@pinebrookcap Thank you. I tried to report this to @Twitter several times but to no avail. Hopefully they will listen to you.

English

Roberto Perli

2.8K posts

@R_Perli

Head of Global Policy Research at Piper Sandler. Former founding partner of Cornerstone Macro and Federal Reserve senior staff member.

An independent #FederalReserve is critical to the well-being of the US #economy. Having said that, it is getting harder to justify such independence when four big operational errors (of analysis, forecasts, actions and communication) are accompanied by a lack of accountability.

Congrats to our Hutchins Center colleague Ben Bernanke! @BrookingsEcon nobelprize.org

How far can Fed QT go before the Treasury market goes from illiquid to dysfunctional? @R_Perli estimates: "reserves may not shrink more than an additional $500-750 billion without inducing a dysfunctional Treasury market." a.k.a. at least 7 months at the current pace.

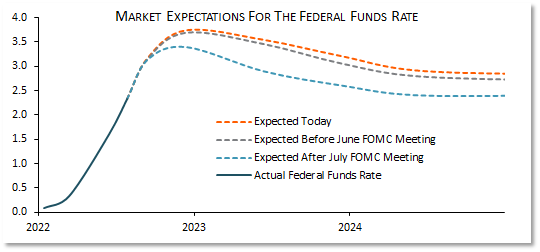

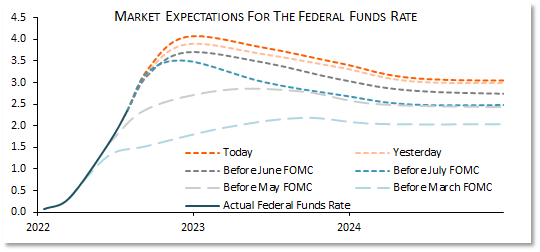

Another hawkish #FOMC meeting this week. - Odds of 100-bp hike greater than the 20% the mkt prices in and close to 50% - Dots to show FFR above 4% this year and a bit higher in '23 - Powell will try to sound hawkish, but experience suggests room for mkt misunderstanding. 1/3

@R_Perli Could only go back to 1998 via Fed archive. Unsure where to get 1978-1997 federalreserve.gov/newsevents/spe… federalreserve.gov/newsevents/spe…