FCF or Bust

7K posts

FCF or Bust

@CapStructKing

Style Agnostic | Capital Structure Agnostic | Never Long Frauds | 90% Indexed with 10% Fun Money | Mostly retweets, not investment advice

Washington, DC शामिल हुए Mart 2021

4.1K फ़ॉलोइंग579 फ़ॉलोवर्स

With oil elevated for the next year… outside E&P or healthcare indon’t see a lot of place to hide…

Bob Elliott@BobEUnlimited

Brent curve is pricing in a $100 average oil price for the rest of the year.

English

FCF or Bust रीट्वीट किया

FCF or Bust रीट्वीट किया

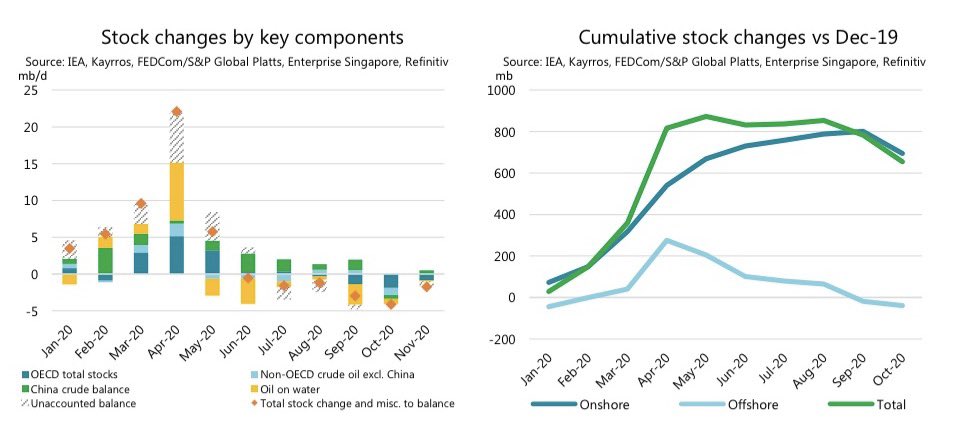

In 2020, global oil inventories saw a max build of ~820 million bbls.

By the middle of next week, production shut-in will reach ~12 million b/d.

In 56 days, we will have lost ~820 million bbls (includes shut-in since March 5).

English

@MRatable If I had to guess, they’ve got stuck assets so can’t take advantage of spot surging and spot tanking rates might actually be lagging behind how hard bunker fuel rates are surging.

English

@taobanker Better question is Oracle vs SoftBank on OpenAI IPO upside.

English

@Franckycfc @TheTranscript_ Guessing from the JPM Industrials conference this week

English

@TheTranscript_ Hello @TheTranscript_ ! Can you let us know which event was this extracted from ? Thanks .

English

$APD Air Products and Chemicals CEO this week: Limited helium inventories offer only weeks of supply

"We have some inventory. You're talking about, you know, high single digit number of containers. That can help the industry. I think that all the competitors do the same. I think that will help the industry for a period of few weeks. If you go for months, you know, the inventory, you know, really will be consumed...I think you can find information on the size of the cavern, the theoretical size of these caverns. How much is inside the cavern is something that we only know for ourselves, right? We have no clue of how much our competitors have in their caverns"

English

@yenoms Might as well just buy some 3 month out low vol OTM calls for soft deltas on both.

English

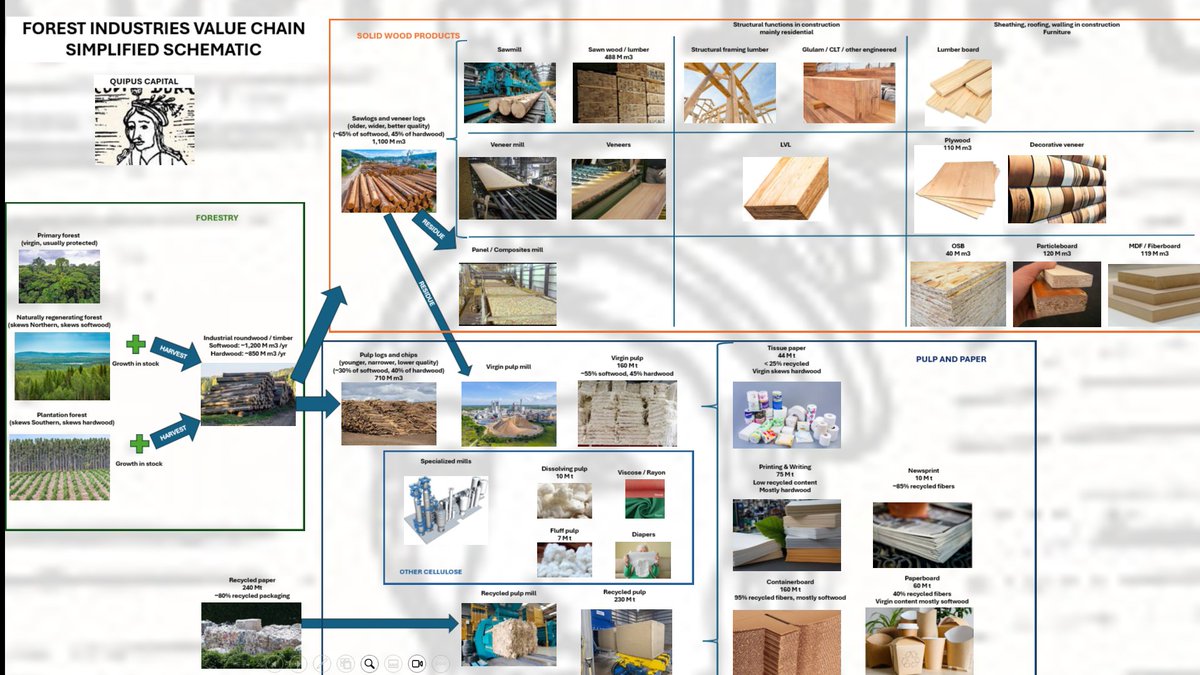

@QuipusCapital Like it! Will you also be covering the rest of the cellulose products (acetates, carboxymethyl, microcrystalline, etc.)?

English

A simplified schematic of the value chain in forest industries. Part of an upcoming primer.

What do you guys think? Anything missing?

English

@taobanker You can calculate a risk-neutral option-implied probability distribution function for stocks and figure out where to press bets vs mental price targets.

English

@taobanker You are unironically better off buying $CALM for the same underlying exposure.

English

@kjnkjp True, crackers need a minimum 60% operating rate so likely shut down before feedstock gets physically depleted. Gonna get real messy past that point.

English

@CapStructKing yeah, but utilization at crackers comes down prior to naptha depletion -> prices go up -> PE producers see spreads go down -> reduces utilization -> operating leverage starts reversing.

English

"resin spread" (ethylene - naptha) is the underlying KPI of the entire industrial sector, and Japan only has a 2 month stockpile of polyethylene. I.e. once crackers reduce output due to margin destruction, you start seeing auto and electronics shortages thereafter.

English

FCF or Bust रीट्वीट किया

This is bad, @DavidDTawil. Yes, they are stuffing it more now.

On December 23, 2025, we warned that private credit's new risk dump is retirement accounts and consumer credit.

If you have missed that, you can read it now here:

contrarianunicus.substack.com/p/private-cred…

David D. Tawil@DavidDTawil

Are we still considering stuffing retail investors, 401ks, etc with #PrivateEquity and #PrivateCredit? That idea has got to really look appealing right now.

English

FCF or Bust रीट्वीट किया

Gm and happy Friday folks. For those that enjoyed last week's poast, this dive into the supply chain knock-on effects dropped last night and should be a fun read.

Most of it is free.

Some single names got mentioned as a pointer on how to map this, not as a reco to buy them.

EconstratPB@EconstratPB

There is something bigger at risk from the Hormuz shock. A regime shift. Includes a roadmap and timeline to navigate this shift, and what to watch out for. As with Tuesday's note, most of it is free so have a read and pls like and RT if you found it useful. 🙏

English

FCF or Bust रीट्वीट किया

Deep dive into $STVN

High-quality compounder? Yes.

- Clear moat

- Strong revenue growth

- Credible margin expansion story

We believe this is about as complete a piece of work as you can get on @StevanatoGroup, enjoy!

English

FCF or Bust रीट्वीट किया

I don't really see a lot on FinX offering advice or even a discussion of hedging, portfolio construction and risk management approaches. However, I do see a lot of renting single name idea conviction, and then hating on anyone who disagrees with pushback or looking at the idea through a different lens re factors, how does it fit into a portfolio, etc. Then the pile-on begins...and one losing idea out of fifty gets quoted like it defines the whole body of work. Nobody really asks about that position and how it is sized or fits into someone's portfolio or what the mandate is... Nobody really asks about trade structures and/or about the hedge. Let's dig in...

Hedge the Damn Book. Or At Least Your Most Convicted Positions.

People love to say they don't need to hedge.

"The valuation is too compelling." "I'm a long-term investor." "Tail hedges never work." "I will just buy more."

Fine. Keep telling yourself that while you watch six months of alpha evaporate in three weeks because you were too proud, or too lazy, to protect the book or a large sector concentration.

Here's what nobody tells you: hedging isn't one thing. It's a toolkit. And most people have only ever picked up one tool, and they aren't even really consistent in its use.

The hedge book budget. Start here:

Before anything else, you need a philosophy. Mine is simple: I start every year already down. Whatever the hedge book costs me — call it 1.25-1.5% of NAV (lotta variables to consider here to come up with this figure range re net/gross/'n'/bull-bear beta/etc). I'm not trying to predict when the correction comes with this approach, but I am buying the right to not care when it does. [Let me know in the comments, how you hedge or have questions on how to think about establishing a hedge book budget for your portfolio.]

That budget gets deployed across structures depending on where vol is. Down 5/20 put spreads when skew is rich and I can finance cheaply. Down 10% outright puts when I just want clean delta. Down 30% puts sitting on the shelf quietly when vol is at the floor and the market is pricing perfection.

And here's the discipline part: I'm not married to any single strike or expiry. I'm looking at the vol surface. Is there skew I can exploit? Can I do a 1x2 put spread and get the structure for near zero? Can I collar a concentrated position and use the premium to buy something else? The market tells you where the cheap protection is. You just have to look. [I have a tool for this that I have used, and make tweaks to for 20+ years.]

The other piece: which index actually correlates to your book? Running a small cap value book and hedging with SPY doesn't make a lot of sense... Know your beta. IWM, QQQ, or even sector ETFs might actually move when your book moves.

Portfolio-level hedges: the game theory of net exposure:

If you're running 150-200% gross with 30-40% net long, your hedge book has a job to do. It's not just protecting downside, you are managing the delta of your portfolio dynamically. As the book rallies and gross goes higher, you need to consider a systematic way to adjust as well as some improv. [Separately, if you manage a fund structure and/or have rebalancing, this is an additional consideration.]

Think about this through the lens of scenarios, and unless you have a track record to back it up, I would tone down the predictions. What does my book do if SPY goes down 10% in a straight line over two weeks? What does it do if vol spikes 30% overnight from some exogenous shock nobody saw coming? What if software sells off 15% and small cap industrials rip?

These are stress tests that are pretty easy to simulate. (I run 6 scenarios that are particular to how I manage dough, but I think 4 core simulations should work for most people with an error factor embedded). Net/net, your hedge book needs to absorb some of that damage before it hits the P&L.

Position-level: risk of loss hedges (I don't think I have ever seen this really discussed outside of my feed on Twit)

This is where I see in lights, ego kills people, and you know who you are...well, candidly, you prob don't!

"The risk/reward is down 2 to make 15. I don't need to hedge it."

So the entire market — every sell-side analyst, every long/short fund, every quant model — has mispriced this thing, and you figured it out. Got it. With a snapshot multiple and a management team you've met a few times and IR guy who calls you back the same day.

The way I see it is this: If the upside is that good, buying a down 15% put (this is just an example) on the position costs you almost nothing relative to the expected gain. The most frustrating losses in investing aren't being wrong — they're being right and not being able to hold it because the drawdown got there first or the best the stock could manage over the event path is to recover that downdraft or a bit more, but it never met the up 15 from your investment starting point...now you are extending your duration, thesis has drifted, but you have conviction!

Risk of fraud hedges. The smart money already knows this. (Again, I have never seen this discussed on FinX):

Next time you see a social media account screaming about unusual options flow — 40% OTM puts on MSFT with 5 months to expiry, 50k VIX calls for next month, 100k end-of-year calls on TSLA that are 40% out of the money — stop thinking informed buyer.

Those are center book risk-of-fraud hedges at multi-manager platforms.

When every pod manager in the building is leaning into the same trade, nobody's calling a meeting to discuss the overlapping stock position. The center book just goes out and buys 40,000 contracts of a down 30% put on the crowded long at 25 cents a piece. The "unusual options activity" content creators are selling you a story. Well, the actual story is risk management at the institutional level.

The dirty long basket. Simple, underused, effective:

Some of the cleanest hedging I've seen isn't in derivatives at all. A portfolio manager who identifies the same factors across a dirty basket of highly shorted names — high short interest, similar sector exposures, same macro sensitivities — and runs that basket long against their alpha shorts is doing something most people overlook.

The logic is simple: your alpha shorts are idiosyncratic and hard to hedge individually. The dirty long basket gives you exposure to names that will rip if the market squeezes or rotates, which is exactly when your short book is most at risk. You're not trying to make money on the basket. You're buying yourself time and absorbing the pain that would otherwise force you out of your best short ideas at the worst possible moment.

You can do it in common stock. You can do it in options. Rank-order your universe and consider whether a dirty long basket gives your short book the room it needs to work. I like to use this opportunistically from time to time (like during summer months, where I don't like to have a lot of single name shorts.

Position blocks and the 13F (see Inside the Mind of Mojo):

A lot of institutional books aren't running singles. They're running position bundles, which entails a long position, sector peer short(s), factor neutralizer(s), maybe a correlated derivative. The goal isn't to make money on every leg. The goal is to isolate the alpha from the noise. I call this teasing out the alpha.

Sector books do this constantly. They rank their universe, run factor exposure reports, and surgically neuter the parts they don't want so the only thing left is the stock-specific edge. If you're reading 13Fs and wondering why a manager has a weird combination of longs and shorts in adjacent spaces, that's usually what's happening. The hedge is embedded in the structure.

When funds neuter the entire block via long fulcrum, short the sector, short the factors, et al, the goal is for the position to look on paper (risk mgmt. tear daily tear sheet) like a boxed trade. Long XYZ, short XYZ equivalent. Essentially flat to the market on paper, while the actual expression is the gap between the long and the hedge package.

This is exactly how some of the more reputable activist firms operate, particularly the ones who create their own catalyst inside a defined duration pressure cooker. Market observers see the 13F, watch the stock pop 15% on the disclosure, watch it give it all back, and declare the trade a failure. This framing misses the entire structure. What did the sector comps do over the same period? If the long went up 15% and the shorts barely moved, the manager just added to their shorts after the pop, resetting the box at a better level, now net neutral or even slightly short the sector and layering options on the fulcrum to remove a meaningful chunk of the remaining downside, locking in a sizable gain. The gross P&L on the long looks flat to the outside world, but the actual net P&L on the structure is a different conversation entirely.

Many sophisticated funds go further and use factor tools like Barra to identify and manage specific risk dimensions re momentum, beta, size, short interest, liquidity, growth, yield, management quality. Others work with their prime broker to construct custom baskets that hedge a specific bundle of exposures more precisely than any off-the-shelf ETF can. The custom basket is 'more' surgical but carries its own basis risk. Where you land depends on how much of your gross you can dedicate to the hedge and how much precision the book actually requires.

Prime brokers also offer synthetic structures worth understanding and knowing they exist even if you never use them. These include knock-in/knock-out puts and calls triggered by conditions being met, and conditional parlay structures where the payoff depends on an order of operations. These go in and out of favor, but when sized correctly they can insulate a significant amount of negative gamma in ways that vanilla options can't or at least come up short...

The broader toolkit:

The tools exist for every situation. A few worth naming that don't fit neatly into the categories above:

Volatility as an asset class. Long VIX calls or UVXY as a pure convexity play when vol is cheap. A separate trade from directional index puts, and often a better one when the risk is a sudden spike rather than a grind lower. I am not really a fan of these after spending time with market makers who print money trading this asset class.

Rate hedges. If the book has meaningful exposure to rate-sensitive longs such as utilities, REITs, long duration growth then perhaps treasury futures deserve a look. Rising rates have a way of repricing entire sleeves of a portfolio simultaneously.

FX forwards and options. Hedge your FX, otherwise you are adding another bet to the trade.

Capital structure hedges. Long the convert, short the equity. Or CDS (have written about this before at Inside Mojo) when investment grade spreads are at multi-year tights and the convexity is better than what SPY puts offer. Credit often moves before equity does in stress scenarios, which means you're getting paid before the stock goes down.

Calendar spreads and ratio structures (I have mentioned these trade structures many many times). Cost-reduction mechanics that apply across most of the above. If a structure is too expensive outright, there's usually a way to finance it. If you read my tweets, you know that I love using calendar spreads around defined event paths to get involved in a situation, where when I do this right I come out long equity vs long puts, then I have real built in protection on something the world think is so idiosyncratic a hedge isn't needed.

The toolkit is large. Saying no hedge fits the situation is almost never true (even in appraisal cases, hedges work!). Usually what's missing is the willingness to look and go deeper.

There is no "right way." But there is a starting point.

I know funds that have managed billions for two decades and have never run a meaningful single-name short book. Their edge is finding great businesses and sizing them correctly and risk managing them re if something changes, they hit the eject button (they only buy on the way down if numbers step function still improving and DO NOT ANCHOR TO VALUATION). An alpha short book of single names/themes would just introduce noise to their process and approach. Their hedging is structural, systematic, and for most long-biased equity funds, it's the right answer.

Here are some different approaches / blends that are worth reviewing:

The sector-ETF approach:

The portfolio is organized by sector. Each sector PM or senior analyst has a conviction level, hot or cold, overweight or underweight relative to the index. That conviction maps directly to a net long target for that sleeve, and the hedge instrument is a sector ETF. This approach does require a single PM/risk manager to make some difficult decisions on behalf of the sector PM/sr analyst, re he is going to have to reduce your names from time to time despite your conviction...for the analyst I would learn to not take this personally, and perhaps when you run your own firm one day, you will find what works for you...

Tech is 30% of the S&P and you're running 40% long tech. That's a real overweight. You hedge down to 50% net long using QQQ, IGV, or SMH — whichever actually correlates to the names you own. If a sector is underweighted relative to the benchmark, you might run it near 100% net long because the beta is low enough to live with.

The result: every sector has a net long target that reflects conviction, managed dynamically with index instruments. No single-name short risk bleeding into the long thesis. No analyst ego wrapped up in a short that's moving against them.

This model works at $500mn and it works at $5bn. It matches what most long-biased funds actually tell their LPs they do.

There's a version of this where the CIO reads the macro regime and rotates between ETF hedges and single-name shorts depending on whether correlation or dispersion is the dominant environment. And there's the full single-name short book, pod-style, where analysts rank their entire universe and the shorts come from the bottom of the list, with net exposure calibrated by hit rate, tenure, and slugging percentage — and the central hedge book charged to every PM whether they want it or not, because whoever's name is on the door is responsible for what happens when everything blows up at once. Both are real models. Both have produced long track records. If there's interest in either, drop a comment and I can probably add more color.

One important caveat on scale:

The sector-ETF framework assumes you have enough AUM that return optimization and risk management are the primary objectives. Sub-scale changes the math entirely.

If you're running a smaller fund without a large anchor investor or family office cornerstone giving you runway, the priority isn't risk-adjusted returns. It's marketability. You need returns high enough to get into the conversation with allocators who have minimum AUM thresholds and track record requirements, and you need to get there before you run out of time.

Unless you have a prior track record of short selling that genuinely adds to P&L rather than drags on it, don't force the short book. Have some book-level hedges in place, but lean on risk of loss disciplines on your largest positions — defined stops, position-level risk parameters that save you from yourself — and flex your cash position as a first line of defense. Sometimes the best hedge is just not being fully invested when the conviction isn't there.

Focus hard on N. A concentrated book in your highest-conviction names, sized right, is what generates the return profile that puts you on the map. Over-hedging a sub-scale fund is a slow way to die. And all of this still has to reflect the mandate — which should be an honest expression of what you've actually proven you can do, not what sounds good in an LP deck.

It's all a game. The rules just depend on where you are in the lifecycle.

Before the hedge book: the mandate

None of this works if it doesn't match what you told your investors you do.

The hedging conversation is always downstream of a more important one: what is this fund actually trying to do? What's the investable universe? Where does the edge come from on the long side, and does it transfer to the short side? The funds that drift from their stated process — that say systematic sector hedging and then start freelancing with single-name shorts because the CIO has a feeling — those are the ones getting difficult questions from allocators. Build the hedge book to match the mandate, not the other way around.

Let's discuss and name the excuses:

"Valuation is my hedge." A cheap stock can get cheaper, stay cheap for years, or get cheaper right before it gets taken out at a premium you never got to enjoy because you stopped out first (or perhaps you should have a stop for a portion of the position so you don't bleed).

"The risk/reward is so good I don't need a hedge." The r/r might look exactly right on paper, but if earnings revisions aren't improving, aren't inflecting, aren't showing any rate of change that justifies the multiple you're anchoring to, then the r/r is probably off. Let's just get this out there...variant view is one of the most over-used term in investing. A cheap multiple on deteriorating numbers is just a value trap with better slide deck language. Unless you have a path to buy the entire company, a board seat to drive the change yourself, or an activist position with real leverage over the outcome, you are a passenger. Don't be stubborn!

"The event path is too idiosyncratic to hedge." This is almost always said by the same person who then wants to size the position up very large. If it's too complex to hedge then (just my opinion) it's too complex to concentrate. If you're concentrating, at least explore finding the hedge and then size it. There is always a trade structure to consider: a put spread, a collar, a correlated proxy, a partial synthetic from your prime broker. The tools are all there.

Two of those excuses are laziness. One is ego. None of them are good enough when you're managing other people's money.

Hedge the position. Hedge the book. Or size it like you know you can't.

Haters...I will be waiting for you in the comments! Let's go!

English

@Mr_Neutral_Man There’s been a lot of excess tire production, leading to excess inventory to work through. Bridgestone in Japan also seeing the same dynamic. Probably takes a while to see benefit to carbon black.

English

@CapStructKing I've been thinking through $OEC and $CBT and how they may benefit or get hurt from all of this

This is basically capturing soot from burning of hydrocarbons and China built and exported a lot of excess capacity and dumped tires in NA

English

Been slowly adding to our O&G exposures to hedge out a nasty 1970s oil shock. Not fully committed yet, w/ each escalation, ramping up our exposure. Would love ideas

$SU - Canadian oilsand low cash cost

$DINO - Inland refinery/lube

$XOP - Calls

$JOY.TO - Small cap E&P

English

@Mr_Neutral_Man Chinese TiO2 is usually sulfide-method and Western TiO2 is chloride-method, so less sulfur exposure there. Chemours took up some price in their TiO2 business. Been a tough demand market with a slowly tightening supply picture. $TROX and $KRO also do TiO2.

English

@CapStructKing Someone had mentioned that sulfur production is way down and some mention of Titanium dioxide

Probably worth the time to think through what Chinese over capacity chemicals/products that US producers can all sudden compete again

Reduced antidumping = better for US

English