Albert ⚔️ ✨OVERWORLD STONE🐦⬛🪨 $MOJO

2.4K posts

Market has pico bottomed and we are headed to 125,000$ in next few months probably by November

Strap in !

English

@Nishant_Bliss Please tell coins in public too

English

Casually speaking to someone who has a record of catching 10-20x.

Had to blur the name because of he doesn’t want his expertise to go public.

Alts 10-15x

English

@Agonybeard @DegenSensei Same bruh tell me best range

English

When are we buying a ton of spot $CRCL @DegenSensei ?

I won’t miss it agane

English

@nirajhodler We believe in you boss and still bullish on elizaOS as they are still inclined with AI agents

English

The buy anything and make money era is over.

AI & agents will be where life-changing money is made this cycle.

🧵 THREAD

1/

I’ve been talking about this for months, even years.

Now top people in tech even the CEO of NVIDIA are validating the same thesis.

Watch this 👇👇

(All-In Podcast)

youtu.be/gwW8GKwHB3I?si…

2/

Decentralized compute → $AKT @akashnet

Did 40x from my call.

And as compute demand explodes

this still looks like it has another massive run in the next cycle.

3/

Decentralized AI → $TAO

Did 18x from my call.

Still one of the strongest contenders

for the biggest play of the next AI cycle.

4/

Now the next frontier:

Open-source agentic tools → @openclaw

I am already spotting multiple 10x runners

even in the worst market conditions.

5/

Let me be very clear —

The days are gone

where you could buy anything and make it.

6/

If you want life-changing gains:

• You need to work 10–18 hours a day

• Build real understanding

• Develop actual skills

• Follow the smartest people in the industry

7/

This cycle won’t reward laziness.

It will reward:

conviction, patience, and deep research.

8/

Most people will stay distracted.

A few will lock in.

Those few will win big. 🚀

NFA

YouTube

English

@Agonybeard @Pickle_cRypto lol, will it again chance around 40$ for accumulation if anyone miss?

English

Tagging @Pickle_cRypto on this post because he has muted the word $CRCL from timeline

It’s at 127.31$ right now what a savage stonk

( why should I suffer alone ? )

English

Buy as much as USDT or USDC you can, accumulate as much as you can, see you at ₹120.

English

Still expecting a not so great summer price wise , deep value pickups might come and I plan to significantly reduce my $BTC spot exposure when we tap mid 80’s before summer time

English

@Nishant_Bliss Bhai mere stock toh btado quantum wale

Italiano

Investing in quantum stocks right now is like investing in $NVDA in 2019.

English

Albert ⚔️ ✨OVERWORLD STONE🐦⬛🪨 $MOJO रीट्वीट किया

join @VitalikButerin cypherpunk warrior arc.

Please do if you really've any gratitude left for the space which has given you lot.

please watch this vid to understand the true side/lost meaning of crypto.

vid is in english.

English

@dave_pionex ser my account gets suspended as even after submitting the proof of funds it’s still not allowing me to withdrawal as ser please look into this matter

English

@aleabitoreddit @grok explain me above in

Short as summarize it

English

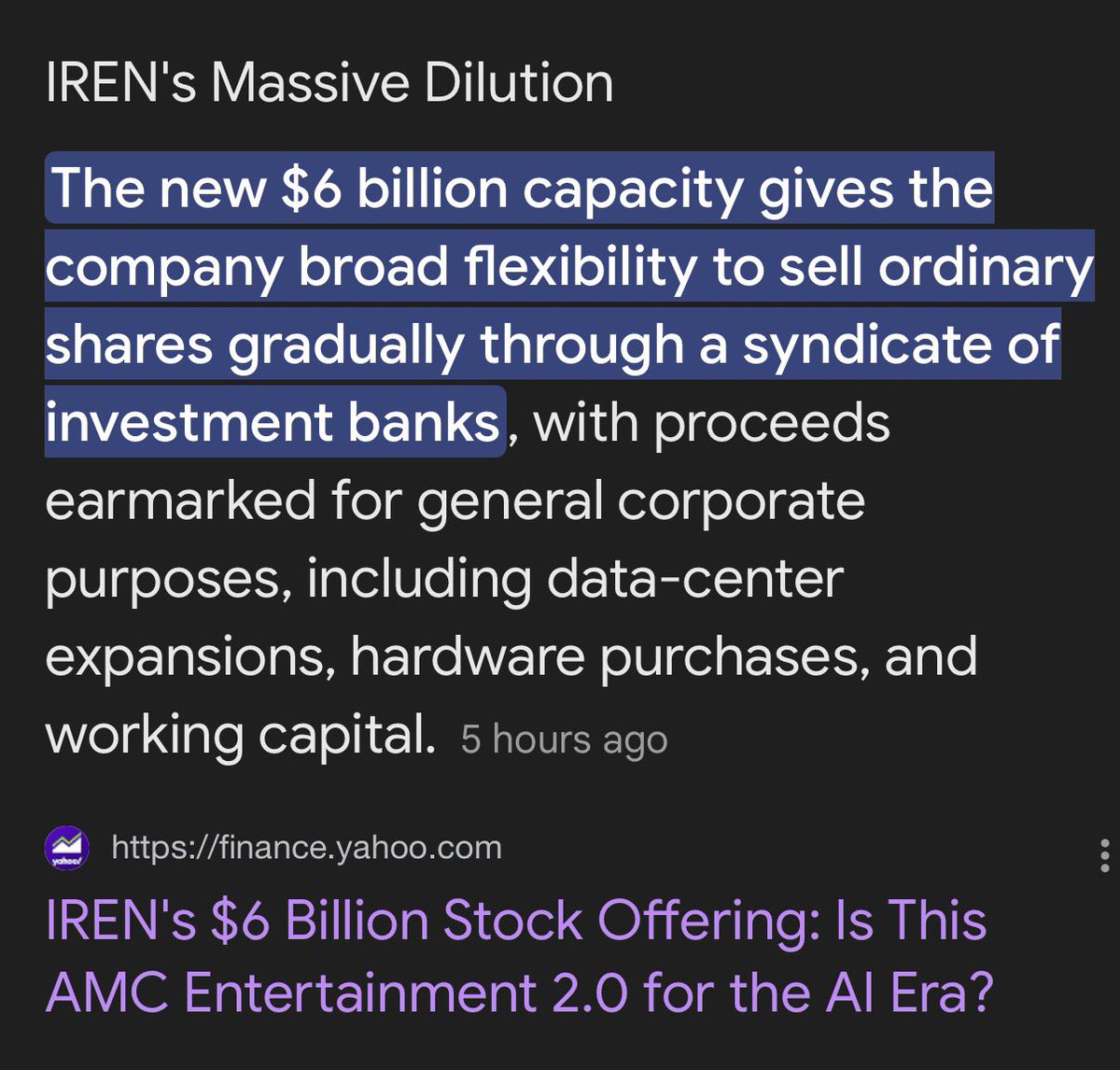

Most people on X make the mistake of getting married to a stock.

If your thesis materially changes with $HIMS or $IREN, so should your position.

If the bull case with $IREN last year was monetizing 3GW capacity through colo.

Then if the company:

-> inevitably dilutes you $6B off a $12.2B MC

-> sells those shares into the open market in every rally

-> pivots to GPU offerings

Your thesis has changed.

And it’s likely a time to exit to pursue more asymmetric opportunities.

If your thesis with $HIMS was that they’re the Amazon of healthcare.

But they get sued to oblivion by $NVO and the US gov. It’s respectable to exit.

But if the thesis is back online given $NVO dropping their lawsuit and partnering up, then there’s nothing wrong with going long again.

A lot of things change every month with catalysts or fundamentals.

If you’re still cheering on an inevitable $6B worth of new shares getting sold against your $IREN positions on every rally.

And your only qualifier is “Trusting in Management” like $AMC investors.

Maybe it’s a good time to ask yourself this:

Are you ignoring every red flag because you’re married to the stock?

Serenity@aleabitoreddit

I see zero compelling case to hold $IREN. Especially given the new $6B share dilution at a $12.8B marketcap. People will likely see that marketcap inflate to $20-$25B. But the value of their shares decrease over time. The risk reward is just not there anymore. Companies like $CIFR offer much more asymmetrical upside given their colo model for $AMZN and $GOOGL through Fluidstack. And companies like $NBIS offer much better diversification (robotaxis, clickhouse), derisked execution, and are well supported for capex. With $IREN, there’s no way to justify being diluted close to half the market cap and cheering that on. Even with a new hyperscaler deal there’s risk reward is just not there. I was bullish $IREN last year but sold it. As holders went from: -> 3GW capacity, asset lite, Colo model (was a fan of this) -> Buying GPUs for $MSFT and cheering on execution risks from the pivot (not a fan) Into -> Cheering on $6B of new share dilution + getting sold on the open market against their positions. (AMC bagholder territory) If you’re trying hard to justify why new ~50% dilution is a good thing sold against your positions and trusting in management: Sorry to tell you, that you’re now in the $AMC equivalent club for datacenters. There are much better longs out there.

English

English

Yes it’s the same with other stocks like $BMNR.

If the goal investors supported was to acquire 5% of $ETH supply and compound return through staking + token appreciation.

Then the company redirects $200M into a YouTuber’s chocolate bar company before even acquiring 5% of Ethereum.

Might be a good time to reconsider.

English

@StaderPro Pha is still aligned with the latest AI agents trend I believe it will survive

English

Albert ⚔️ ✨OVERWORLD STONE🐦⬛🪨 $MOJO रीट्वीट किया

@nirajhodler Cool, btw targets of how much minum and maximum mcap it can achieve?

English

English

English

Watch all my holes get destroyed by @JulesJordan and @ZacWildxxx in this INSANE double penetration scene 💣💥

Out NOW 😈➡️ angelawhite.com

English

@grok @aleabitoreddit Kindly explain above in more shorter and how much is he expecting from it @grok

English

Summary: KOSPI crashed 7.24% today (to 5791) on LNG price spike fears after Iran drone hit Qatar's gas hub, hammering Samsung (-9.8%) & SK Hynix (-11.1%) amid deleveraging.

He's conveying: This is a clear buying opp unlike 2022's energy+consumer crash. AI memory demand is insane & locked-in—hyperscalers will absorb costs, no oversupply. Revenue forecasts huge for '26-'27.

Can't-miss: AI arms race makes SK tech bulletproof; dip is overreaction, ops income will crush it.

English

Thoughts on the $EWY / KOSPI crash and whether it's a buying opportunity for Samsung/Sk Hynix:

This looks like a clear buying opportunity.

Especially as investors misunderstand that 2026 is not 2022 (Ukraine-Russia) conflicts.

AI has fundamentally changed the demand for memory, compared to the 2022 downturn in consumer electronics, where Samsung/Sk Hynix also footed opex costs.

The main catalyst for one of the largest single-day drops in Korean history was Iran drone striking QatarEnergy's Ras Laffan complex.

Qatar is roughly ~20% of the global LNG supply.

Results:

-> Dutch TTF (Euro Natural Gas): +46%

-> Asian Spot LNG: + 39%

-> U.S. Natural Gas: +4.16% (fine)

The LNG spike was the catalyst for the drop as South Korea is materially exposed as it relies on imported LNG.

Fearing this inflationary energy shock, investors aggressively dumped South Korean tech equities, combined with deleveraging of 10x Samsung/Sk Hynix.

Sending

-> Samsung Electronics down by 9.79%.

-> SK Hynix shares sank by 11.12%.

and the $EWY (KR futures) down 14.49% today.

Everyone is fearing the 2022 incident with Russia-Ukraine war increasing LNG prices, causing industrial electricity tariffs in South Korea climbed by roughly 70% after KEPCO stopped abosring losses.

In 2022 alone, Samsung's domestic facilities consumed approximately 28,000 GWh of electricity.

The tariff hikes added an estimated KRW 2 trillion (over $1.4 billion USD) to Samsung's annual operating expenses and over KRW 1 trillion for SK Hynix.

This unprecedented spike in operational expenses (OPEX) hit at the exact worst possible time.

In late 2022, the semiconductor industry entered a brutal cyclical downturn. Post-pandemic demand for PCs and smartphones plummeted, leading to a massive oversupply of DRAM and NAND flash.

However, 2026 is completely different:

Compared to 2022 that faced increasing energy costs during a downturn:

AI demand for memory is completely unprecedented. On the 27th, there were reports of DRAM hikes again from Samsung/Sk Hynix.

Demand for NAND prices from $SNDK have been so high for capacity allocation that they've been taking 3 year pre-orders in advance.

There is no end to demand in sight, and no relief way until 2028.

Comparing this to 2022, where consumer segments for laptops and smartphones were already facing a downturn, memory makers could not pass on the costs (and tanked opex bill). That caused a major correction last time.

Because the global AI chip shortage is so acute in 2026, they will seamlessly pass their inflated utility bills down the supply chain.

Because supply is severely constrained, Samsung and SK Hynix dictate the market terms. Big Tech hyperscalers (Microsoft, Meta, Google, Amazon) are locked in an AI arms race. They are highly price-insensitive right now and prioritize securing volume over haggling.

As a result, this looks like a clear buying opportunity, especially as projections range from:

Morgan Stanley | Macquarie on Samsung

2026: ~$182.0B USD vs. ~$210.8B USD

2027: ~$235.1B USD vs. ~$333.7B USD

Morgan Stanley | Macquarie on SK Hynix:

2026: ~$132.9B USD vs. ~$190.5B USD

2027: ~$167.0B USD vs. ~$312.8B USD

The selloff looks like an immediate de-risking from fears over 2022 Ukraine-Russia-conflicts, combined with extreme leverage from 10x instruments.

But unlike 2022, where laptops and consumer demand were already facing a downturn and LNG spikes caused Samsung/SK Hynix to foot the bill:

This time it's passed onto hyperscaler costs because demand is too high.

People always compare KOSPI to silver, but the difference is one has whopping operational income, where in a bull-case scenario, 2 years of income alone would exceed their market cap of companies like SK Hynix.

The drop on Samsung/Sk Hynix looks like a clear buying opportunity as their operational income will likely blow past any short term volatility.

English