Tweet Disematkan

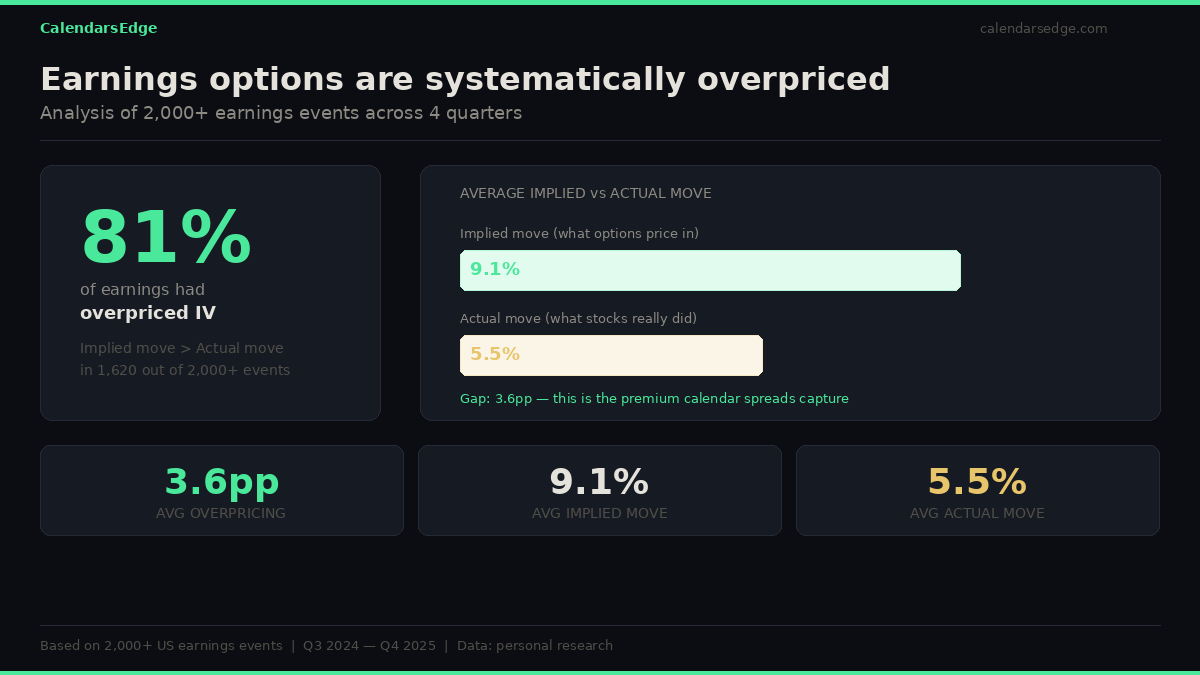

I've screened 2,000+ earnings events over 4 quarters.

In 81% of cases, options overpriced the move.

The average implied move was 9.1%.

The actual move? Just 5.5%.

That 3.6pp gap is real money — here's how to capture it.

English

CalendarsEdge

51 posts

@CalendarsEdge

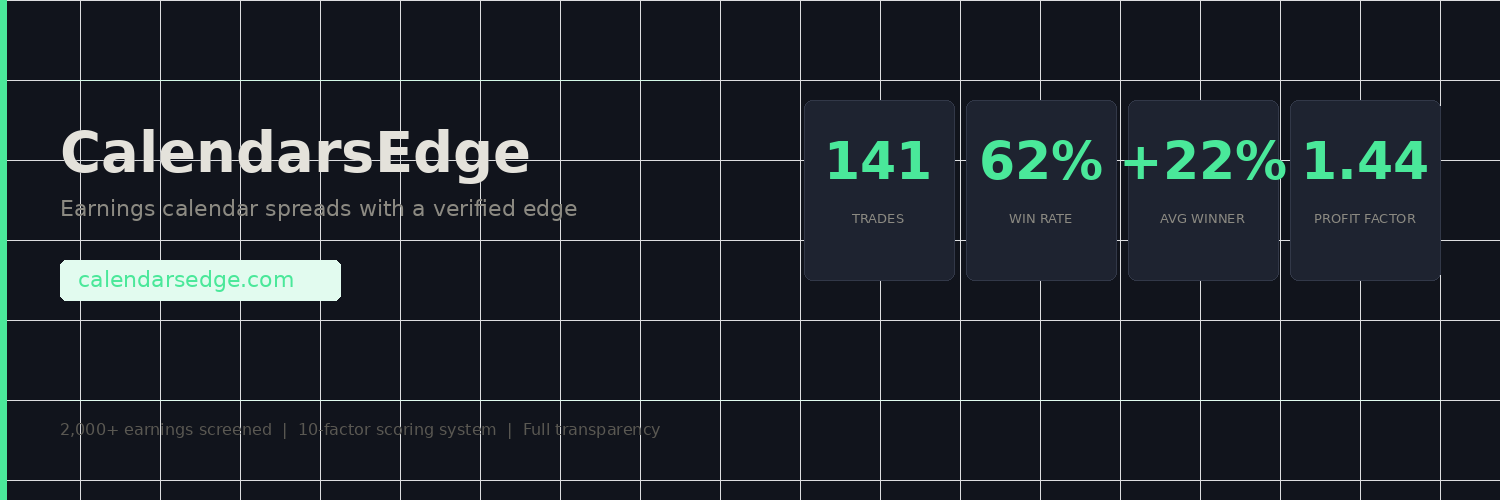

Earnings calendar spreads. Avg winner +22% ROI overnight. Daily scans during earnings. Track record: https://t.co/O1zTL6rvVl

Former SpaceX astronaut Garrett Reisman reveals the single prism Elon Musk runs every major decision through "He measures pretty much every major decision by whether or not it brings the day when we have a self-sustainable colony on Mars sooner or later" "That's the prism by which he makes every single decision he makes" "He's got an idea and he'll keep pushing, and he gives us aggressive timelines that we have to work to" "We work really hard to try to meet them. It's hard when you're doing stuff that's this complicated to predict exactly how long it's going to take" "We end up falling a little bit behind, but we do our best"

Locked and loaded on $APLD ⚡️ Just added 1,000 shares and sold the April 17 Covered Calls to harvest that absolute monster IV of 178%. 🚜 💰 The market is pricing in a wild ±18% swing ($4.56 move) for the 17th. Range is sitting between $20.71 – $29.83. Taking the "rent" while the infrastructure plays stay spicy. 🚀📈 #APLD #OptionsTrading #CoveredCalls #FinTwit