchmarks. $AMD EPYC Venice is about to be shipped in less than 2 months, and will remain the best CPUs for a long time. AMD's rise in the server CPU market is one of the most dramatic reversals in semiconductor history. From less than 1% market share in 2017, AMD has grown to approximately 29% by late 2025, with EPYC Turin (5th Gen, Zen 5) driving record enterprise and hyperscale deployments. ~10 of 10 major social media platforms now run EPYC including Meta, which was historically an Intel-only shop ~ 10 of 10 large SaaS organizations have converted to EPYC ~3× year-over-year public cloud adoption growth by large customers ~AMD's target of 50%+ server CPU market share is achievable by 2027 with Venice and Verano ~ 100% of AMD Helios AI racks (pairing Venice CPUs with Instinct MI455X GPUs) use EPYC as the host CPU, locking in CPU sales tied to AI GPU deployments Not Financial Advice!

English

@amitisinvesting @giggspyt Great company for sure. Long term winner.

English

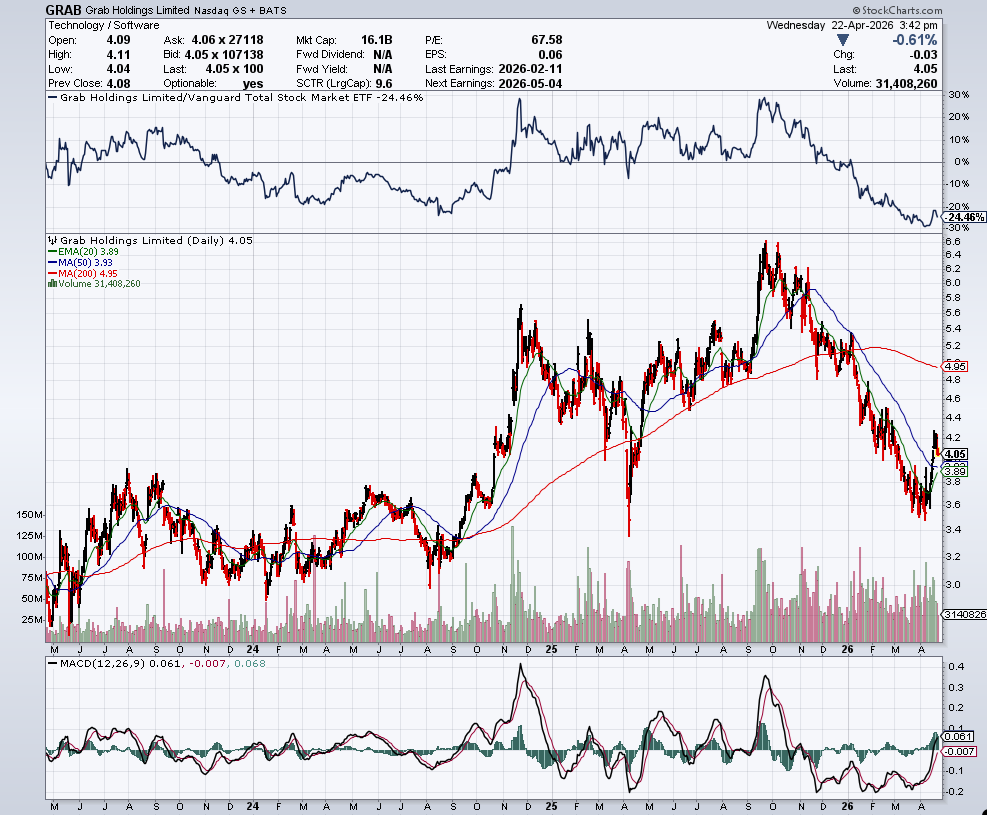

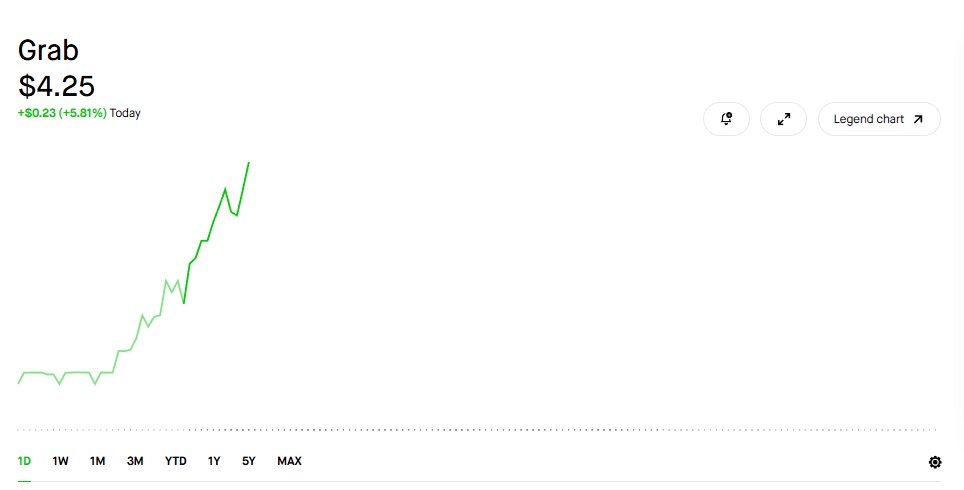

$GRAB

GRAB IS EXPANDING TO TAIWAN.

They are scooping up FoodPanda’s delivery business in the region for $600M with the deal expected to close in H2 2026.

Okay, I really like this. Here’s why:

1. The company has $6B in cash. We have been waiting for them to start using it in more strategic ways and this is one of the first expansions outside of SEA that makes sense given how synergistic the acquisition is to Grab’s overall business of delivery. Spending the cash pile they have on growth and expansion, especially if they can get discounted deals, is very good.

2. $UBER tried to buy this business for $1.25B last year. Regulators didn’t allow it. Grab is getting a 50% discount.

3. FoodPanda Taiwan did around $1.8B in GMV and is also profitable on an adjusted. EBITDA basis from last year. $GRAB did $14.2B of GMV last year so for $600M, they are adding 12% of GMV to the business in a profitable way. I really, really like this use of cash.

Ultimately, I own $GRAB for the broader thesis around the SuperApp becoming much bigger and more entrenched in different parts of the world. They have the cash, are guiding for 20% topline and 40% ebitda growth for the next 3 years, and can use these deals to consolidate within various regions to create continued operating leverage. Their fintech business is going to begin showing significant leverage this year as well which should compound the overall growth. At these prices, I do think the stock is intrinsically undervalued BUT it is not in the thematic of drones/nuclear/energy/etc and the rising oil prices have been a very ugly headwind for them.

Probably better opportunities out there short term but long term, these are the types of moves that continue to give me confidence as a shareholder.

Gab@GabGrowth

BREAKING: $GRAB has acquired Delivery Hero's FoodPanda Delivery Business in Taiwan. The deal has been agreed for $600 million in cash.

English

Apparently, at $307 stock price, $AMD becomes $500B market cap company!

English

$AMD: Mike is just pumping his stock for years

$PLTR: Mike is just pumping his stock for years

$TSLA: Mike is just pumping his stock for years

$XYZ : Mike is just pumping his stock for years

$HIMS: Mike is just pumping his stock for years

$GRAB: Mike is just pumping his stock for years

$META: Mike is just pumping his stock for years

$GOOGL: Mike is just pumping his stock for years

$AMZN: Mike is just pumping his stock for years

Well At least haters were consistent.

I was consistent too, sharing what I learned, and why they are high quality businesses.

Congratz to all @AMD shareholders, those that been following me for years. It is still very cheap at $330. Read more below to understand

Appreciate all the support from subscribers to improve the quality of researches for everyone!

Portfolio hit ATH, and AMD is now the largest position.

Not Financial Advice!

Mike@MikeLongTerm

$AMD at $600 is still cheap vs all others 🧵 Most should understand after you read the thread below, $AMD is so much cheaper than $ARM and $INTC. Now, $AMD is still the least owned Semi stock among all Funds because of bearish Analysts for years. Basically these institutions/Funds are reading these equity report on AMD and sold/trimmed AMD. So if we are talking about balancing back AMD to normal ownership level, it should be around $500-$600 approximately speaking. If you don't believe me, google those videos and equity papers on @AMD in 2022-2023-2024 and 2025. I was writing $AMD threads alone most of the time. $AMD is at ~$494B market cap or P/S 13x | Fwd P/S 6x-7x Fwd P/E 20-25x In what world this is expensive to you? PEG Ratio is 0.22. In what world is this expensive? $NVDA PEG Ratio is ~1; $AVGO PEG Ratio is 1.20 And AMD is the only company that has the full-stack AI solution CPUs,GPUs, NPU, ROCm open Software, Networking & Interconnects, and Custom Chip. And you think $494 B market cap is expensive? Think again!!!! IMO, AMD should be at 25x-28x or ~$600 a share. If we are using Forward P/S at 25x= $1,250 a share. For this kind of growth and potential, i'm already MAD Conservative. I'm not even pumping AMD here, just asking for a fair multiple. You have not seen FOMO at all, we are about to enter the most consequential J-curve Quarters or Q3 Q4 2026 toward the next 3-5 years. Now you know why I called analysts sexist for years. I will continue to do so as they kept rolling out 1GW Helios Rack revenue at $10 B. At $10 B, $AMD would lose money, and these idiots are getting paid $50-$200k a year on these equity reports. Mine is Free.99 or $10/month when subscribed. I will continue to call AMD Analysts sexist until they cover AMD fairly like other Semi companies. There is no need to judge base on male or female CEO, it should be judge purely on Financial Performance, Growth, and product leaderships. I spent years covering AMD, most followers and subscribers already know this. Analysts forecasted AMD to grow only 15-20% FY2026. Now they are rushing to change all PT and forecasts so they don't look like idiots. The whole Semi supply chain is complex and expensive to get Helios Racks to customers and AMD recognizes revenue when shipment gets to customers, not when customers decide to turn-on. 1GW of Helios Rack should generate ~$20-$25 B, because CPUs price is rising. The Industry is expecting 25-40% CPUs price increase for entire 2026, this is MASSIVE. Because the whole CPU:GPU ratio went from 1:4 to 3-5:1. $NVDA sold roughly 7m GPUs in 2025, so we are talking about 21m-35m Data Center CPUs shortage here, where $AMD EPYC Turin(Current Gen) is already dominating in all benchmarks. $AMD EPYC Venice is about to be shipped in less than 2 months, and will remain the best CPUs for a long time. AMD's rise in the server CPU market is one of the most dramatic reversals in semiconductor history. From less than 1% market share in 2017, AMD has grown to approximately 29% by late 2025, with EPYC Turin (5th Gen, Zen 5) driving record enterprise and hyperscale deployments. ~10 of 10 major social media platforms now run EPYC including Meta, which was historically an Intel-only shop ~ 10 of 10 large SaaS organizations have converted to EPYC ~3× year-over-year public cloud adoption growth by large customers ~AMD's target of 50%+ server CPU market share is achievable by 2027 with Venice and Verano ~ 100% of AMD Helios AI racks (pairing Venice CPUs with Instinct MI455X GPUs) use EPYC as the host CPU, locking in CPU sales tied to AI GPU deployments Not Financial Advice!

English

@todd20006 @unusual_whales They not need to approve in this case dude

English

Trump: I have ordered the US to kill any boat putting mines in the Strait

English

$AMD (April 23, 2026-daily chart update)

The whales handed us multiple opportunities to accumulate while bears and Elliott Wave analysts were loudly calling for a collapse to $160. This is exactly why DCAing at strong support levels remains one of the smartest strategies in the market.

When the bullish signals triggered, our community confidently doubled down before $200, positioning ourselves for powerful compounding gains.

There’s no need to perfectly time the absolute bottom at $76 — position sizing is ultimately what separates the winners from the rest.

The Great Mattsby@matthughes13

Its going to $397 $AMD x.com/matthughes13/s…

English

$GRAB in 2027-2028 S-curve ⤴️

Don't forget @MikeLongTerm talked about $GRAB Fundamental in more than 1,000 threads in 2025-2026 before it gets cool.

Consolidation in SEA is happening, AKA 90-95% market share.

MTUs is about to be explosive in 2027-2028

And yes i'm green on $GRAB

High quality is High quality in all cycles.

Yes it may take time for thesis to play out, especially when leadership chose long tem roadmap- the difficult route to dominate!

Not Financial Advice!

Mike@MikeLongTerm

$GRAB is worth so much more long term 🧵 Once u understand what the team is trying to build, it should worth so much more long term than today. Many are saying why shoud I bother when other long term like $AMD $PLTR $TSLA $HIMS $XYZ are already high quality. Well, this is a new long term since Feb 2025, and I got to average down significantly(im green now). And my long term bull thesis is 30x more from here($16.7B MC) or roughly $8-$9B rev a quarter. The other high conviction long term already have significant position sizing. I dont expect Grab to ramp up massive YTD return, it can take time for the thesis to play out. Stock price follows sentiment, not Fundamental or its long term potential. However, the market is incredibly efficient long term, where price action will follow fundamental. I don't need to chase the hyped tickers. And I don't plan to convince anyone to buy this stock. You have to do your own DD, as I dont offer Financial Advice! I'm enjoying the discount, when it is hated. or the legend Howard Marks, "discounted stock when it is not loved", yes OakTree capital owns $GRAB. 350-400m MTUs, 250-300m Subscribers are within achievable in 6-7 years or sooner. GRAB has the most resilient business model even during bad macro condition, it been through worse like slow growth 2018-2019, Covid, 2022 mad global inflation, and the last 40 days. I know many gonna say, Mike is just out here pumping his stock. Well if that was the case, I wouldnt write more than 1,000 threads on this company, and most of them are very long. Currently, Grab has 50.5m MTUs. Here are some of the keys MTUs could accelerate to 350-400m within 5 years. Ads revenue will be much higher at 350m-400m MTUs! A. FoodPanda recently sold Taiwan operation to $GRAB, but they are still in 3 markets competing with $GRAB(Malaysia, Singapore, and Philippines). Yes they are losing market share, drivers, users and merchants to $GRAB. FoodPanda is likely to exit these 3 markets as they have $5.44 billion debt and $2.9B in Cash. This would effective send $GRAB to be monopoly: ~Malaysia= 93-95%+ Market share ~Singapore= 94-95%+ Market share ~Philippines= 90-95%+ market share Foodpanda will likely to focus on these market to gain more operating leverage, and reduce debt ~Bangladesh(~70% market share) ~Pakistan(60-65% market share) ~Hong Kong(#1 player) And yes, it is entirely possible for Foodpanda to sell Bangladesh, Pakistan to GRAB later on like Taiwan. B. $GOTO(Indonesia) Mobility/Delivery negotiation is ongoing with $GRAB. No denial so far from management unlike the last 5 years. If we are using FoodPanda Taiwan sale price, $GOTO Mobility would only be worth $740m-$1B price tag. This would make $GRAB 90-95% market share in Indonesia and add: ~30m+ MTUs ~3.1m+ drivers ~20m+ merchants C. GrabFin is expected to accelerate MTUs, as it would allow 70%+ unbanked population or ~500m to access financial services from digital banking, insurance, payments, loan, GrabCoin(reward 3-5% on spending), and Wealth management. Users are now able to borrow money if they use $GRAB services or Cash Loan. The interest rate is 2.99%/month, which is much lower than loan shark or high interest lenders from 12-30% per month. This 2.99%/month will probably send Loan Book to above $2.5B or potentially $3B by end of 2026. D. Secret Weapon-Affordability Focus on Products ~Group Ride: Share a ride with up to 4 people on similar routes; AI coordinates pickups/split payments. Saves up to 40% on fares vs. riding alone ~Grab More: Add items from a second nearby merchant to your food/grocery order with no extra delivery fee, no minimum order, and no small-order fee. ~Grab AI Assistant/GrabGPT: Free ~GrabMaps open for consumers: Free and more accurate than GoogleMap.Grab can generate significant revenue off GrabMaps ~Travel Bundle/Package at discounted rates ~Paylater: with no interest if paid on time ~Cash Loan: at much lower interest than all banks/lenders ~Low cost insurances ~GrabUnlimited subscription for all services at discounted rate, priority support, additional rewards, and it should pay for itself within 2-3 uses. ~GrabCoins: earn 3-5% back when you spend like our credit card here, to increase more frequency ~GrabStays: Budget-friendly deals on Hotels/Motels with flexible cancellation. If you look at GMV/MTUs below, 2025 was the year that "Secret Weapon" strategy is working, as users are spending more on the SuperApp. It is not the SEA's Uber, it is not just Wechat-Financial like, It is not just Amazon ads/subscription like. It is a combination of all, to embrace Bottom of Pyramid, that longer term extend to 5 billion people TAM. While @AnthonyPY_Tan has ambitious goal, I set my projection to 700-800m TAM. I will adjust when we expand to more countries. Not Financial Advice!

English

BREAKING $GRAB & Globe Telecom Partnership🛜

Globe taps Grab’s driver network for real-time connectivity insights

Globe Telecom has partnered with Grab to enhance network optimization by harnessing real-world data gathered from everyday mobility across Metro Manila. The collaboration taps into Grab’s extensive network of driver-partners, transforming routine trips into dynamic data collection efforts that provide deeper visibility into network performance on the ground.

Through this initiative, over one hundred Grab driver-partners collected more than 20,000 network samples during the survey period, enabling Globe to assess connectivity strength and consistency across varying routes, traffic conditions, and times of day. The data offers a ground-truth perspective, capturing performance in high-traffic and previously untested areas, identifying weak coverage zones, and benchmarking live network conditions with greater accuracy.

The partnership allows both companies to co-develop targeted improvements that directly benefit users’ daily digital interactions—from ride-hailing to food delivery—while also enhancing the connectivity experience for Grab driver-partners. Improved network performance supports more reliable navigation and seamless app functionality, contributing to a more efficient and responsive digital ecosystem.

“This partnership gives us clarity from the ground up. By working with Grab and its dedicated fleet of driver-partners, we’re able to see how our network performs in real life and use that data to make meaningful improvements for their drivers and our customers,” said Eric Tanbauco, Vice President of Consumer Mobile Business at Globe.

By integrating real-world insights into its network strategy, Globe reinforces its commitment to delivering reliable connectivity as a critical enabler of the country’s digital economy.

Mike@MikeLongTerm

$GRAB| People are laughing at me now! 🤔 Not Financial Advice! Years from now, People will be laughing with me. Then "you were right Mike" It works like magic like other long term. I love the misunderstanding, the hatred for a ~Profitable ~FCF+ ~$6.8B Cash liquidity with little debt ~Accelerated MTUs growth ~70-75% market share inching 90-95% or Monopoly business, because I got to buy at mad godlike average. You cannot get a great price when everyone loves it. That is the truth on any stocks. $AMD $PLTR $TSLA $XYZ $HIMS were very cheap at certain points. Short sellers were dominating on daily/weekly headlines. Retail investors couldnt stop trashing it for months and years. But "Smart money" continued to add like a turtle. Slow but steady, and consistent. I really don't care what short sellers said because most of them are full of shit, and as soon as I pull out the D(DDs), they got quiet. They started showing financial numbers from the past or started insulting instead of having a genuine discussion. And then they started citing random business which is not even close to the core business to gain favor. I actually welcome short sellers, because I get to buy stocks at mad discounts. But I dislike how they maniplute stock price action or spread fake new to advance their positions in the near term. And that should be illegal. I don't mind if they actually post the truth, then I can revisit my thesis. 99.99% of my $GRAB threads are Free.99. But do know by subscribing, you will get to see better research. Investing is an ongoing journey, it is not an one time thing. Thesis can change or strengthen or progress much more rapidly. For example, At first I thought It would take 10 years+ to get to 350-400m MTUs and 250-300m GrabUnlimited Sub, now it will only take around 6 years or a bit longer. This is only based on 700-800m People TAM, while the Anthony's ambition is 5 billion people. Yes it can take time for his ambition to play out, he is willing to endure the pain of building the trust, the brandname, the reliability for folks at Bottom of Pyramid. The hardest group to build a profitable, FCF+ business, and Grab is the only company that got it done. 2025 was the first year $GRAB achieved full-year GAAP Proftiability. You can see how "Secret Sauce" and "Secret Weapon" are working nicely; the clearest trend is GMV/MTU and 2025. 2027 will be the year S-curve. Now if u can't afford subscription, just slap the like/repost and bookmark to show your love, to please the X algo so to speak. To see all my posts, you need to click turn on notification bell to, because I was told posts cannot show up to all followers(this is odd), but it is what it is. I know what I own, and you should too. I always stated that everyone should do their own DDs, and dont pay for those $300-$500/ a month or $10-$50k/year equity researches. You can get 99% of materials from my Free.99 Threads already, so dont pay that much. Starts with the basic 10k-q(Free) and even may be travel to SEA to try the service. Talk to drivers/merchants/users on the SuperApp to understand more. I was doing this in Jan 2025 vacation. I talked to at least 200 merchants and drivers. I paid my own sources in major markets to do more in-depth researchesm, and I shared most of them for Free.99. Yes That is how far I go with my DDs, because remember this "Mike does not F*** around with his capital long term". You can see that in other long term where I wrote extensively on them daily. I know many hated long threads, but you may have to follow other accounts to see short thread pump and dump. I don't do that. Alright, that is it. Not Financial Advice!

English

BREAKING $GRAB| HOLY 🐮🐮🐮🐮🐮🐮🐮

$85m PURCHASE From "Smart Money" 🚨🚨🚨

13F Filing-Assenagon Asset Management($98B Fund) MASSIVELY increased $GRAB by 20,152,535 shares or 58%.

Total Holding: 54,906,371 shares or $233m position.

(Screen shot and source below)

So Short sellers said $GRAB is going to $0, but "Smart money" bought even more or swallowed the float 😲

You see, short sellers lied, 13f doesnt!

Just like many large funds started small position on $GRAB will increase to tens of millions of shares. Assenagon Asset Management started on $GRAB with just 35,258 shares 🤔.

RIP Short sellers!

Mike@MikeLongTerm

$GRAB| People are laughing at me now! 🤔 Not Financial Advice! Years from now, People will be laughing with me. Then "you were right Mike" It works like magic like other long term. I love the misunderstanding, the hatred for a ~Profitable ~FCF+ ~$6.8B Cash liquidity with little debt ~Accelerated MTUs growth ~70-75% market share inching 90-95% or Monopoly business, because I got to buy at mad godlike average. You cannot get a great price when everyone loves it. That is the truth on any stocks. $AMD $PLTR $TSLA $XYZ $HIMS were very cheap at certain points. Short sellers were dominating on daily/weekly headlines. Retail investors couldnt stop trashing it for months and years. But "Smart money" continued to add like a turtle. Slow but steady, and consistent. I really don't care what short sellers said because most of them are full of shit, and as soon as I pull out the D(DDs), they got quiet. They started showing financial numbers from the past or started insulting instead of having a genuine discussion. And then they started citing random business which is not even close to the core business to gain favor. I actually welcome short sellers, because I get to buy stocks at mad discounts. But I dislike how they maniplute stock price action or spread fake new to advance their positions in the near term. And that should be illegal. I don't mind if they actually post the truth, then I can revisit my thesis. 99.99% of my $GRAB threads are Free.99. But do know by subscribing, you will get to see better research. Investing is an ongoing journey, it is not an one time thing. Thesis can change or strengthen or progress much more rapidly. For example, At first I thought It would take 10 years+ to get to 350-400m MTUs and 250-300m GrabUnlimited Sub, now it will only take around 6 years or a bit longer. This is only based on 700-800m People TAM, while the Anthony's ambition is 5 billion people. Yes it can take time for his ambition to play out, he is willing to endure the pain of building the trust, the brandname, the reliability for folks at Bottom of Pyramid. The hardest group to build a profitable, FCF+ business, and Grab is the only company that got it done. 2025 was the first year $GRAB achieved full-year GAAP Proftiability. You can see how "Secret Sauce" and "Secret Weapon" are working nicely; the clearest trend is GMV/MTU and 2025. 2027 will be the year S-curve. Now if u can't afford subscription, just slap the like/repost and bookmark to show your love, to please the X algo so to speak. To see all my posts, you need to click turn on notification bell to, because I was told posts cannot show up to all followers(this is odd), but it is what it is. I know what I own, and you should too. I always stated that everyone should do their own DDs, and dont pay for those $300-$500/ a month or $10-$50k/year equity researches. You can get 99% of materials from my Free.99 Threads already, so dont pay that much. Starts with the basic 10k-q(Free) and even may be travel to SEA to try the service. Talk to drivers/merchants/users on the SuperApp to understand more. I was doing this in Jan 2025 vacation. I talked to at least 200 merchants and drivers. I paid my own sources in major markets to do more in-depth researchesm, and I shared most of them for Free.99. Yes That is how far I go with my DDs, because remember this "Mike does not F*** around with his capital long term". You can see that in other long term where I wrote extensively on them daily. I know many hated long threads, but you may have to follow other accounts to see short thread pump and dump. I don't do that. Alright, that is it. Not Financial Advice!

English

$AMD Inference Queen vs Training King $NVDA 🧵

@AMD : $453.87B market cap

P/S: 13x | Fwd P/S less than 6x

P/E 106x | Fwd P/E 20x-25x

@nvidia : $4.9 Trillion market cap

P/S: 23x | Fwd P/S 18-20x

P/E: 41x | Fwd P/E 24-28x

It is not that NVDA cant grow, but when company hit this size or the top 10 mega cap, it would require so much buying inflow to move it, and it will. Where $AMD MC is tiny for its true potential. Just looks at how Fwd P/S and P/E are collapsing or cheaper to anyhting else on the market at this size and this growth. And yes AMD stock price will move slower when it gets to $4-$5 Trillion. It is the nature of boomers(money managers) making the call, and they like to overpay for $WMT and $COST(5-8% growth).

Followers and Subscribers already know I been talking about EPYC and Agentic AI since 2023/2024. And the demand for Inference will shift the balance CPU:GPU from 1:4-8 to 10-20:1 by 2030, or Autonomous Agents where fleets of agents running 24/7 for enterprises. GPU was the King from 2023-2025, 2026 and beyond are the time for Inference Queen!

Over the past decade, FLOPs required for leading models have grown >4x every year. This trend continues as models get smarter (larger, more capable reasoning). Training remains GPU-heavy and NVIDIA-dominant, but it’s “only” a 4x annual ramp.

Inference (tokens processed): Exploded 100x in the last two years alone. This is the “always-on” phase, billions of daily users, embedded AI everywhere, and now agentic systems running continuously

Inference has now reached (and in many cases surpassed) training as the dominant driver of new compute spend. Traditional single-shot LLM calls (one prompt → response) were GPU-bound and relatively contained. Agentic AI changes everything.

1. What Is Agentic AI and Why It Supercharges Inference Demand, and EPYC is the best CPU

~They plan & break tasks into steps).

~Reason (chain-of-thought, critique, iterate).

~Act (call tools/APIs, query databases, interact with external systems).

~Orchestrate (spawn sub-agents, coordinate multi-agent teams, loop until success).

~Examples: Autonomous research agents, multi-step enterprise workflows, self-improving code/debug agents, robotics control loops, or customer-support agents that handle full conversations + backend actions.

The real explosive J-Curve:

~A traditional LLM query might use 50–500 tokens.

~An Agentic Workflow can use more than 50,000 tokens or 1,000 more, because each step involves fresh inference calls, tool results, re-planning, verification...

=> This is persistent, latency-sensitive, and 24/7 (not batchable like training). Real-world adoption data shows agentic traffic growing 7,851% YoY in 2025, with 79% of organizations already deploying agents and 96% planning expansion in 2026. Multi-agent orchestration grew 327% in just four months in some Fortune 500 deployments.

2. Why this shifts the balance Dramatically Toward CPU:GPU in the ratio of 1:1, and in just months to 3-5:1.

It used to be 1:4-8 prior explosive Agentic demand since Feb 2026. By 2030, CPU:GPU ratio will change dramatically to 10:1 to 20:1.

The shift in CPU:GPU ratio toward much higher CPU intensity ( 10:1 to 20:1 in terms of CPU cycles, cores, or sockets relative to GPUs in some interpretations) isn't about replacing GPUs, it's about the fundamental change in workload architecture that agentic AI introduces. Traditional LLM inference was mostly "one-shot" matrix math on GPUs. Agentic AI turns it into a complex, multi-step operating system-like workflow where the control plane (orchestration) dominates.

Traditional LLM inference is ~90%+ GPU-bound matrix math (parallel token generation). Heavy orchestration, scheduling, data movement, tool calling, memory/database queries, control flow, and decision logic. GPUs excel at parallel math but are inefficient for irregular, low-latency, branchy, sequential control-plane work.

CPUs become the bottleneck (or enabler): They keep GPUs fed/utilized, route data between agents/enterprise apps/data lakes, manage state, enforce policies, and handle the “results-focused” management layer.

Current 5th-gen EPYC Turin (Zen 5, up to 192 cores/384 threads) already leads in many orchestration and mixed AI workloads vs. Intel Xeon 6 and even NVIDIA Grace, with strong perf/watt and TCO advantages. But Venice takes it to the next level and is purpose-built for exactly this agentic shift.

Venice will power AMD's Helios rack (shown at CES 2026): each tray/node pairs one Venice CPU with four MI455X GPUs + Pensando/Vulcano networking, liquid-cooled for yotta-scale efficiency. This is explicitly designed for the training + massive inference demands Su described.

Conclusion: At CES 2026, she stood on stage and delivered a clear, data-backed message: while training compute continues its impressive ~4x annual growth in FLOPs, inference has already exploded 100x more tokens processed in just the last two years marking a decisive inflection point. To support AI everywhere, from billions of users to autonomous agents solving complex real-world problems, the world will need another 100x increase in total AI compute capacity over the next 4–5 years, pushing beyond 10 yottaflops.

She was right because the rise of agentic AI systems (since 2023/2024) that don’t just answer questions but plan, reason, use tools, iterate, coordinate with other agents, and act autonomously is fundamentally rewriting the economics and architecture of AI infrastructure. A single traditional query might consume hundreds of tokens on a GPU. A sophisticated agentic workflow can multiply that by 15x, 50x, or even 1,000x through repeated reasoning loops, tool calls, verifications, and multi-agent orchestration. The result is not just more inference volume, but a profound shift in workload character: bursty GPU math now sits inside a much larger, persistent, CPU-intensive control plane.

This drives the dramatic rebalancing of CPU:GPU ratios. Traditional GPU-heavy clusters (often 1:4 to 1:8 CPU sockets to GPUs) are giving way to far more CPU-centric designs. Orchestration, tool processing, state management, data movement, and latency-sensitive decision logic can consume 50–90% of end-to-end latency in agentic flows. To keep expensive GPUs saturated and responsive, hyperscalers and enterprises are deploying significantly more high-core CPU capacity pushing effective ratios toward 5:1, 10:1, or even higher in CPU cycles and orchestration layers as fleets of autonomous agents run 24/7.

And here is where AMD’s positioning shines. Dr. Su didn’t just call the trend, she unveiled the hardware blueprint to ride it: the Helios rack-scale platform, powered by Instinct MI455X GPUs for raw acceleration and the next-generation EPYC Venice (Zen 6) CPUs as the orchestration engine. With up to 256 cores on an advanced 2nm process, explosive memory bandwidth (1.6 TB/s raw or 2-3x memory bandwidth in optimized workload setup), revolutionary dual I/O dies, and massive PCIe scaling, Venice is purpose-built to feed GPUs efficiently while dominating the branchy, memory-intensive, high-concurrency work that agentic AI demands. Paired with Pensando networking and the open ROCm ecosystem, Helios delivers a balanced, energy-efficient, yotta-scale solution that hyperscalers and enterprises can actually deploy at volume.

Dr. Su was right because she saw beyond the GPU headlines to the full-stack reality: the inference explosion is here, agentic AI is the multiplier, and balanced systems where powerful CPUs like EPYC Venice keep everything humming will determine who wins at scale. Training will keep growing steadily, but the real infrastructure buildout, the real spend, and the real opportunity in the coming years will be shaped by this new, CPU-augmented inference era.

Not Financial Advice!

Mike@MikeLongTerm

$AMD NEEDS $TSM to hit $1,000 a share 🧵 Understanding 2nm Wafer Capacity ✍️ Context:Current EPYC CPU demand is 15-20m units, and is projected to double from H2 2026 to H1 2027. Meaning Supply is way behind from Demand, as companies are using entire year token budget in less than 30 days. Meaning, Agentic AI is consuming high CPU resources because it operates through continuous, multi-step Reasoning-Action-Observation loops rather than single-pass inference. TSMC's N2 (2nm) early phase production launched in late 2025 has already positioned the company for an accelerated ramp far beyond typical new-node timelines, directly supporting bullish outlook on scaling from ~25-35k to 60k+ wafers per month and unlocking millions of extra AMD EPYC Venice server CPUs. This is the first GAA/nanosheet node, with volume production kicking off on schedule (and with strong initial yields) at dedicated fabs in Taiwan. Combined output from the first lines started at ~35k-40k WPM (some early 2026 reads put it at 40k-60k aggregate). Yields opened strong at ~70% (with Taiwan sources reported of 75-80% overall and higher on certain layers) well above historical new-node averages. This "stable yield" is the key technical enabler for the post's "faster than standard" ramp, as it allows parallel equipment qualification and minimal downtime. 1. How many 2nm Fabs are Online and Planned TSMC's N2 production is centered in Taiwan (with U.S. contributions later). Fabs here are massive "Gigafab" sites with multiple phases (P1, P2..), each adding tens of thousands of WPM. Current(April 2026): We have 2 Primary Fabs for 2nm ~Fab 20 (Hsinchu Baoshan): Phase 1 online since late 2025. Initial ~20k-25k WPM contribution. ~Fab 22 (Kaohsiung): Phase 1 online (first to start volume production in Dec 2025); Phase 2 now in trial production / early ramp. As of now, 35k-60k WPM output is expected, and the are fully booked for 2026. TSMC aggressive Expansion which will help $AMD to service explosive Agentic AI demand Fab 20: P3 and P4 under construction (for N2 and below-2nm). Fab 22: P3 mostly complete, P4/P5 already breaking ground all five phases targeted fully operational by Q4 2027. Additional new sites: Three more in Tainan + expansions in central/northern parks ( Taichung, Chiayi). TSMC Target: Aggregate N2 capacity 120k-150k WPM (2026). This is a ~3-4x jump from early 2026 levels in roughly 9-12 months beating my own conservative "1+ year per major phase" typical timeline thanks to 70-80% yields and capex ($60B+ baseline for 2026, potentially higher). Arizona Fab 21 Phase 3/4 (N2-capable) targeted for equipment install in 2026 and production ramp 2027-2028 (initial ~20k WPM for N2 in some phases). TSMC has committed ~30% of future sub-2nm output to U.S. fabs long-term. => 2 fabs online, scaling 4 more fabs/phases toward end of 2026, and actively planning 10 fabs in the next 12-24 months. Timeline could go down with higher demand from AMD 3. The question is, how much TSMC can ramp up supply to support AMD significant demand for EPYC Venice in H2 2026? Venice is AMD's first HPC product on N2 (taped out April 2025, silicon validated with excellent perf/efficiency), using a chiplet design with N2 CCDs + 3nm I/O dies and advanced 3D SoIC packaging. Helios racks (AMD's new rack-scale AI platform) represent committed baseline volume( @OpenAI , $Meta, $MSFT, $ORCL, LumaAI...) , but TSMC's accelerated multi-fab expansion provides substantial headroom for standalone EPYC sales, hyperscaler direct purchases, and further Helios upside. According to TSMC CEO C.C. Wei, he expects "Faster ramp in 2026" due to higher yield and parallel fab buildouts on 2nm. 1m additional EPYC Venice would require 20-25k wafers(estimate). It is possible to ramp up 7-10m additional EPYC Venice to service Agentic AI demand or roughly 13-15k additional wafers per month from H2 2026 to H1 2027. This will enable AMD to: ~Fulfill hyperscaler Venice dense rack orders faster. ~Capture standalone server CPU share (vs. Intel). ~Support "Agentic AI" pricing power and multi-year data-center growth. Conclusion: TSMC’s accelerated N2 (2nm) ramp already delivering strong ~70-80% yields from the two primary Gigafabs (Fab 20 in Hsinchu and Fab 22 in Kaohsiung) that came online in late Q4 2025 makes the addition of 7-10 million extra EPYC Venice units for AMD from H2 2026 through H1 2027 not only technically feasible but a highly probable outcome of disciplined execution under explosive AI/HPC demand. Aggregate N2 output is scaling from the current ~35k-50k wafers per month (WPM) baseline to 120k-150k WPM by year-end 2026, with four+ effective plants/phases contributing and further phases (including Fab 20/22 expansions plus new Tainan sites) coming online in parallel. This delivers tens of thousands of incremental WPM precisely during the 12-month window in question compressing the “typical” 1+ year per major phase timeline thanks to stable yields and $52-56 billion in 2026 capex Each ~76 mm² Zen 6 CCD (12-core/48 MB L3 standard; up to 32-core Zen 6c dense variant) yields ~450-640 good dies per 300 mm wafer at current-to-mature N2 yields. With Venice’s chiplet design (typically 8 CCDs + I/O die + advanced 3D SoIC packaging), blended output across the full SKU mix lands in the realistic 40-60 CPUs per wafer range during ramp. Even conservatively allocating AMD 10-15%+ of incremental N2 capacity , the math easily supports multi-million extra units on top of the committed Helios rack baseline. TSMC isn’t just hitting its J-curve; it is breaking out of J-curve the historical new-node ramp curve because yields are strong, fabs are being stood up in parallel, and AI urgency is driving prioritization and capex flexibility. This supply tailwind directly validates and amplifies the multi-year bullish case for AMD turning 2026-2027 into a revenue and margin inflection point driven by Agentic AI server demand, pricing power, and share gains. Not Financial Advice!

English

$GRAB MTU Trajectory 📶

The speed and quality of Grab's MTU growth is the clearest signal that the affordability pivot is working. From 41.9 million MTUs in Q3 2024, the platform scaled to 50.5 million MTUs in Q4 2025 , adding nearly 9 million transacting users in six quarters. Critically, this growth is demand-led: transaction volumes are consistently outpacing both MTU and GMV growth, which means users are transacting more frequently, not just joining the platform.

At current pace, it would need 7-9 years to reach 350-400m MTUs, but Here are some of the variables that will speed things up or down to ~6 years to get there. Or roughly $7-$8B revenue per quarter, this is only sticking to 700-800m people TAM.

1. Affordable products & intentional MTU focus: Management has explicitly called out affordability (, cheaper rides, GrabFood for One, Shared Saver/group buying, grocery/quick-commerce pushes, cheaper everything) as one of the fastest ways to add new users. These launched or ramped in 2025 and are designed to broaden the addressable market (solo diners, price-sensitive users...). This directly counters the recent slowdown in MTU growth

2. GrabFin scaling: This is the biggest potential multiplier. The loan portfolio doubled YoY to $1.18 billion in Q4 2025. Management is on track to exceed $2 billion by end-2026, with more cross-sell (payments, insurance, investing via the Stash acquisition tech). Fintech drives higher engagement, frequency, and new-user acquisition (especially unbanked/underbanked populations). It also improves monetization per user, which indirectly funds more affordability.

Cash Loan is incentivizing new users to spend to establish credit score, this will allow GRAB to grow Loanbook to $2.5-$3B.

Longer term, it should be able to generate 12-15% of total Loan Book per quarter. For example $30B loan book can generate $3.6-$4.5B revenue per quarter when including all other financial services. % of all loanbook is an easier way to picture the story.

3. New verticals driving MTU expansion: GrabMart, GrabMore (grocery add-on to food orders), Dine-out, GrabCoin, GrabFinancial(more lending,insurance, payment, banking, invest products), and Aggressive Tourism expansion(Booking, travel package, GrabPay...) are bringing entirely new user cohorts who may not have engaged with Grab through ride-hailing or food delivery alone.

4. AI & new features: Just launched at GrabX 2026 (April 2026) 3 AI-powered experiences for consumers, merchants, drivers, and travelers. This deepens the “everyday guide” superapp role and could boost retention + acquisition. Grab AI Assistant or I called it GrabGPT, they should name it GrabGPT, this will bring in more users that search for foods/ride/dine-out/financial products searches. GrabMap will also be great "free" engagement to get new users in.

5. Large markets remain underpenetrated like Vietnam, Indonesia, Philippines. Meaning so much more room to grow, especially after $GOTO Mobility/Delivery is acquired.

6. Proven GMV per MTU is the most important signal

(Detail Thread below)

In a SuperApp business, user count is necessary but insufficient. What separates winners from flash-in-the-pan growth stories is spend per user , the depth of wallet penetration. For Grab, On-Demand GMV per MTU is the single clearest indicator that the platform is deepening its hold on Southeast Asian consumers beyond one-dimensional use cases. If MTUs are growing and GMV/MTU is also growing, it means the platform is getting simultaneously wider (new users) and deeper (existing users spending more). That dual expansion is exactly what Grab is demonstrating.

The significance of a rising GMV/MTU in the context of strong MTU growth cannot be overstated. Normally, as a platform scales to more price-sensitive user cohorts, average spend per user dilutes. Grab is defying this pattern: even as it intentionally recruits lower-income, higher-price-sensitivity users through Saver products, the GMV/MTU metric is rising. This happens because the existing base , particularly GrabUnlimited subscribers , is deepening engagement across multiple verticals at a faster rate than the spend dilution from new cohorts.

7. The current state of GrabUnlimited and long term

GrabUnlimited is the largest on-demand loyalty subscription program in Southeast Asia. Its fundamental value proposition , discounted delivery fees, menu-wide percentage discounts, exclusive merchant perks, and priority customer support , has proven to be the most effective tool for converting occasional users into habitual, high-LTV subscribers.

GrabUnlimited members spend approximately 5x more in total platform GMV and order approximately 3x more frequently than non-subscribers. In food deliveries alone, subscribers spent 4.2x more relative to non-subscribers. In Southeast Asia, one out of two of Grab's top spenders are now GrabUnlimited subscribers , confirming that the program has successfully captured the highest-LTV segment of the user base.

For merchants and drivers: GrabUnlimited creates a dedicated high-frequency buyer audience that merchants can specifically target with marketing spend. "From a merchant perspective, if you have a USD 100 marketing budget, it makes more sense for you to invest that on the GrabUnlimited base" , Shweta Padmanaban, Head of Product, Consumer Experience at Grab. This allows Merchants and Drivers to enjoy consistent income/growth.

At its core, GrabUnlimited is not just a loyalty program , it is a recurring revenue mechanism with Amazon Prime-like economics. Subscribers pre-commit to the platform, increasing switching costs and driving cross-vertical spend. A GrabUnlimited subscriber who pays for the delivery benefit is naturally inclined to use GrabPay for payments, GrabFinancial for lending, and Grab mobility for rides , because each usage reinforces the ROI of the subscription.

To add on top, GrabCoin is another credit card like reward at 3-5%, to fuel even more spending from existing and new users.

In conclusion, Grab is poised to deliver one of the most compelling multi-year growth stories in global tech scaling from 50.5 million MTUs today to 350–400 million within just six years (by 2031–2032). The foundation is already proven, Grab has more than doubled its user base from ~26 million in Q4 2021 to 50.5 million by Q4 2025, navigating COVID volatility and emerging stronger with consistent mid-teens growth and rising cross-app usage. That progress was powered by core strengths in mobility, deliveries, and the affordability initiatives + GrabFin scaling.

The next leap, a roughly 7–8x expansion requiring ~38–41% annual MTU CAGR becomes achievable through new verticals and deliberate geographic + demographic expansion, all squarely in Grab’s execution playbook. With an asset-light model, strong free-cash-flow generation, and Anthony Tan’s long-term vision of serving the “bottom of the pyramid” across 5 billion people globally, these moves compound: more verticals drive higher frequency → more data fuels better AI → broader expansion adds users faster than ever before.

By 2032, 350–400 million MTUs would represent not just a numbers milestone but a generational shift making Grab the dominant intelligent SuperApp for daily life, commerce, and finance across Southeast Asia and beyond. The trajectory from the 2021–2025 chart is clear: every chapter has been about building the flywheel. The next six years are when that flywheel hits escape velocity. The opportunity is massive and Grab is built exactly for this moment.

Not Financial Advice

Mike@MikeLongTerm

$GRAB is worth so much more long term 🧵 Once u understand what the team is trying to build, it should worth so much more long term than today. Many are saying why shoud I bother when other long term like $AMD $PLTR $TSLA $HIMS $XYZ are already high quality. Well, this is a new long term since Feb 2025, and I got to average down significantly(im green now). And my long term bull thesis is 30x more from here($16.7B MC) or roughly $8-$9B rev a quarter. The other high conviction long term already have significant position sizing. I dont expect Grab to ramp up massive YTD return, it can take time for the thesis to play out. Stock price follows sentiment, not Fundamental or its long term potential. However, the market is incredibly efficient long term, where price action will follow fundamental. I don't need to chase the hyped tickers. And I don't plan to convince anyone to buy this stock. You have to do your own DD, as I dont offer Financial Advice! I'm enjoying the discount, when it is hated. or the legend Howard Marks, "discounted stock when it is not loved", yes OakTree capital owns $GRAB. 350-400m MTUs, 250-300m Subscribers are within achievable in 6-7 years or sooner. GRAB has the most resilient business model even during bad macro condition, it been through worse like slow growth 2018-2019, Covid, 2022 mad global inflation, and the last 40 days. I know many gonna say, Mike is just out here pumping his stock. Well if that was the case, I wouldnt write more than 1,000 threads on this company, and most of them are very long. Currently, Grab has 50.5m MTUs. Here are some of the keys MTUs could accelerate to 350-400m within 5 years. Ads revenue will be much higher at 350m-400m MTUs! A. FoodPanda recently sold Taiwan operation to $GRAB, but they are still in 3 markets competing with $GRAB(Malaysia, Singapore, and Philippines). Yes they are losing market share, drivers, users and merchants to $GRAB. FoodPanda is likely to exit these 3 markets as they have $5.44 billion debt and $2.9B in Cash. This would effective send $GRAB to be monopoly: ~Malaysia= 93-95%+ Market share ~Singapore= 94-95%+ Market share ~Philippines= 90-95%+ market share Foodpanda will likely to focus on these market to gain more operating leverage, and reduce debt ~Bangladesh(~70% market share) ~Pakistan(60-65% market share) ~Hong Kong(#1 player) And yes, it is entirely possible for Foodpanda to sell Bangladesh, Pakistan to GRAB later on like Taiwan. B. $GOTO(Indonesia) Mobility/Delivery negotiation is ongoing with $GRAB. No denial so far from management unlike the last 5 years. If we are using FoodPanda Taiwan sale price, $GOTO Mobility would only be worth $740m-$1B price tag. This would make $GRAB 90-95% market share in Indonesia and add: ~30m+ MTUs ~3.1m+ drivers ~20m+ merchants C. GrabFin is expected to accelerate MTUs, as it would allow 70%+ unbanked population or ~500m to access financial services from digital banking, insurance, payments, loan, GrabCoin(reward 3-5% on spending), and Wealth management. Users are now able to borrow money if they use $GRAB services or Cash Loan. The interest rate is 2.99%/month, which is much lower than loan shark or high interest lenders from 12-30% per month. This 2.99%/month will probably send Loan Book to above $2.5B or potentially $3B by end of 2026. D. Secret Weapon-Affordability Focus on Products ~Group Ride: Share a ride with up to 4 people on similar routes; AI coordinates pickups/split payments. Saves up to 40% on fares vs. riding alone ~Grab More: Add items from a second nearby merchant to your food/grocery order with no extra delivery fee, no minimum order, and no small-order fee. ~Grab AI Assistant/GrabGPT: Free ~GrabMaps open for consumers: Free and more accurate than GoogleMap.Grab can generate significant revenue off GrabMaps ~Travel Bundle/Package at discounted rates ~Paylater: with no interest if paid on time ~Cash Loan: at much lower interest than all banks/lenders ~Low cost insurances ~GrabUnlimited subscription for all services at discounted rate, priority support, additional rewards, and it should pay for itself within 2-3 uses. ~GrabCoins: earn 3-5% back when you spend like our credit card here, to increase more frequency ~GrabStays: Budget-friendly deals on Hotels/Motels with flexible cancellation. If you look at GMV/MTUs below, 2025 was the year that "Secret Weapon" strategy is working, as users are spending more on the SuperApp. It is not the SEA's Uber, it is not just Wechat-Financial like, It is not just Amazon ads/subscription like. It is a combination of all, to embrace Bottom of Pyramid, that longer term extend to 5 billion people TAM. While @AnthonyPY_Tan has ambitious goal, I set my projection to 700-800m TAM. I will adjust when we expand to more countries. Not Financial Advice!

English

$AMD would still be cheap at $3 Trillion dollar market cap.

If you do enough research and follow what I wrote over the months and years, many would understand how undervalued AMD is right now.

And it shouldn't trade at less than 6x Fwd P/S

Not Financial Advice!

youtube.com/watch?v=w5KlIB…

YouTube

English

@MikeLongTerm @giggspyt Bravo Mike grab is huge great company long term winner. My friend in South Asia told me great company

English

$GRAB around $10 🧐

That is when people start saying

"Oh i understand $GRAB business now"

Not when I wrotes more than 1,000 threads DD on this company.

Then they will cry when the stock pull back, say from $10 to $8.

Conviction cannot be borrowed or convinced.

Years from now, most will look back at how low it traded because of 2 months conflict.

Not Financial Advice!

Mike@MikeLongTerm

$GRAB is worth so much more long term 🧵 Once u understand what the team is trying to build, it should worth so much more long term than today. Many are saying why shoud I bother when other long term like $AMD $PLTR $TSLA $HIMS $XYZ are already high quality. Well, this is a new long term since Feb 2025, and I got to average down significantly(im green now). And my long term bull thesis is 30x more from here($16.7B MC) or roughly $8-$9B rev a quarter. The other high conviction long term already have significant position sizing. I dont expect Grab to ramp up massive YTD return, it can take time for the thesis to play out. Stock price follows sentiment, not Fundamental or its long term potential. However, the market is incredibly efficient long term, where price action will follow fundamental. I don't need to chase the hyped tickers. And I don't plan to convince anyone to buy this stock. You have to do your own DD, as I dont offer Financial Advice! I'm enjoying the discount, when it is hated. or the legend Howard Marks, "discounted stock when it is not loved", yes OakTree capital owns $GRAB. 350-400m MTUs, 250-300m Subscribers are within achievable in 6-7 years or sooner. GRAB has the most resilient business model even during bad macro condition, it been through worse like slow growth 2018-2019, Covid, 2022 mad global inflation, and the last 40 days. I know many gonna say, Mike is just out here pumping his stock. Well if that was the case, I wouldnt write more than 1,000 threads on this company, and most of them are very long. Currently, Grab has 50.5m MTUs. Here are some of the keys MTUs could accelerate to 350-400m within 5 years. Ads revenue will be much higher at 350m-400m MTUs! A. FoodPanda recently sold Taiwan operation to $GRAB, but they are still in 3 markets competing with $GRAB(Malaysia, Singapore, and Philippines). Yes they are losing market share, drivers, users and merchants to $GRAB. FoodPanda is likely to exit these 3 markets as they have $5.44 billion debt and $2.9B in Cash. This would effective send $GRAB to be monopoly: ~Malaysia= 93-95%+ Market share ~Singapore= 94-95%+ Market share ~Philippines= 90-95%+ market share Foodpanda will likely to focus on these market to gain more operating leverage, and reduce debt ~Bangladesh(~70% market share) ~Pakistan(60-65% market share) ~Hong Kong(#1 player) And yes, it is entirely possible for Foodpanda to sell Bangladesh, Pakistan to GRAB later on like Taiwan. B. $GOTO(Indonesia) Mobility/Delivery negotiation is ongoing with $GRAB. No denial so far from management unlike the last 5 years. If we are using FoodPanda Taiwan sale price, $GOTO Mobility would only be worth $740m-$1B price tag. This would make $GRAB 90-95% market share in Indonesia and add: ~30m+ MTUs ~3.1m+ drivers ~20m+ merchants C. GrabFin is expected to accelerate MTUs, as it would allow 70%+ unbanked population or ~500m to access financial services from digital banking, insurance, payments, loan, GrabCoin(reward 3-5% on spending), and Wealth management. Users are now able to borrow money if they use $GRAB services or Cash Loan. The interest rate is 2.99%/month, which is much lower than loan shark or high interest lenders from 12-30% per month. This 2.99%/month will probably send Loan Book to above $2.5B or potentially $3B by end of 2026. D. Secret Weapon-Affordability Focus on Products ~Group Ride: Share a ride with up to 4 people on similar routes; AI coordinates pickups/split payments. Saves up to 40% on fares vs. riding alone ~Grab More: Add items from a second nearby merchant to your food/grocery order with no extra delivery fee, no minimum order, and no small-order fee. ~Grab AI Assistant/GrabGPT: Free ~GrabMaps open for consumers: Free and more accurate than GoogleMap.Grab can generate significant revenue off GrabMaps ~Travel Bundle/Package at discounted rates ~Paylater: with no interest if paid on time ~Cash Loan: at much lower interest than all banks/lenders ~Low cost insurances ~GrabUnlimited subscription for all services at discounted rate, priority support, additional rewards, and it should pay for itself within 2-3 uses. ~GrabCoins: earn 3-5% back when you spend like our credit card here, to increase more frequency ~GrabStays: Budget-friendly deals on Hotels/Motels with flexible cancellation. If you look at GMV/MTUs below, 2025 was the year that "Secret Weapon" strategy is working, as users are spending more on the SuperApp. It is not the SEA's Uber, it is not just Wechat-Financial like, It is not just Amazon ads/subscription like. It is a combination of all, to embrace Bottom of Pyramid, that longer term extend to 5 billion people TAM. While @AnthonyPY_Tan has ambitious goal, I set my projection to 700-800m TAM. I will adjust when we expand to more countries. Not Financial Advice!

English

$GRAB| $7 PT| Buy Rating 📶

"Barclays analyst Jiong Shao maintains Grab Holdings (GRAB) with a buy rating, and maintains the target price at $7."

Mike@MikeLongTerm

$GRAB is worth so much more long term 🧵 Once u understand what the team is trying to build, it should worth so much more long term than today. Many are saying why shoud I bother when other long term like $AMD $PLTR $TSLA $HIMS $XYZ are already high quality. Well, this is a new long term since Feb 2025, and I got to average down significantly(im green now). And my long term bull thesis is 30x more from here($16.7B MC) or roughly $8-$9B rev a quarter. The other high conviction long term already have significant position sizing. I dont expect Grab to ramp up massive YTD return, it can take time for the thesis to play out. Stock price follows sentiment, not Fundamental or its long term potential. However, the market is incredibly efficient long term, where price action will follow fundamental. I don't need to chase the hyped tickers. And I don't plan to convince anyone to buy this stock. You have to do your own DD, as I dont offer Financial Advice! I'm enjoying the discount, when it is hated. or the legend Howard Marks, "discounted stock when it is not loved", yes OakTree capital owns $GRAB. 350-400m MTUs, 250-300m Subscribers are within achievable in 6-7 years or sooner. GRAB has the most resilient business model even during bad macro condition, it been through worse like slow growth 2018-2019, Covid, 2022 mad global inflation, and the last 40 days. I know many gonna say, Mike is just out here pumping his stock. Well if that was the case, I wouldnt write more than 1,000 threads on this company, and most of them are very long. Currently, Grab has 50.5m MTUs. Here are some of the keys MTUs could accelerate to 350-400m within 5 years. Ads revenue will be much higher at 350m-400m MTUs! A. FoodPanda recently sold Taiwan operation to $GRAB, but they are still in 3 markets competing with $GRAB(Malaysia, Singapore, and Philippines). Yes they are losing market share, drivers, users and merchants to $GRAB. FoodPanda is likely to exit these 3 markets as they have $5.44 billion debt and $2.9B in Cash. This would effective send $GRAB to be monopoly: ~Malaysia= 93-95%+ Market share ~Singapore= 94-95%+ Market share ~Philippines= 90-95%+ market share Foodpanda will likely to focus on these market to gain more operating leverage, and reduce debt ~Bangladesh(~70% market share) ~Pakistan(60-65% market share) ~Hong Kong(#1 player) And yes, it is entirely possible for Foodpanda to sell Bangladesh, Pakistan to GRAB later on like Taiwan. B. $GOTO(Indonesia) Mobility/Delivery negotiation is ongoing with $GRAB. No denial so far from management unlike the last 5 years. If we are using FoodPanda Taiwan sale price, $GOTO Mobility would only be worth $740m-$1B price tag. This would make $GRAB 90-95% market share in Indonesia and add: ~30m+ MTUs ~3.1m+ drivers ~20m+ merchants C. GrabFin is expected to accelerate MTUs, as it would allow 70%+ unbanked population or ~500m to access financial services from digital banking, insurance, payments, loan, GrabCoin(reward 3-5% on spending), and Wealth management. Users are now able to borrow money if they use $GRAB services or Cash Loan. The interest rate is 2.99%/month, which is much lower than loan shark or high interest lenders from 12-30% per month. This 2.99%/month will probably send Loan Book to above $2.5B or potentially $3B by end of 2026. D. Secret Weapon-Affordability Focus on Products ~Group Ride: Share a ride with up to 4 people on similar routes; AI coordinates pickups/split payments. Saves up to 40% on fares vs. riding alone ~Grab More: Add items from a second nearby merchant to your food/grocery order with no extra delivery fee, no minimum order, and no small-order fee. ~Grab AI Assistant/GrabGPT: Free ~GrabMaps open for consumers: Free and more accurate than GoogleMap.Grab can generate significant revenue off GrabMaps ~Travel Bundle/Package at discounted rates ~Paylater: with no interest if paid on time ~Cash Loan: at much lower interest than all banks/lenders ~Low cost insurances ~GrabUnlimited subscription for all services at discounted rate, priority support, additional rewards, and it should pay for itself within 2-3 uses. ~GrabCoins: earn 3-5% back when you spend like our credit card here, to increase more frequency ~GrabStays: Budget-friendly deals on Hotels/Motels with flexible cancellation. If you look at GMV/MTUs below, 2025 was the year that "Secret Weapon" strategy is working, as users are spending more on the SuperApp. It is not the SEA's Uber, it is not just Wechat-Financial like, It is not just Amazon ads/subscription like. It is a combination of all, to embrace Bottom of Pyramid, that longer term extend to 5 billion people TAM. While @AnthonyPY_Tan has ambitious goal, I set my projection to 700-800m TAM. I will adjust when we expand to more countries. Not Financial Advice!

English