पिन किया गया ट्वीट

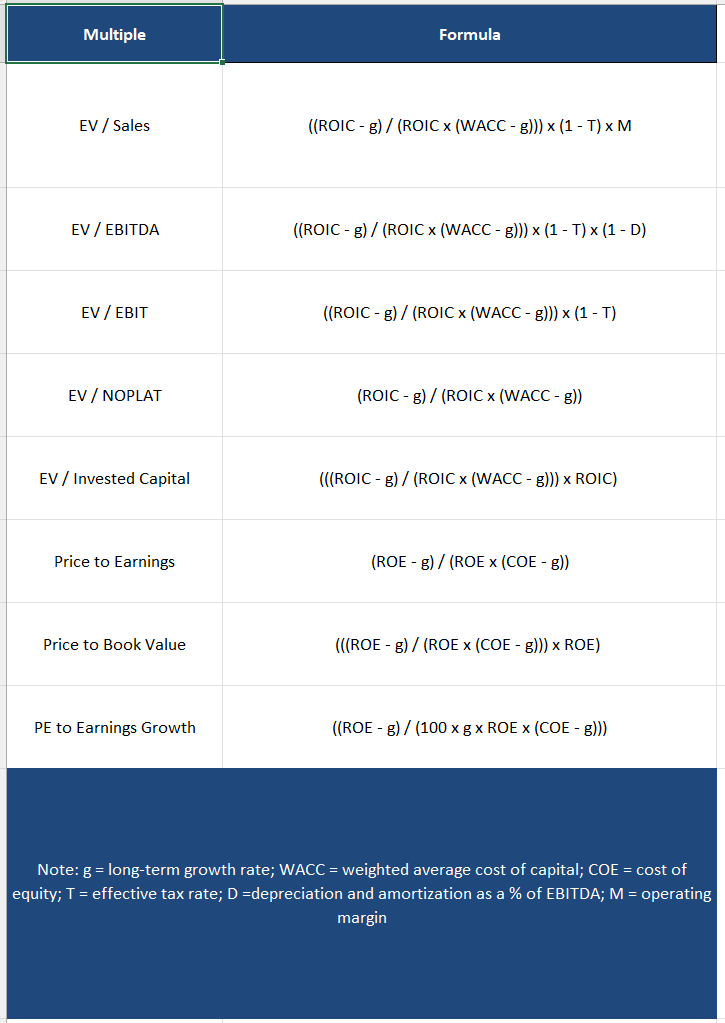

Using a quantitative framework to understand which factors have the greatest impact on valuation multiples

Important quantitative drivers of a valuation multiple are return on capital, cost of capital, growth, and duration of growth. From a quantitative perspective, it is important to understand which factors will have the greatest impact on a company's valuation multiple - What is the impact to the multiple from a 1% change in the return on capital? What is the impact from 2 points of long term growth to the multiple? Target multiples can be derived based on these underlying drivers using the formulas below.

The formulas below assume that value-adding growth will continue perpetually. This is a simplifying assumption but more realistic two-stage versions of the formulas can be used which incorporate an initial growth period followed by a terminal period.

Comment below if you'd like the excel file with the one stage formulas, two stage formulas, and their derivations.

English