Raju | Insurance & Finance

125 posts

Raju | Insurance & Finance

@RajuFinExplains

Simplifying Insurance, Banking & Personal Finance for Indians 🇮🇳 No hype. Only clarity.

Patna, India Bergabung Mart 2020

76 Mengikuti13 Pengikut

@RajuFinExplains Great question to unpack. When correlations spike like this, it usually means liquidity is leaving the system rather than rotating between assets. Cash and patience become positions of their own in those moments.

English

Gold, Crypto, Tech stocks, and even Oil are all crashing at the exact same time. If everything is going down... where is all that money actually going? 🤔💸 Let's break it down simply:

When the entire market turns red, the money isn't moving to another investment. It's either hiding in pure cash or being completely wiped out by debt. 🛑📉

Here is what’s really happening:

1️⃣ Everyone is running to Cash ($DXY): When investors get scared of inflation and high interest rates, they stop taking risks. They sell their stocks, crypto, and gold, and just hold onto the US Dollar. Right now, sitting on cash pays a decent guaranteed return, so big investors are choosing safety over volatility. 💵🛡️

2️⃣ Money is literally disappearing: It sounds crazy, but a lot of the money isn't being moved—it's being deleted. The stock and crypto markets run on massive amounts of borrowed money (leverage). When prices drop, brokers force traders to sell their assets immediately to pay back their loans. Billions of dollars in value are simply erased just to settle debts. 💥🕳️

The Big Picture: In a market like this, doing nothing and holding cash is a valid strategy. The money isn't lost forever; it's just sitting safely on the sidelines waiting for the panic to stop before buying things up at a massive discount. 💼📊

Are you panic-selling everything right now, or are you sitting on cash waiting for the perfect time to buy the dip? 👇

#StockMarket #Crypto #Bitcoin #Gold #Investing #MoneyTips #EconomicsMadeEasy

English

Buying a ₹1 Crore Term Insurance plan blindly? You might be leaving your family completely exposed. 🚨🧵

Most people treat Term Insurance like a random checklist item: "Premium cheaper is better, let's buy a random cover." But a single mistake can turn your financial safety net into a nightmare during a claim.

Here is a quick, no-nonsense checklist you MUST check before signing the dotted line: 👇

1️⃣ The HLV Cap (Stop guessing your Sum Assured)

You can't just buy any cover you want. Insurers calculate your Human Life Value (HLV).

A standard thumb rule is 20x to 25x of your annual income.

If your annual income is ₹10 Lakhs, aim for a ₹2.5 Crore cover. Don't let agents under-insure you with a basic ₹50 Lakh policy just to show a lower premium! 📉

2️⃣ Claim Settlement Ratio (CSR) vs. Claim Amount Settlement Ratio

Don't just look at CSR (number of claims settled). Look at the Amount Settlement Ratio (the actual value of total money paid out).

Look for insurers with a CSR consistently above 98% over the last 3-5 years. Brand reputation and corporate governance matter when it's D-day for your family. 🏛️

3️⃣ The "Moratorium Period" is NOT a License to Lie 🛑

Under IRDAI rules, after 3 years (for term plans), an insurer generally cannot reject a claim.

BUT HERE IS THE CATCH: If the insurer proves willful fraud or deliberate hiding of chronic pre-existing diseases (like diabetes, heart conditions, or cancer) to get the policy, they can take it to court, cancel the policy, and forfeit your premiums.

Declare every medical checkup, smoking habit, and family history honestly. A rejection at the proposal stage is 100x better than a claim rejection for your grieving family. 📑

4️⃣ Skip the "Return of Premium" (TROP) Trap 🪤

Agents love selling "Term with Return of Premium" because you get your money back if you survive.

The Reality: These plans charge a significantly higher premium.

Better Strategy: Buy a regular, pure term plan. Take the money you saved on the premium difference and put it into a low-cost Index Fund or Public Provident Fund (PPF). You will end up with a much larger corpus! 💰🚀

5️⃣ Choose Policy Term Wisely (Don't insure till 85!)

You only need a term plan until your active working age and until your major liabilities (home loans, children's education) are cleared.

Taking a cover up to age 60 or 65 is usually optimal. Extending it to age 80 or 85 just inflates your premium unnecessarily for years when you no longer have active income to replace. ⏳

Bottom Line: Pure term insurance is the cheapest and most powerful financial gift you can give your family. Buy it early when you are young and healthy to lock in dirt-cheap premiums.

What is the biggest roadblock holding you back from buying a pure term insurance policy today? Share your doubts below! 👇

#PersonalFinanceIndia #TermInsurance #FinancialLiteracy #MoneyTips #InsuranceAdvice #TermPlan #FinancialPlanning #IRDAI

English

Perfectly put. The "cost of waiting" is a real financial metric. ⏳❌

Even if a correction comes, history shows that the structural winners always emerge stronger (like Amazon after 2000). The goal isn't to avoid the volatility; it's to build a portfolio resilient enough to survive it while pocketing the gains along the way. Invest, hedge, and don't just watch from the bleachers. 💯🚀

English

Many are assuming that AI bubble is going to burst like the 2000 dotcom bubble.

Here are some points you need to think about:-

- AI might/might not be a bubble.

- If there is a bubble. And, if it pops: markets will drop 80%+ like in 2000.

- This theory is not new. This has been going on for at least 2 years.

In that phase: people lose 40%+ run up already.

Optimism has "bubble-risk".

Pessimism has "missing the run-up risk".

You are betting either way.

So build your strategy.

Or see the world go by.

Akshat Shrivastava@Akshat_World

In 2000 dot com bubble. The market corrected by 83%. Someone invested 100 at peak. That money became 17. But, here is the interesting fact that almost no one is talking:- If you invested 100 before crash. Went through the entire bubble burst. Stayed put. You are now at 7.9X. This is roughly 8.3% CAGR in $ terms over the last 26 years. Massive gains? No. But, this is assuming you invested all your money at absolute peak. And, never downward averaged anything. A more realistic return estimate would be 12-13% CAGR in US$ terms. Point being: if you invest in things where value is migrating towards, you're likely to win. There is a reason why top firms like Google, Meta are staking all their cash, reputation and assets on the line for participating in the AI built out. If you step back and zoom long-term: this is one of the cleanest phases where these firms are deploying large capital with a lot of conviction. While the short-term noise of 5%, 10% fall will always be there. If you deploy capital patiently: there is good money to be made. I did a podcast with actual investors who are putting money on AI investments, do check out there views.... (these are real folks, putting real money on the line)

English

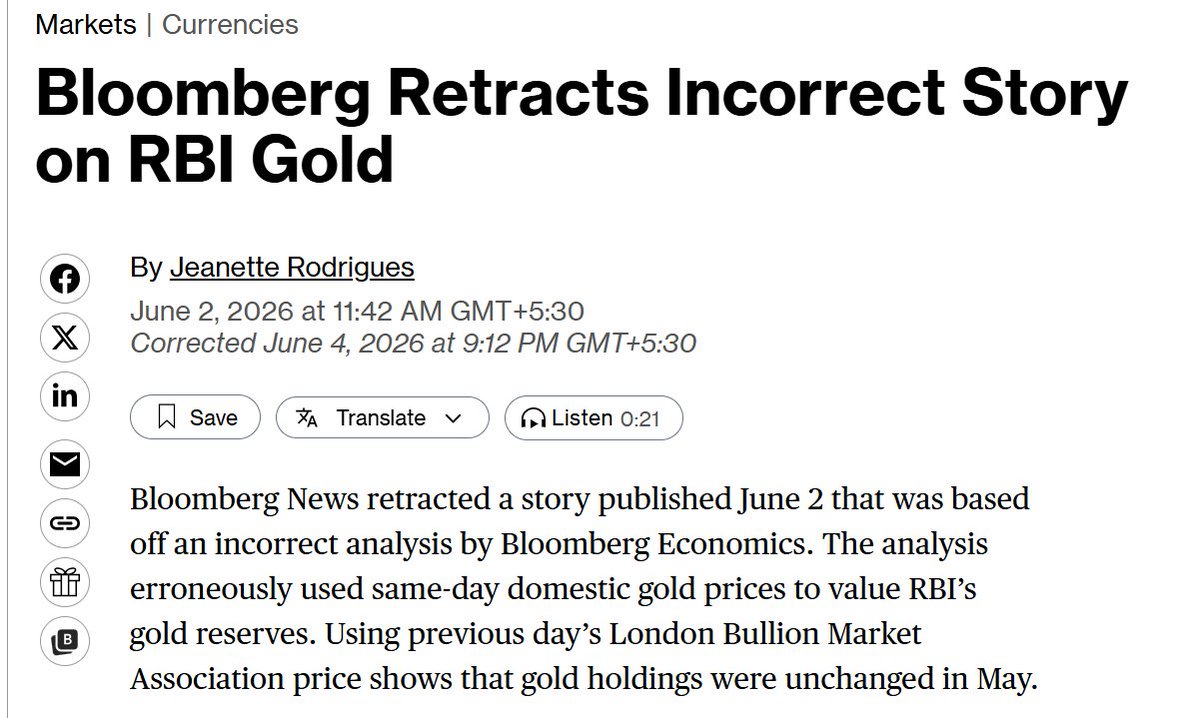

Hit the nail on the head. 🔨 Some people are so conditioned to look for a "scam" that they will trust a foreign outlet’s spreadsheet error over actual, verified data from their own central bank.

The physical gold stock didn’t change by a single gram—the price did. Basic economics, but the narrative had to be spun anyway. Be proud of the RBI; they are running one of the most resilient economies in the world right now. 🇮🇳💯

English

On June 5th, the incorrect analysis is retracted.

Despite the RBI clarification, social media analysts were raising doubts on RBI gold holdings while going by the wirehouse's analysis.

This happens only in India.

I have met many nationalities in a career of four decades. National pride, patriotism is foremost.

Only in India, we first want to pull down our own country and put our belief in outsiders.

When I was an investor in a textile startup, this was starkly evident. A Chinese buying agent would give the Chinese suppliers a lot of leeway and go out of the way to favour Chinese producers . Indian buying agents would be the worst for Indian producers.

Have seen that in various formats.

Having worked with German and Japanese owned companies, this was very evident. The National pride was something that you could count on at every step.

Only in India we have mastered the pulling down of the Nation.

The same was the case here.

Despite RBI saying the Gold holdings are constant "as on date" there were doubts raised on what that meant, was RBI using old data and gold had been sold in May etc etc.

Now the "incorrect story" is retracted.

If this was China, the wirehouse would have been severely penalised.

We shrug off these anti India moves too lightly.

Be more proud of your country and its institutions.

We are a 20,000 year old civilisation and a young modern country that is progressing fast. Faster than all major economies of the world.

We are not perfect but neither are the others.

But their nationals are much more patriotic.

There is no apology from this media outlet which often publishes anti India narratives brazenly.

English

I believe, If the RBI sounds unexpectedly hawkish or hints at prolonged rate pauses due to global supply shocks, banking stocks will face immediate selling pressure. Conversely, a status quo with an optimistic growth commentary will trigger a strong relief rally across banking and NBFC counters.

English

#MarketsWithMC | Trading Plan: Will RBI policy help Nifty 50 reclaim 23,500, Bank Nifty march toward 55,000?

-Market awaits the outcome of three-day RBI MPC meeting scheduled on June 5

-Nifty 50 likely to remain range-bound until it convincingly surpasses and sustains above 23,700 on the higher side

-Immediate support seen at the 23,300 and resistane at 23,500

Read More ⤵️

moneycontrol.com/news/business/…

English

🌅 Morning Outlook(05-Jun-2026): D-Day For Bulls! RBI Policy Takes Center Stage 🏛️🔥

D-Day for traders! 🏛️🔥 GIFT Nifty points green, but the RBI Policy at 10 AM will decide if the market rallies or crashes! 📈📉

A breather for the bulls! GIFT Nifty is trading up ~0.3%, supported by Brent crude cooling off 3% from its highs to $96.97. But don't get comfortable—the real trend starts when the RBI drops its interest rate decision. 🌋⏳

📍 Nifty: A positive open is on the cards. The 23,300 level is the absolute line of defense for the bulls. If the RBI stays neutral, we can expect a fast push toward 23,550–23,600. Overhead resistance sits at 23,500. 🛡️

📍 Bank Nifty: Gearing up for massive premium swings. The 53,600 zone needs to hold on an opening basis; a supportive policy could trigger heavy short-covering toward 54,200+, while a hawkish surprise opens the trapdoor to 53,300. 🏦

🚨 The Major Trigger: RBI MPC at 10:00 AM. While a repo rate hold at 5.25% is expected, the central bank's commentary on inflation, rising bond yields, and growth will dictate the trend for high-beta banking heavyweights like $SBIN and $HDFCBANK. 💸📊

Strategy: Protect your capital! Avoid over-leveraging in the first hour. Let Governor Sanjay Malhotra finish his address and let the options premiums settle down before initiating fresh directional trades. 💼🔍

Are you sitting on cash ahead of the RBI policy announcement, or are you betting on a massive short-covering rally in bank stocks today? 👇

#StockMarketIndia #Nifty50 #BankNifty #RBIPolicy #GIFTNifty #TradingStrategy #OptionsTrading #NiftyPrediction

English

🌅 Morning Outlook(04-Jun-2026): Gap-Down Alert! Bears Take the Wheel 🐻🌋

Brace for impact! 🚨 GIFT Nifty down 150+ points as global markets bleed. Are the bulls completely trapped? 📉🐻

A brutal risk-off wave has hit global equities. Wall Street slumped overnight as spiking crude oil prices rekindled inflation fears, sending the GIFT Nifty down 155 points—indicating a major gap-down for Indian markets. 🌋🇺🇸

📍 Nifty: Gearing up to test its core structural base. The 23,150–23,200 zone is the ultimate line of defense for the bulls. If it breaks, expect deeper liquidations. Heavy overhead resistance now locks in at 23,500. 🛡️

📍 Bank Nifty: Staring at a 350+ point opening cut. Eyes are entirely on the 53,200–53,300 support floor. If this holds, expect a short-covering bounce; if it breaks, the gates open down to 53,000. 🏦

🚨 The Macro Headwind: Surging oil prices and a sharp spike in bond yields will put interest-rate-sensitive stocks like $SBIN and $HDFCBANK under immense pressure from FII selling early on. 💸📊

Strategy: Gaps like these are meant for patience, not impulse. Avoid chasing shorts at the open or catching a falling knife. Let the market form a stable baseline around the 23,200 area before building long setups. 💼🔍

Are you buying this 150-point gap-down as a deep-value opportunity, or do you think this is the start of a much larger June correction? 👇

#StockMarketIndia #Nifty50 #BankNifty #GIFTNifty #TradingStrategy #OptionsTrading #NiftyLevels #NiftyPrediction

English

Spot on! 🎯 Most people treating term insurance as a random guessing game get burned by inflation later.

Two crucial things people miss in this calculation:

The Human Life Value (HLV) Cap: Even if Option 2 says you need ₹4 Crore, insurance companies won't give it to you if your income doesn't support the underwriting. You can't just buy any amount you want.

Inflation is a Term Plan Killer: A ₹1 Crore cover feels massive today, but in 20 years at 6% inflation, its actual purchasing power drops to roughly ₹31 Lakhs.

Pro Tip: If affordability is an issue, start with a basic cover and choose an Increasing Term Insurance plan where the sum assured automatically bumps up by 5–10% every year to fight inflation. 📈🛡️

#FinancialLiteracy #TermInsurance #PersonalFinanceIndia

English

🚨How much Sum insured should you buy for a term plan?🤔🤔

Most people are confused about one of the most critical aspects of a term plan:-

Sum Insured

How much should u buy?

This is one of the most difficult questions with no clear answer

So let's deep dive👇👇

Why do u buy a term plan?

A term plan is ideally bought for the income replacement of an earning member in case something happens to them.

Option 1:-

Multiple of the annual income,

Many people just go on to choose the multiple of the annual income,

Let's say 25x or 30x of the annual income,

Let's say ur annual income is 10L

Then they buy a term plan for 2.5 or 3cr,

Option 2:-

Income replacement and liabilities method,

Term plan Sum insured=Income replacement-assets+liabilities

If your annual income is ₹10 Lakh,

Here is what your calculation might look like:

· Income Replacement (20 * ₹10 Lakh): ₹2.0 Crore

· Plus Outstanding Loans (e.g., Home Loan): + ₹50 Lakh

· Plus Child's Education Fund: + ₹30 Lakh

· Minus Existing Investments: - ₹30 Lakh

· Total Required Sum Assured: ₹2.5 Crore

Option 3:-

Depends on the premium affordability as well.

Someone may need a term plan of 4cr,

But it may not be affordable to them,

So this is also a way to select the sum insured in a term plan

So net net,

Every term plan is really different,

Be very careful while selecting a term plan,

Inflation is real.

Under-insuring leaves your family vulnerable.

Evaluate your liabilities today, review your cover every 5 years, and never let your policy lapse.

English

🌅 Morning Outlook(03-Jun-2026): Can Bulls Defend Yesterday’s Massive Intraday Reversal? 🐂🥊

Another massive gap-down! GIFT Nifty tumbles 120+ points—will yesterday’s heroic recovery hold or fold? 📉🚨

The market is refusing to give the bulls an easy ride. Despite yesterday’s spectacular 328-point intraday rescue mission, global cues and a 120-point knock on the GIFT Nifty point to a volatile opening bell for Indian equities. 🌋🐻

📍 Nifty: The 120-point drop brings us right back to the edge. All eyes are on the 23,350 critical demand zone. If this breaks, the bears will easily target 23,230. Resistance shifts back up to 23,500. 🛡️

📍 Bank Nifty: Gearing up for a tough defensive day. The 53,700 level must be held on an opening basis; a clean breakdown opens the doors straight to 53,400. 🏦

🚨 The Macro Headwind: Rising Indian bond yields combined with heavy FPI selling momentum (nearly ₹33k Cr wiped out in May) will keep rate-sensitives under intense pressure today. Play defensively. 💸📊

Strategy: Cash remains king in high-volatility gaps. Do not chase the morning short or catch a falling knife. Let the first 30 minutes settle to see if the 23,350 demand zone can successfully spark a bounce. 💼

Are you treating this 120-point gap-down as a discount buying opportunity, or do you think the bears are about to take full control of June? 👇

#StockMarketIndia #Nifty50 #BankNifty #GIFTNifty #TradingStrategy #OptionsTrading #NiftyLevels #NiftyPrediction

English

Saving a few thousand rupees by hiding a disease is the worst financial trade you can make. 📉❌

Insurers have massive forensic medical teams. If they prove intentional fraud, the 3 or 5-year moratorium rule completely vanishes. You don't just lose the claim; you lose the entire policy and all the premiums you paid.

Always choose a rejection at the proposal stage over a rejection at the claim stage!

English

🚨Can the moratorium period help you if you hide diseases in health/life insurance?

Many people are not eligible for health/life insurance due to pre-existing medical conditions

In frustration,

They say they will hide medical conditions and take a policy,

In health insurance after 5 years,

The insurer cannot reject a claim,

In term insurance after 3 years,

The insurer cannot reject a claim,

But can the moratorium period save you in case you willfully hide a disease to gain policy?

The clear answer is "NO."

No, the moratorium period will not protect you if you deliberately hide or misrepresent pre-existing diseases

IRDAI created the moratorium period to protect the rights of the policyholders.

IRDAI didnt create the moratorium period to misuse it to hide diseases to gain insurance,

While the moratorium applies to everything,

IRDAI still let insurers not apply a moratorium period in case of FRAUD

If the insurer can prove a FRAUD

Insurers retain the legal right to reject claims, cancel your policy, and forfeit your premiums if they establish intentional deception

So can the insurer reject a claim even after 5 years?

This is a certain grey area.

The regulation gives insurers the power to reject claims in case of fraud.

If the insurer is able to prove that you knowingly hid pre-existing diseases in order to gain insurance, then the insurer will take the matter to court by categorising it as fraud

Therefore, it is important to disclose all pre-existing diseases honestly while buying the policy.

One must not depend on the moratorium period, thinking they will not disclose diseases honestly, but the insurer will have to service claims after the moratorium period

Remember, honesty is the best policy in health insurance.

English

@theRealKiyosaki Because governments have a spending problem, not a revenue problem. They operate on a fiat printer where the rules of personal finance don't apply to them—until the inflation bill arrives. 💸🖨️

English

HOW DOES a GOVERNMENT that takes 40% of everyone’s money wind up trillions in debt?

Thank GOD our government is not any bigger.

English

🌅 Morning Outlook(02-Jun-2026): Bears Strike Back early in June! 🐻📉

Bears strike back! GIFT Nifty down 150+ points—is the June rally already in danger? 📉🚨

The bulls are facing an immediate reality check this morning. A brutal risk-off wave across Asian markets has sent GIFT Nifty tumbling over 150 points, pointing to a rough, gap-down opening bell for Indian equities. 🌋🐻

📍 Nifty: The 150-point drop puts us right back to the edge. Eyes are glued to the 23,500 critical demand floor. If this level breaks, the bears will easily target 23,350. Immediate overhead resistance moves to 23,750. 🛡️

📍 Bank Nifty: Gearing up for an aggressive defensive play. The 53,800–54,000 zone must be protected by options writers; otherwise, we're looking at a fast slide down to 53,400. 🏦

🚨 The Macro Headwind: A sudden bounce in domestic 10-year bond yields coupled with persistent global profit-taking is going to put heavy-beta rate-sensitives like $SBIN and $HDFCBANK under immediate pressure at the open. 💸📊

Strategy: Cash is king in high-volatility gaps. Avoid chasing the morning short or catching the falling knife. Let the indices establish a clear equilibrium over the 23,500 base before deploying fresh capital. 💼🔍

Are you utilizing this 150-point gap-down to buy high-quality banking stocks at a discount, or do you expect deeper cuts ahead this week? 👇

#StockMarketIndia #Nifty50 #BankNifty #GIFTNifty #TradingStrategy #OptionsTrading #NiftyLevels #NiftyPrediction

English

This is classic hindsight bias and a flawed financial comparison.

Comparing Sukanya Samriddhi Yojana (SSY)—a tax-free, guaranteed sovereign bond—to a single tech stock like Google over a tiny 3-year window is apples and oranges.

Betting your daughter’s entire 21-year future on one single company isn't 'smart risk management'; it’s massive concentration risk. Ask anyone who bought Intel or Cisco at their peaks.

SSY isn't meant to make you rich; it’s a volatility hedge to ensure your daughter has guaranteed funds at 18 even if the stock market crashes. The real alternative to SSY is a diversified equity index fund, not a single-stock gamble that happened to pay off this time.

English

My daughter was born in 2023. My wife & I debated investing in Sukanya Samriddhi Yojana (SSY)

We ended the conversation in 2 mins. And, decided to put 100K in Google. That's it.

100 units in SSY= became 135

100 units in Google= became 390

That's 8.3X more returns.

But, wait: SSY gives returns in INR, google gives returns in USD. So let's adjust for that as well.

100 units in Google = became 450 (INR-adjusted). That's ~10x more returns.

Some will say: oh the risk is high. Yes, absolutely.

When you lock money for 21 years trusting the government, that's the highest unit of risk you're taking.

English

Exactly. Insurance companies love the "99-year" emotional pitch because "payout sure-shot hai." 🧠🪤

But they pocket the time value of your money. By the time that ₹1 Crore payout happens at age 85 or 90, inflation will have severely eroded its purchasing power—it will feel like ₹10-15 Lakhs in today's value. 💸📉

Buy protection till your retirement, invest the rest, and break free from the "premium waste" mindset.

#MoneyTips #FinancialEducation #InsuranceTrap #MiddleClassIndia

English

🚨Term life isnurance plan till 60/65 or till 99 years?🤔🤔

Many people think,

Let's buy a term plan till 99 years,

If we are paying life insurance premiums,

We will get a sure-shot payout,

Why waste the premium?

But let's look at this objectively!

What is the function of a term plan:-

A term plan (term life insurance) is a pure life insurance policy that provides a substantial death benefit to your beneficiaries if you pass away within a fixed, agreed-upon period (e.g., 10 to 40 years).

It is basically needed to replace the income of the earning member of the family,

So that the dependent members can get money to live,

A term plan is generally bought till retirement.

Once the income of the earning member vanishes no need of a term plan,

Let's take an example,

For a 30-year-old,

You buy a term plan up to 99 years,

You buy a term plan until 60 years,

For a 1cr cover,

The yearly premium for 60 years is Rs 9,497/-

The yearly premium for 99 years is Rs 25,474/-

For 60 years u end up paying Rs2,84,910

For 99 years u end up paying Rs17,57,706

The return for 65 years will be 16-18.5%(provided a payout happens at 65 years)

The return for 99 years will be 4-4.5%(provided a payout happens at 65 years)

The returns sharply drop as you choose a longer tenure

The insurance company themselves know,

By buying the term plan till 99,

They will have to give a sure shot payout,

There they steeply load the premium

Therefore, always choose the tenure only till retirement

English

🌅 Morning Outlook(01-Jun-2026): Turning the Page to a Bullish June?

$93 Crude & Dow Records: Will the June Series start with a massive Bull revival? 🛢️🚀

After Friday's painful liquidation, the macro landscape has completely flipped over the weekend! GIFT Nifty is pointing to a positive open near 23,725 as global markets surge on inline US PCE inflation data. 📊🔥

📍 Nifty: Eyes are locked firmly onto the 23,750 day pivot. If the first 30-minute candle closes above this level, expect a fast short-covering push back toward 23,850. Major support sits at 23,500. 🛡️

📍 Bank Nifty: Gearing up for a recovery attempt. Demands are strongly packed in the 53,900-54,000 zone, while the 54,800 line acts as the primary overhead target. 🏦

🚨 The Macro Tailwinds: Brent crude tumbling down to $93/bbl on West Asia easing is massive news for India. Cooling bond yields will act as a direct fuel injection for interest rate-sensitive spaces like Private Banks ($KOTAKBANK) and NBFCs. 📈💸

💻 Sector Momentum: Watch out for IT to continue its leadership role following Wall Street's AI-driven tech party on Friday night! 🤖📱

Strategy: Let the opening gap settle. If the market comfortably absorbs the morning tick and stabilizes above 23,750, structure long trades with strict trail stops. 💼

Are you buying the morning gap-up in Private Banks and IT, or are you waiting for the market to give a clearer confirmation past 23,800? 👇

#StockMarketIndia #Nifty50 #BankNifty #GIFTNifty #CrudeOil #PersonalFinance #OptionsTrading #TradingStrategy

English

👑 BACK-TO-BACK CHAMPIONS! RCB REIGNS SUPREME IN 2026! 🏆❤️

THE CHAMPIONS HAVE A NAME, AND IT’S ROYAL CHALLENGERS BENGALURU! 🏆🏆

2025: Champions 🥇

2026: BACK-TO-BACK CHAMPIONS 👑

History has been rewritten at Ahmedabad! King Kohli delivers yet again in a grand finale as RCB chases down the target against GT to successfully defend their crown. The era of RCB dominance is officially here! ❤️🔥

#RCBvGT #IPL2026Final #PlayBold #IPL2026 #Champions #ViratKohli #EeSalaCupNamdu #BackToBack

English

Most complex financial products have higher costs

and lower transparency.

Low-cost, simple products (like index funds)

have historically delivered competitive returns.

Simplicity works.

#FinancialAwareness

English

Credit card interest rates can go up to 36–42% annually.

A ₹50,000 unpaid balance

can grow rapidly if only minimum due is paid.

Always clear full dues.

#PersonalFinance

English

📊 Weekly Review (25–29 May 2026): The 24,000 Mountain Reclaimed and Lost! 🎢💥

From 24,000 Euphoria to a 359-Point Friday Crash: The ultimate May F&O Series plot twist! 📉🎢

The week of May 25-29 was a textbook reminder of market vulnerability. We started the week populating a historic bull run past 24k on lower crude prices, but ended with a brutal ₹6 lakh crore liquidation on Friday. 📊💥

📍 Nifty 50: Succumbed to heavy post-lunch selling on Friday, tanking 1.50% to close the week at 23,547.75—completely erasing the weekly breakout.

📍 Bank Nifty: Failed to hold its higher ground as FIIs resumed basket selling in financial heavyweights, turning the week's initial 1,200-point gain into an aggressive trap. 🏦⚠️

💻 The Silver Lining: Nifty IT ($INFY, $TCS, $WIPRO) showed brilliant relative strength early Friday, but it wasn't enough to stop the broad-based cascading bleed as India VIX jumped 8%.

The Takeaway: The 24,000 ceiling remains a multi-week structural resistance wall. Going into early June, the bulls must now aggressively defend the 23,450–23,500 demand pocket to avoid triggering a deeper multi-month correction. 🛡️💼

Did you book profits during Monday's historic 24k surge, or did Friday's sudden 359-point cascade catch your portfolio off guard? 👇

#StockMarketIndia #Nifty50 #BankNifty #WeeklyWrap #SensexCrash #OptionsTrading #Investing #TradingStrategy

English